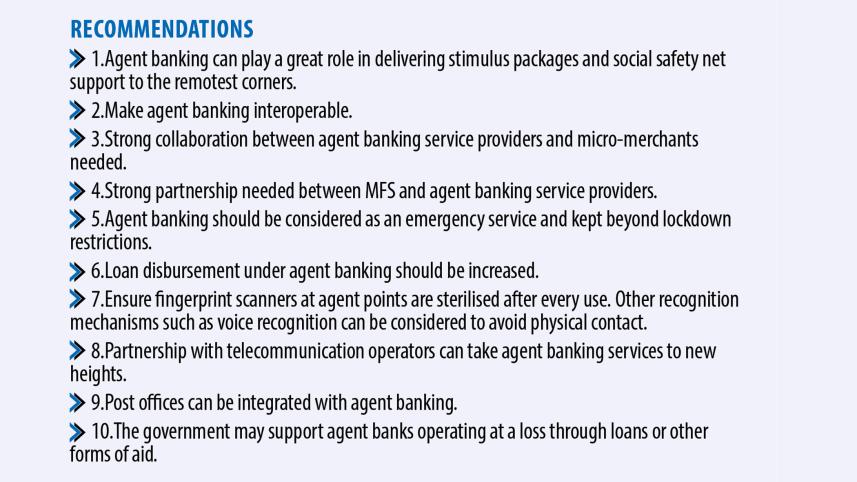

Agent banking solutions during coronavirus pandemic

Muhammad Zahidul Islam,

Senior Business Correspondent, The Daily Star and Moderator of the session

Agent banking is quite a recent addition to banking services but it has already made waves in our community in terms of user number, agent points, and number of transactions. There have been various responses from the banking sector in regards to how this banking channel can work in the present COVID-19 crisis. The exceptionally high participation of women is also an impressive aspect of agent banking.

The marginal population, who used to store their incomes at their homes, now prefer to deposit them at various agent points. Financial inclusion is improving and these people are also feeling more secure in regards to their finances.

Mashrur Arefin, Managing Director and CEO, The City Bank Limited

We can now operate only 30 percent of the 550 agent points across the country. Transactions at agent points have decreased from around 40,000 per month to now only 11,115 which is an almost 75 percent fall in transaction volume. A major issue is that the central bank has stopped all Real Time Gross Settlement (RTGS) banking. This is why banks around the country are now charging 0.25 percent for every amount over one lakh taka, which is much higher than the standard charge. The banks are also refusing to use Bangladesh Electronic Funds Transfer Network (BEFTN) since this requires 24 hours for them to receive the money.

There is a fear of COVID-19 transmission surrounding agent banking due to the use of fingerprint recognition. Therefore, it must be ensured that the fingerprint scanners at agent points are sterilised after every use.

The government has stated that if we keep our banks open then each permanent employee must be paid a COVID-19 allowance of 30,000 taka and contractual employees an allowance of 15,000 taka. Business is in a deplorable state right now so paying these amounts to employees to keep all 550 agent points open will cause operating expenses to shoot up by 25 percent, which is unmanageable.

Telco partnership was previously proposed to Bangladesh Bank by Bank Asia; however, this was not approved. If telecommunication companies like Grameenphone or Robi partner with agent banking, our services will reach new heights.

AKM Shirin, Managing Director and CEO, Dutch Bangla Bank Limited (DBBL)

We have around 4,100 agent outlets and some of these are in the most remote areas. Consequently, people are also sending a lot of remittance to these areas. Foreign remittances are being directly transferred to the agents and the customers are receiving it from them. They are also being given a card which can be used to take out cash from ATMs, free of cost. There are no liquidity issues here since if, for some reason, agent booths don't have enough cash, the customers can pick up their money from a nearby ATM or even a different bank branch.

Due to the fast growth rate of agent banking, around two-thirds of the agent points are incurring losses. We have employed various ways to try to increase profits and their income. One example is through the commissions given when foreign remittances are disbursed. When agent booths are set up, we also provide agents one lakh taka for furniture and decorations. We are also adding an extra one percent to the two percent remittance incentive that the government is providing the customers.

Since agent banking is a verified banking platform and is spread throughout all the rural areas of the country, it could be an effective and secure channel for transferring government allowances during this pandemic. Banks are currently operating in a limited fashion but agents are still operating from 8 AM to 8 PM. Hence, many customers have now opted for agent banking.

People working in agent banking are not bankers and so do not have bank IDs. Therefore, by Bangladesh Bank's orders, they are not exempt from lockdown restrictions. Consequently, they face many hindrances when attempting to open up their outlets. The agents could be provided with special permits that prevent them from facing such challenges.

Dr Nazneen Ahmed,

Senior Research Fellow, Bangladesh Institute of Development Studies

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. There are over 4,000 Union Digital Centres set up by our government and among them, 2,500-2,600 are active. Agent bankers can be found inside these centres and the advantage of this is when customers visit these centres for other purposes, they encounter the agent bankers in the same place and can receive their services.

