Banking sector for sustainable growth

Bangladesh's financial sector is dominated by the banking sector. The dominance of the banking sector makes the financial sector vulnerable on the one hand, but highlights the crucial importance of the sector in resource mobilisation and economic growth, on the other. The role of the banking sector in accelerating growth is contingent upon the soundness and depth of the sector. In Bangladesh the banking sector has travelled through a journey where the sector has experienced several ups and downs. Reforms measures have been undertaken in an attempt to improve upon the structural constraints of the sector.

Such measures have been driven by objectives such as increasing the capital adequacy of banks, streamlining guidelines for rescheduling of various types of loans, tightening provisions for non-performing loans, strengthening disclosure requirements and improving accounting system. These have undoubtedly improved the soundness of the sector over the years. However, the performance of the banking sector in the recent past has not been satisfactory. At present, key performance indicators of commercial banks in the country reflect the poor health of banks. Most banks have not been able to show significant improvements on indictors such as capital to risk weighted asset, non-performing loans, expenditure-income ratio, return on asset, return on equity, liquid asset and excess liquidity despite several measures taken by the central bank.

Since large financial irregularities in Sonali and BASIC banks, monitoring and inspection of Bangladesh Bank have increased. The central bank has also appointed observers in 14 banks and financial institutions, both state-owned and private to check further deterioration of these banks and supervise closely to improve their governance.

The results, however, are yet to show up in the performance indicators of these banks.

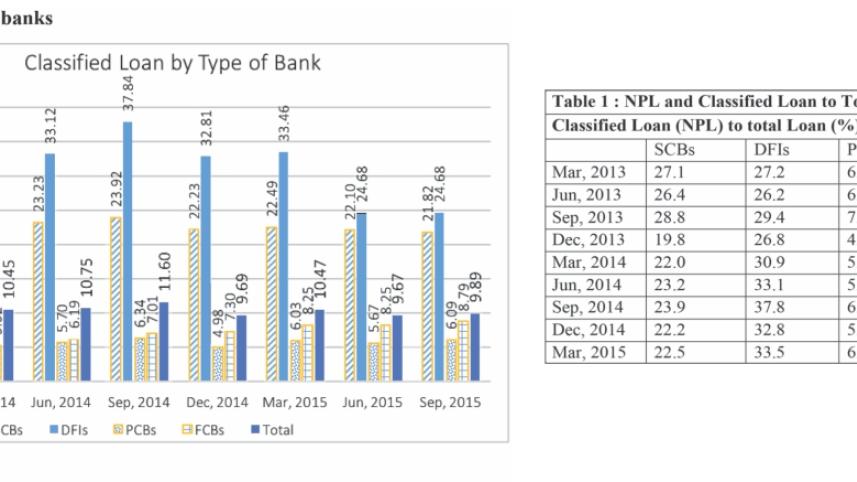

Profitability, measured by return on asset and return on equity, has been negative for the state-owned banks (SCBs).For private commercial banks, though these indicators are positive, but very low. In case of non-performing loans (NPL) similar performance is observed. Though the share of NPL to total loans in SCBs has slightly declined in September 2015 from June 2014, the rate is still as high as 21.82%. On the other hand, NPL in private commercial banks (PCBs) and foreign commercial banks (FCBs) have increased. Because of high NPL, state-owned banks have to make larger provisions. The government has to inject capital into these banks to keep them going. Clearly, implementation of BASEL III requirements that call for capital adequacy ratio to be raised to 12.5% of their risk-weighted assets by 2019 will be challenging for the SCBs. As of September 2015, capital adequacy ratio of SCBs was only 6.2%.

Lower profits in SCBs are mainly due to bad assets, inefficiency and political interference. In case of PCBs, stricter compliance requirements by the central bank and low appetite for credit by the private sector due to sluggish business environment are the major reasons for lower profits. This is reflected through high volume of liquidity in banks. The advance-deposit ratio has been little over 70% in November 2015 even though banks are allowed to lend up to 80% of their total deposit.

Despite anaemic performance of the sector, governance in banks still remains a distant reality. Concerned authorities have been slow to take action against the identified people for embezzlement of money from banks. The Hallmark group has not returned any money to the bank till now. More frustrating is that bank authorities do not even expect to get back the misappropriated money. These incidences have affected the effectiveness of various measures taken to improve the governance of the banking sector. Flexible measures, including loan rescheduling policy favouring powerful people and lack of punishment for fraudulence in banks have worsened the situation. The oversight mechanism has clearly been less effective.

Shocks in the banking sector and emerging challenges require further reforms for improvement of governance in the sector. In view of this there is a need for setting up a commission for the financial sector. The commission will scrutinise the overall performance of the sector, assess the need of customers and the economy, identify the current problems and emerging challenges and suggest concrete recommendations for prudential banking to be implemented in the short to medium terms. Considering the emerging need and in order to build up more transparent and responsible banking sector the commission can also include non-bank financial institutions, such as insurance companies and capital market under its jurisdiction as they are interconnected.

Recently, there has been some discussion at the policy level as regards setting up a 'Financial Sector Commission' for the improvement of the sector. Hopefully, this will take off soon. The broad terms of reference of the commission should be to critically assess the problems and weaknesses of the banking industry in order to find whether there is any disconnect between demand of the growing economy and the realities of a back dated financial system that is failing to meet the emerging need. On the basis of a comprehensive scrutiny, the commission will prepare guidelines and make recommendations as regards automation, risk management, internal control, the role of various players in banks and other financial institutions. In 1998, a Commission on Banking and in 2002, a Banking Reform Committee were formed to make recommendations for the improvement of the performance of banks.

The banking sector has achieved considerable success due to the reforms in the 1990s, 2000s and afterwards. However, the sector will have to prepare for the next generation of global regulatory framework and meet emerging clients' needs. In the coming days, the banking industry will have to achieve the ability to absorb shocks arising from financial and economic stress, improve risk management and governance, and strengthen banks' transparency and disclosures. And if the sector has to play the larger role of contributing towards a stable and sound macroeconomic situation, the banking sector has to go through the painful path of stricter policy and legal measures.

The writer is Research Director, Centre for Policy Dialogue (CPD).

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments