Agent banking: the bright spot in lending landscape

Agent banking, which takes banking services to the unbanked people, is going from strength to strength, with both deposit collection and loan disbursement on the rise.

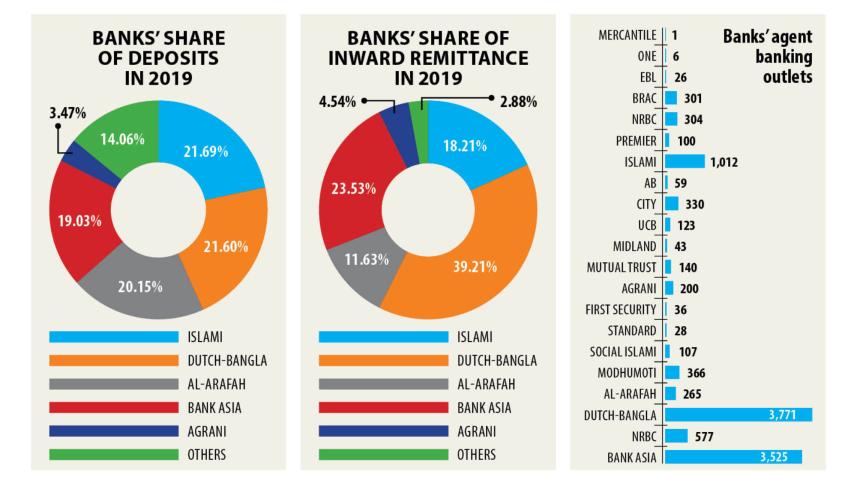

Lenders earlier kept their core focus on collecting deposits from clients through the new banking wing but they have given the same importance to loan disbursement and inward remittance.

As of September last year, loan disbursement through the agent banking channel was Tk 446 crore, which is more than double that from a year earlier. At the same time, deposit collection went up 142 per cent to Tk 7,517 crore, according to data from the central bank.

"The tremendous growth of agent banking proves that the underprivileged people are keen on banking services," said Md Arfan Ali, managing director of Bank Asia.

There remains huge scope for widening agent banking as lenders are yet to extend their traditional banking service to the large numbers of unbanked people.

"We will focus more on agent banking in the days ahead as operational cost of the banking window is much, much lower than the traditional one," Ali said, adding that Bank Asia will disburse loans at 9 per cent from April through agent banking as per the government instruction.

At present, the lender is disbursing loans ranging from Tk 20,000 to Tk 200,000 to borrowers at an interest rate of 14-15 per cent through the channel.

The lower operational costs for agent banking will help Bank Asia sidestep the difficulties stemming from implementation of single-digit interest rate on lending.

As of December last year, loan disbursement by Bank Asia stood at Tk 259 crore, which is 58 per cent of the total outstanding loans given out by all lenders through agent banking.

Agent banking will get more popularity for loan disbursement in the coming days as rural people are often forced to take loans from non-governmental organisations and the informal sector at a high interest rate, Ali said.

"So, we have laid emphasis on disbursing loans by our agents so that underprivileged people can take their required loans at a cost lower than the rate offered by the informal sector," Ali added.

The central bank issued the agent banking guideline in 2013 but the licensees did not start full-fledged operations until 2016.

Agent banking offers limited banking and financial services to the underserved population by engaging representatives under a valid agency agreement.

It is the owner of an outlet who conducts banking transactions on behalf of a bank.

Agents provide services such as cash deposits, withdrawals, remittance disbursement, small value loan disbursement and recovery of loans, and cash payments under the government's social safety net programmes.

"The banking service has caught the attention of rural people very fast due to its hassle-free services," said Md Anwarul Islam, general manager of the Financial Inclusion Department of the central bank.

The Financial Inclusion Department is dedicated to monitoring agent banking.

"Customers initially faced some sort of confusion on whether the outlets actually ran banking services. But such ambiguity has been removed, which had helped agent banking to flourish."

Banks will introduce the electronic Know Your Customer (e-KYC) for agent banking soon, which will let clients open accounts within 5-6 minutes, he said.

"This will give further boost to agent banking," Islam added.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Outlets of agent banking distributed Tk 15,534 crore in remittance last year, up a staggering 180 per cent year-on-year.

Receivers of remittance usually go to their bank branches to collect remittance, but they can easily receive the funds from agent banking outlets that tend to be located adjacent to their home, said a Bangladesh Bank official.

Besides, for the lenders agent banking is a source of low-cost deposits: the cost of collecting deposits through the winder is 1-1.5 per cent lower.

"And people in rural areas mostly prefer savings accounts," he said.

As of December last year, 21 banks combined have 52.68 lakh accounts, up 114 per cent from a year earlier.

Comments