In the current situation, not only receiving allowances but all other banking transactions has become easier due to the agent points. We need to ensure that all of these agent points are operating smoothly. Agent banking is also particularly helpful for female customers, especially the female-headed households, as they feel safer due to its location and convenience of use. For instance, they don't have to go to bazaars where they usually feel insecure and thus, obtaining services from Union Digital Centres is more beneficial. In future, we should try and ensure that every Union Digital Centre in Bangladesh has better accessibility to agent banking.

In regards to the current situation, the government is planning to provide monetary assistance to people and agent bankers, which can be highly beneficial. They can help identify the people who require such assistance and they can also help in double-checking their backgrounds. Since the government needs a proper list of people who are in need of assistance, the KYC form filled up by the customers can also be very helpful for verification.

Syed Mahbubur Rahman,

Managing Director & CEO, Mutual Trust Bank Limited (MTB)

Despite keeping our agent points open in many locked down areas, our daily transactions have gone down from around five crore to 1.5 crore taka. Therefore, government support is very important here.

Public banks are being used to disburse various kinds of allowances right now. Disbursing more of these allowances through agent banking is a good option as they can provide greater transparency and customer support, since the agent booths have continuous supervision.

Electronic Funds Transfer (EFT) has been cut down from 25 to only 10 transactions per day now. This transaction number needs to be increased. Besides, if we get permission, then we can create a system where, if consumers buy savings certificates from banks, their profit can be linked to agent banking corners.

The verification process of agent banking has been under scrutiny due to the outbreak since it requires fingerprint identification. So, we are trying to look into face and voice recognition technology. We are also using biometrics. We have been able to give out roughly 150 crore taka as loans though we are supposed to give more. We get complaints that we only take deposits from rural areas but don't give out loans there but the problem is that our chances of obtaining returns after giving out loans are low in these areas. Therefore, we are working with small loans in the rural areas.

Interoperability is another area that can be explored to make agent banking more popular. Besides, if we can convince corporates to get involved in this arena, it would increase the credibility of the agent banks. Insurance companies can also become partners of agent banking. In this way, we can reduce operating costs and increase the profits of our agents.

Md Arfan Ali, President and Managing Director, Bank Asia Limited

Fund transfer through bank-to-bank account is now possible via Bangladesh Bank using RTGS or BEFTN platform. Since mobile banking operation is increasing rapidly, the banks can access each other's accounts by using different fund transfer methods offered by the payment system of Bangladesh Bank. The work that Bangladesh Bank was doing on National Payment Switch Bangladesh (NPSB) should be emphasised on. In this way, any bank accountholder, be it in agent banking or big bank branches, can transfer funds to any bank account in Bangladesh.

We have also established connections with MFS such as bKash. Such partnerships are increasingly required to meet the government's target of financial inclusion programmes. Since we have an established set up of agent banking, everyone should think of optimising resource utilisation in this moment of crisis. We can achieve it by assessing how much work we can do to provide adequate services with our existing agent banking. Through various partnerships among the relevant service providers, social safety net, remittance, utility payment settlement and other small transactions can be done efficiently.

We are disbursing salaries of around 35,000 RMG workers through our agent banking services. Most of the RMG owners have not expressed their interest fully to provide bank accounts for their workers since they were not keen to disburse salary in bank accounts. However, we can move forward now bearing in mind that a bank account is everyone's right and thus one should be able to receive all the associated services. In line with the spirit of National Financial Inclusion Strategy, we need to work together to ensure that each village of the country has a financial kiosk and every adult has a bank account.

Dr Khondaker Golam Moazzem, Research Director, Centre for Policy Dialogue (CPD)

Regarding the COVID-19 situation, there were instructions from the government that the agents will receive some incentive upon starting their services from their respective banks. Such an initiative might prove to be burdensome for banks. However, to tackle this, CPD is trying to bring out a proposal for the government to include in its upcoming budget, where it explores if it is possible to provide tax exemption to all those companies that are undertaking emergency initiatives despite pressure or losses during the COVID-19 crisis.

Since remittance is a big source of deposit collection in agent banking, it will continue to remain this way in the future. So far, agent banking has obtained around 15,500 crore taka. A part of this amount is with banks as loans or deposits. Banks can explore if loans can be provided with easier conditions to those who previously used to send money through agent banking services from abroad and have now returned to the country by leaving those jobs as these people will not be able to return to their jobs anytime soon. The government has created a pool of 200 crore taka for these people but that fund will not suffice.

Dr Ahsan H Mansur,

Economist, Executive Director-Policy Research Institute and Chairperson-BRAC Bank

The banking sector will face a huge blow this year and the number of write-offs or non-performing assets will increase in both the RMG sector as well as in the SME sector at a larger scale. Therefore, the government should implement a risk-sharing arrangement for the banking sector. Risk-sharing is required because we cannot compare the low interest rate in risky areas, where the operation costs are high, with corporate lending at nine percent. If the government and Bangladesh Bank mitigate the default risk then lending operations can continue, be it through agent banking or SMEs.

