Is Bangladesh’s economy ready to withstand these external shocks?

The US Federal Reserve in a statement on March 4 warned that the coronavirus outbreak, which has already disturbed travel and access to goods worldwide, could cause further disruptions in the coming weeks. In a bid to boost confidence and shore up the US economy, the Fed even had to make an emergency interest rate cut. The outbreak, however, has gotten much worse since then.

In Bangladesh, export earnings in February declined 1.8 percent year-on-year to USD 3.32 billion mainly because of a slowdown in apparel shipment, according to data from the Export Promotion Bureau (EPB). It was 10.74 percent short of the USD 3.72 billion target set for the month. Meanwhile, exporters and economists fear that exports may receive further blows amid the coronavirus outbreak in China, the major source of raw materials for Bangladesh's apparel items.

Given the importance of China in the world's supply chain, and the rate at which the virus is spreading to other countries and regions, it is obvious that other sectors too will be affected. And this is likely to happen on a global scale.

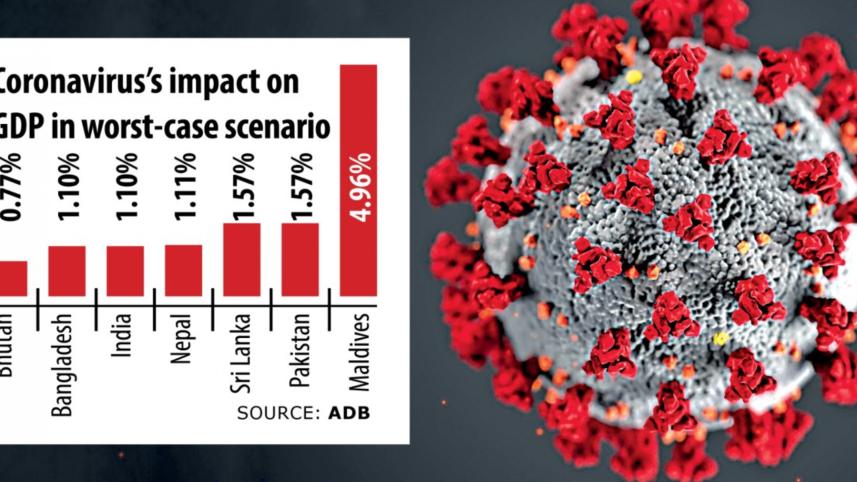

According to an analysis done by the Asian Development Bank, in a hypothetical worst-case scenario, Bangladesh's gross domestic product may contract by as much as 1.1 percent due to the outbreak. It forecasted that the virus could wipe USD 3.02 billion off the country's USD 300 billion-plus economy and lead to 894,930 job losses.

One of the main ways the virus could damage economies is through creating panic and shattering public confidence. For example, in India, the outbreak which is yet to kill even one person, has been absolutely lethal to the country's poultry industry. Fuelled by social media posts suggesting that the COVID-19 could be transmitted through white meat, the unfounded rumour prompted many to drop chicken and eggs from their daily diet and made poultry sale plummet by up to 80 percent across India, the third-largest producer of eggs and fourth-largest of chickens in the world.

While this was happening, the world's oil market also experienced some volatility. After the breakdown of a crucial global oil pact involving OPEC+, oil prices plunged 25 percent. Despite managing to claw back up again, it is clear that since peaking after the killing of Iranian General Qassem Soleimani, oil prices have been sliding further and further down. This is why the OPEC tried to save itself by asking for a historic production cut, which Russia did not agree to.

As a result, oil suffered its sharpest drop since the 1991 Gulf War and global stocks plunged on Monday after Saudi Arabia launched a crude price war with Russia, further rattling investors who were already anxious about the spread of the virus. Moreover, since beginning to trade in December, shares of Saudi state oil company Aramco—the world's most valuable company with a price tag of USD 1.7 trillion—fell below their initial public offering price for the first time on Sunday.

The two factors—COVID-19 and uncertainties in the oil market—could prove devastating for the global economy, according to author Pepe Escobar. He writes that the planet seems to be "under the spell of a pair of black swans...caused by an alleged oil war between Russia and the House of Saud, plus the uncontrolled spread of Covid-19—leading to an all-out 'cross-asset pandemonium'." A black swan is an unpredictable event that is beyond what is normally expected of a situation and has potentially severe consequences. Economist Rehman Sobhan also compared the coronavirus to the black swan. He said the coronavirus "emerged out of nowhere and it is a lesson to all of us that even though everything is going well in the economy, random shocks can come and afflict you and you may not be prepared for this."

But unfortunately, everything has not been going well for our economy. As experts have been pointing out, confidence in our banking sector is already at an all-time low due to the huge amount of non-performing loans in the sector. This means that the financial sector, responsible for distributing resources into the economy in a competitive and predictable way, is itself extremely vulnerable to any shocks—leaving the rest of the economy exposed.

If we look at India for comparison, shares of Yes Bank recently plunged by as much as 85 percent on March 6 after the central bank seized control and imposed withdrawal limits to prevent the collapse of the country's fourth-largest lender. The decision sparked a sell-off across the troubled banking sector and sent the rupee falling to its weakest level since 2018.

At a time when there are so many uncertainties that could affect global markets, it is crucial to have stability in the financial sector, which we desperately lack. The United Nations Conference on Trade and Development released a study on March 9 where it offered some parallels between the Asian financial crisis of the late 1990s and today. And said, "Public and private aggregate debt levels in many developing countries already are elevated, and in several cases acute." Warning that, "Central Banks are not in a position to solve this crisis alone and an appropriate macroeconomic policy response will need aggressive fiscal spending with significant public investment."

Bangladesh is a perfect candidate to be among the countries the UNCTAD was referring to. Meaning it could be heavily exposed to the current (and any future) external shocks reverberating across global markets and the economy.

However, the answer to overcoming the current crisis is not to panic. After that, we must identify the weaknesses we have and try and fix them. On Bangladesh's part, that will require "a series of dedicated policy responses and institutional reforms"—as prescribed by the UNCTAD—particularly in the banking sector.

Eresh Omar Jamal is a member of the editorial team at The Daily Star.

His Twitter handle is: @EreshOmarJamal

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments