Sales of savings tools soaring

Net sales of savings instruments continue to post robust growth this fiscal year riding on the higher returns than its alternatives.

Bangladesh Bank data shows net sales of savings tools stood at upwards of Tk 11,650 crore during the July-September quarter, up 74.37 percent year-on-year.

Over Tk 3,854 crore worth of savings certificates were sold in September this year, up by a whooping 88 percent from a year earlier.

BB officials and commercial bankers attributed the growth to the returns the government offers for investments in savings tools.

Investors were lured in by the interest rates, which are 5-6 percentage points higher than those offered by commercial banks on term deposits.

"High interest rates are the main reason for this surge in sales in recent months," said Ayezuddin Ahmed, a director of the Department of National Savings.

People also feel a sense of security in investing their money in government's savings schemes, he said.

But BB officials and bankers said the higher rate of returns is not only distorting the market but also creating interest payment burden on the government, which can lead to a mismatch in treasury management.

"The rate is distorting the market. More people will rush in to buy the instruments," a BB official said.

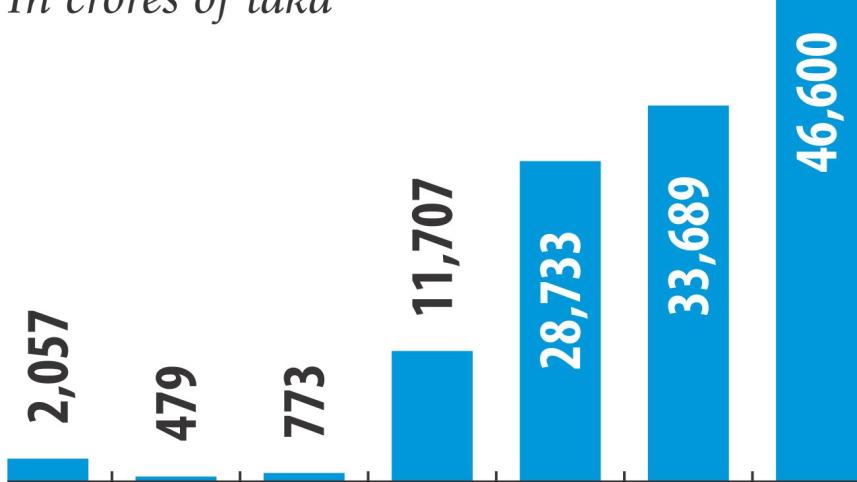

The net sales of savings certificates were more than double the target set by the government for fiscal 2015-16: it stood at Tk 33,688.6 crore -- the highest in the country's history -- against the target of Tk 15,000 crore.

The government sold savings instruments of Tk 28,732.66 crore in fiscal 2014-15, while the amount was Tk 11,707 crore the year before.

In fiscal 2012-13, the total sales of the instruments were a meagre Tk 772.84 crore.

People, be it retired government employees, private service holders, businessmen or housewives, are running to invest their savings in these tools because of the returns, which are beyond any market rate. Currently, banks offer 6-7 percent interest rate for term deposits and it is a minimum of 11 percent for investments in savings schemes.

"I don't understand why the government is borrowing at so high a cost when the money is available at much cheaper rates," said Ahmed Kamal Khan Chowdhury, managing director of Prime Bank.

The expected cash is not flowing into the capital markets because of the very high rate of returns on savings tools, he said. In May last year, the government slashed deposit rates on savings instruments by up to 2 percentage points. But still it is higher than the others.

The interest rate on the five-year family savings certificates has been brought down to 11.52 percent from 13.45 percent, according to a notice of the Internal Resources Division. The five-year pensioner savings schemes saw its interest rate slashed to 11.76 percent from 13.19 percent.

The interest rate on the three-year post office savings certificates came down to 11.28 percent from 13.24 percent.

For Bangladesh Savings Certificates, the rate was fixed at 11.28 percent, down from 13.19 percent. The three-year profit-based savings certificates saw their deposit rates go down to 11.04 percent from 12.59 percent.

On the other hand, commercial banks offer 5.5-6 percent for term deposits and the average return on five-year bonds is 6.5 percent. The call money rate has come down to around 3.5 percent in recent days, and the capital market is not lucrative for investors either.

A senior banker said the rates on government savings schemes are distorting the market in different ways.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The government set the target to borrow Tk 15,000 crore from savings scheme last fiscal year, but it got more than double the sum. Consequently, the government's interest liability will shoot up, he said.

On the other hand, the target to borrow from commercial banks remained hugely unachieved, so the banks would get demoralised as their excess liquidity would be soaring, he said. BB data also supports the observation.

The government borrowed only around Tk 4,000 crore from the banking system against the target of Tk 38,523 crore for fiscal 2015-16, though the banks were sitting on excess liquidity. For the current fiscal year, the government has planned to borrow Tk 43,000 crore from the banking sector to meet its budget deficit.

"We are in trouble as the BB is not buying the banks' money. The repo and reverse repo are totally inactive," said a frustrated managing director of a private commercial bank requesting not to be named.

Presently, an individual can invest up to Tk 30 lakh in five-year term certificates and three-month profit-bearing certificates.

An adult female can purchase up to Tk 45 lakh in savings instruments under Paribar Sanchayapatra (family savings certificates), and the relatively rich take advantage of this by investing big sums in them.

Comments