Microcredit institutions and banks will be competing in the same area and only the most competent ones will survive. So, I believe a lot of microcredit institutions will be wiped out in the future. Banks will be there because there is money to be tapped into. Everyone will now focus on how remittance can be capitalised and how money can be retained through agent banking and other means. We have potential in these areas. Also, since our rural areas are expanding and becoming financially solvent, banks, as well as agent banking, will definitely tap into that area. This is not much of a good news for the existing players in those areas but they have to change their modus operandi to enhance their competitiveness.

We are not investing in new brick-and-mortar. We are working with those agent banking services which already have existing establishments and with those who don't have establishments but are willing to carry on without setting up new establishments. In this way, we are being able to achieve cost efficiency.

Md Abul Kalam Azad,

Former Principal Secretary and Principal Coordinator of SDGs

Amidst the coronavirus pandemic, some sectors, such as agent banking, MFS, e-commerce, telcos, have gotten the opportunity to work their way up and help people to tackle the crisis. There is more scope for improvement and we should look into how we can achieve it.

Financial inclusion is a big component of the SDGs. Bangladesh has around 8,500 post offices. If we can utilise this platform by connecting it with agent banking, then I believe, people's faith will increase.

Though there are limitations for selectively channelling the loan packages by the government, we can help them reach doorsteps through agent banking services.

Since the banking sector is working hard to give services to people, Bangladesh Bank can look into the factor of risk-sharing more profoundly. I believe, agent banking is playing a significant role to promote women's empowerment and the economic development of the rural areas.

Dr Atiur Rahman, Professor, Department of Development Studies, University of Dhaka and Former Governor, Bangladesh Bank

Bangladesh Bank had launched a small-scale credit guarantee scheme with only two crore taka from the United Nations Capital Development Fund (UNCDF). There is scope for expanding this credit guarantee scheme with 200 crore taka from the budget while keeping SMEs as the core focus. If 80 percent of loans can be brought under the credit guarantee scheme, then banks will be more secure in giving out small loans.

Bangladesh Bank has already taken some great initiatives in terms of stimulus packages. One such initiative is the 20,000 crore taka SME loan offering through banks which will be refinanced by 50 percent. I believe this should be refinanced by 100 percent since bringing down costs is required due to the additional risk in this field. Another offering is of 3,000 crore taka through MFIs, without refinancing. This can be increased further, even though this will be renewed automatically.

There are around 800 micro-merchants currently working. If agent banks work with these micro-merchants, an e-commerce platform can be created. If we make account payments through micro-merchants who can then deliver products and services, this would become a great e-commerce platform in the rural areas or in semi-urban or small urban areas. Government stimulus package distribution can also be done through agent banking.

Agent banking is also mobilising savings. 28 percent of women have opened accounts in agent banks and are taking various kinds of small loans. Special initiatives can be made for women entrepreneurs.

The number one target of next year's budget will be healthcare, followed by food security. Therefore, the social safety net coverage will have to be doubled. Agent banking can play a crucial role here since there are now more agent outlets than bank branches, and the number of outlets is increasing.

It would be beneficial if our national payment switch could be turned into an interoperable service. If other mobile financial services such as Rocket step forward the same way that bKash has in their work with banks, then forming an interoperable service would become a much quicker process.

Muhammad Abdul Mannan,

MP, Honourable Planning Minister

Since agent banking does not involve a large gathering of people, it aligns with the COVID-19 guideline of avoiding crowds. Hence, we are trying to promote agent banking even further during this time. It is disheartening to hear that some agents have faced unfair restrictions while trying to set up outlets, but hopefully, this issue will be resolved soon.

Ideally, economic actors should discuss solutions to their issues amongst themselves. The regulators should only be involved for taking the final formal steps required to mobilise changes. I believe mobile banking now requires the least interference by regulators. Bangladesh Bank and agent banks can work together to figure out how to cover the losses sustained by the agent banks. The government may support agent banks operating at a loss through loans or other forms of aid.

Microcredit operators, or NGOs, have immense experience in the field of rural financing and have connections with millions of people. Agent banks should collaborate with these NGOs to attain mutual benefits. Interrelations between different financing systems are required.

Services must be made user-friendly for uneducated groups in rural areas so that they understand that they are also capable of availing these services. Additionally, user forms must be simplified using accessible language. Use of continually evolving technology in these services is essential, and proper training must be provided to all employees as well.

Bangladesh Bank has expressed dissatisfaction about only 28 percent of females having deposits in agent banks, but I think this is still a big step in the right direction. The focus should not be on the number of deposits, rather on their quality and weight.

There is excellent scope for agent banking in terms of remittance. Remittance is a very valuable and vast flow. Bangladesh Bank and the Ministry of Finance will look into how to strengthen the use of agent banking in this regard.

Comments