Shift from West to East

Stephen Green

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Our industry is going through a crisis the like of which none of us has experienced before. Many people are asking if this is the worst financial crisis since 1929. It probably is. Is it the most complex financial crisis the world has seen? Certainly, it is. Will it usher in a recession? I'm afraid this seems inevitable. Indeed, although the economic data lags the facts on the ground, it seems likely that the UK and a number of other economies are already contracting. These risks are creating a further phase in which conventional credit impairments rise as a result of recession.

As the crisis has intensified, so has the analysis of the causes behind it, which are complex.

Many factors have contributed to the financial crisis. Some of the most significant … but this is by no means an exhaustive list… include:

The explosive growth of subprime lending, notably in the US. Eighteen months ago, subprime was the main villain; today it has been subsumed by the wider crisis, and appears half-forgotten. Yet it was the downturn in the US housing market, and the pressure that put on less well-off homeowners that triggered the start of this crisis.

Subprime is, however, far from the only villain in town. The complexity and opacity of certain financial instruments reached a point where even senior and experienced bankers had trouble understanding them, let alone investors. This meant that people were selling and buying assets whose risks they had not properly assessed.

On top of that, these assets were created on the back of ever-higher leverage, both direct and indirect. And when the securitisation market began to collapse, banks found themselves with assets that they could neither sell nor fund, so creating large losses on the asset side and a funding stretch on the liability side for which they were entirely unprepared.

In several markets there was an over-dependence on wholesale funding, based on the assumption that funding would never dry up -- an assumption that has proved fatal to some once distinguished names in banking.

Finally, weakening economies and declining asset values, particularly housing, risk feeding back into lower asset quality more generally, giving rise to further impairment charges.

Each of these factors has undoubtedly contributed to the breadth and depth of this financial crisis.

However, something even more fundamental is underway in the world economy, of which this crisis is a manifestation and on which we need to focus if we are to understand its real significance. And to understand this, we need to take a step back and consider the global macro-economic context.

The principal feature of the global economy in recent years is that it has become something of a perpetuum mobile. In the post-war period there has been an increasing interdependence between national economies, on the back of falling trade barriers and freer capital flows.

The post-war recovery of Germany and the rise of Japan foreshadowed the rise of dynamic Asian economies such as Hong Kong, Korea and Taiwan, the so-called newly industrialised countries. And of course, in the last 20 years, the economic renaissance of the world's two largest nations -- China and India -- has changed the landscape still further.

We have also seen the rapid rise of resource-rich nations, primarily energy-producers, thanks to the growing demand for oil and other minerals.

Meanwhile, in mature economies the consumer has become king. Consumption in western markets has been the main driver of economic growth over the last few years, funded by exceptionally cheap borrowing, made possible by savings surpluses built up in the developing world.

These changes to the economic landscape have effectively created an economic triangle. On one side, those economies that are the workshops of the world, most of which are relatively resource-poor. On another side are the resource suppliers, notably the Middle East, which produces almost a third of the world's oil and will produce an increasingly significant proportion of the world's gas as well.

And on the third side, you have consuming nations with low savings ratios particularly, of course, the US, which has become what you might call the “spender of last resort”.

This triangle has sustained high rates of world economic growth, but it has also helped create huge, and growing financial imbalances. The newly industrialised countries -- the workshops of the world -- with their high savings rates and low exchange rates have built up massive currency reserves.

So have the resource-rich exporters, where in many cases a combination of small populations, and until recently strong global demand for oil and high energy prices, has created surplus liquidity which is available for investment in international markets in one form or another.

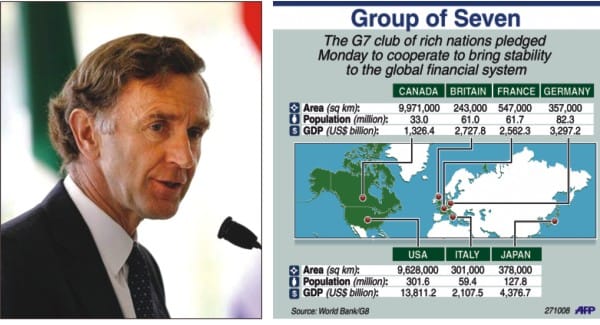

Meanwhile, counterbalancing these surpluses have been the consumers of the developed world, where debt has grown exponentially among consumers. In the UK, for example, the ratio of debt to income reached 173 percent this year, up from 129 percent five years ago, and higher than any other G7 economies.

These factors have been accompanied by increased financial market leverage. Why? Again, there are multiple reasons.

Primary among them, the search for yield among investors. The equity collapse at the beginning of the decade prompted institutional investors to move out of equities and into fixed income investments. But the bond markets were drawing in surplus liquidity from emerging markets -- over 50 per cent of US treasury debt is now owned by foreign investors -- significantly reducing bond yields. Mortgage backed securities seemed to fit the bill of higher yields with limited risk that was sought by investors. This in turn stimulated huge growth in these securities, and also changed the funding model for banks. In 1990, just 10 percent of mortgages in the United States were securitised, compared with 70 percent in 2007.

And in general, the liquidity build-up served to artificially compress risk spreads, fuelling asset price inflation, especially in real estate, that eventually became a bubble.

Even at zero growth rates, the imbalances in the real economy would have led to an increase in assets and liabilities. And at high growth rates, the after-burners were well and truly on.

The combination of a tidal wave of liquidity and the search for yield produced rising risk or reward ratios, with investors moving up the scale, even as the scale itself was rising.

So the effect of this macro-economic triangle was to make the financial markets intrinsically and increasingly unstable. And on top of this, global monetary conditions contributed further to instability.

The period of loose monetary policy between 2002 and 2004 offset the corporate deleveraging that had followed the dot com bust and 9/11 by encouraging increased consumer leverage.

The tendency for emerging markets to run monetary policies explicitly or implicitly tied to US policy, because of their foreign exchange policies, created the scope for loose monetary conditions to spread globally.

This reduced the cost and the risk of investing surplus liquidity in the US dollar, thus feeding what would become a spiral of cheap credit, rising asset prices and high consumer borrowing.

The blow-up was inevitable and has been very painful.

And as in previous crises, the specific trigger for today's crisis, subprime, has become relatively less important as the crisis unfolds.

Now the principal concerns are about the massive breakdown in confidence and trust that has led to market failure, manifested by the system-wide “wholesale bank-run” which has clogged the inter-bank markets and turned the bursting of an asset price bubble into a full-blown liquidity crisis. And so we arrive at today's situation where governments have been forced to guarantee term lending, to inject huge volumes of liquidity into the system, and to recapitalise many financial institutions, becoming potential or actual “owners of last resort”.

“This too shall pass,” as the saying goes. But there will be no return to the status quo ante. There are many lessons for banks, regulators, investors, monetary authorities, accountants and consumers to learn from this crisis.

The high-leverage model of finance is bankrupt. But securitisation will survive. You cannot bring the whole of the world's capital markets back on to banks' balance sheets.

Comments