Savers, small borrowers pay price as banks run after high profit

With the financial sector being weighed down by huge excess liquidity, banks have cut the interest rates on deposits at a faster pace than on loans, penalising savers and, to some extent, small borrowers.

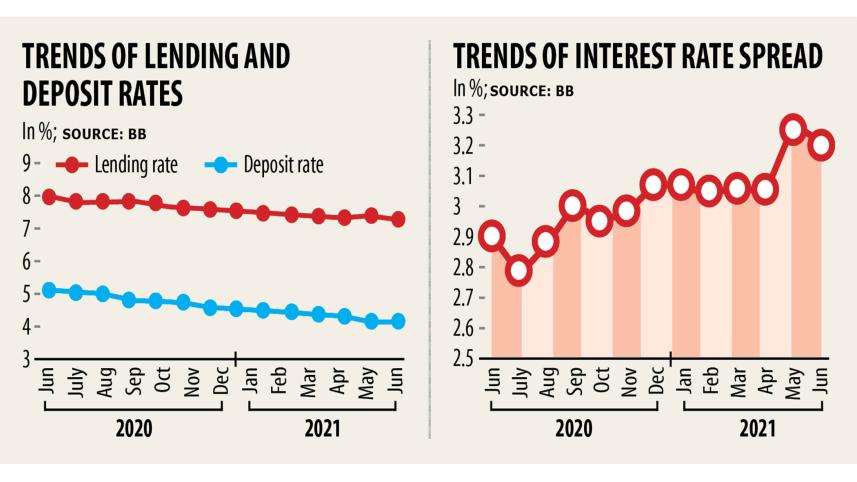

But the average spread, the difference between the lending rates and the deposit rates, widened over the last several months, meaning banks are punishing clients to ensure handsome profits and dividends for shareholders.

The weighted average rate on deposits stood at 4.13 per cent in June, down from 5.06 per cent a year ago, according to data from Bangladesh Bank. As a result, depositors are facing a negative return on savings given the inflation rate of 5.64 per cent in June.

The lending rate declined to 7.33 per cent in the month from 7.95 per cent a year ago.

Against the backdrop, the spread stood at 3.20 percentage points in June in contrast to 2.89 percentage points in the same month a year ago.

"The higher spread is not desirable at all as it is depriving the depositors of a scope to get a return on their funds kept at banks," said Salehuddin Ahmed, a former governor of the central bank.

"If we consider the inflation rate, the real interest rate is highly negative."

Most banks now offer an interest rate of 2 to 4 per cent on the fixed deposit receipts (FDRs), which result in a negative real interest rate of 2-3 per cent for savers.

The plight of the savers who have kept their money in the savings accounts is deeper than that of the depositors who opened FDRs as many banks provide less than 2 per cent interest rate on the former products.

"Banks in other countries are hardly following such a higher spread at this moment," Ahmed said.

"Although the main agenda of banks is to lend money, they are not doing so now. Rather, they are maintaining a lower interest rate on deposits and a higher rate on lending to make a hefty profit."

He urged banks not to adopt such a strategy in times of crisis as people's income had been hit hard because of the economic slowdown brought on by the coronavirus pandemic.

Ahmed Kabir, a retired schoolteacher in Cox's Bazar, said he was highly dependent on the interest income from the FDRs he kept with three banks.

"All of my FDRs have recently matured. I am now in a difficult situation to park the money as banks have cut the interest rate on deposits."

Abul Kashem Md Shirin, managing director of Dutch-Bangla Bank Ltd, said it was easier to cut the deposit rate than the lending rate.

"Depositors are not united. But borrowers make an all-out effort in case of an increase in the lending rate," he said.

He said the spread had helped banks post a robust profit in the first half of 2021 despite the business slowdown.

"The upward trend of the excess liquidity in the banking sector has mainly created the imbalanced situation," said Ahsan H Mansur, chairman of Brac Bank.

The excess liquidity in the banking system reached an all-time high of Tk 231,462 crore in June.

The stance adopted by banks has also had an adverse impact on small borrowers as they have little bargaining power to secure loans at a lower rate than the larger ones, according to Mansur, also the executive director of the Policy Research Institute of Bangladesh.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. "The large borrowers can borrow at a relatively lower interest rate by using their influence. Lenders usually do not pay attention to smaller borrowers."

The lending rate would go down if banks gave out loans as expected, he said, adding that this would also reduce the excess liquidity subsequently.

"The depositors will also benefit if the excess liquidity declines."

But the scenario may not change until the pandemic situation improves.

Although depositing money at banks now brings losses for savers, there are not enough options to invest and get an expected return.

The only safe option is savings certificates, whose interest rates can reach as high as 11.76 per cent.

As expected, the net investment in the savings tools has been on an upward curve. It stood at Tk 37,386 crore in the first 11 months of the last fiscal year, which is nearly four times higher than the same period a year ago, according to data from the Department of National Savings.

But the government lowered the maximum investment ceilings of three types of savings certificates on December 3 to get some respite from the burden of the high-cost borrowing.

The securities are the five-year Bangladesh savings certificate, the three-month profit-bearing savings certificate, and the family savings certificate.

As per the new rules, investors are allowed to purchase these savings tools of up to Tk 50 lakh under a single name and Tk 1 crore under a joint account, in contrast to Tk 1.05 crore and Tk 1.20 crore, respectively, in the past.

So, many depositors have had to go back to banks to keep their money despite the negative interest rate.

The stock market would have been one of the best options for the individual investors if there had been a strong structure, a BB official said.

"But people should stay away from the stock market as the excess liquidity has already created a bubble."

The private sector's appetite for credit was essential to boost the interest rate on deposits, said Syed Mahbubur Rahman, managing director of Mutual Trust Bank.

The credit growth stood at 8.40 per cent in the last fiscal year against the central bank target of 14.80 per cent.

The existing situation might not improve this year even if the central bank mopped up a portion of the excess liquidity, said Rahman, adding that the Covid-19 situation had become the critical factor in restoring business confidence.

Comments