Stocks, Sox and avoiding DSE investor shocks

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. There has been a great deal of focus in recent weeks on the sell-off in the DSE and whether the bull market for stocks is over or we are just in the midst of a more protracted correction. Rather than assess the near-term prospects for the stock market, in today's column, I wanted to highlight the critical role the stock market could play in offering an alternative, and likely cheaper, source of financing to companies to bank borrowing along with the necessary financial reforms to achieve this.

The stock market should be one of the primary mechanisms by which savers or investors, those with excess capital, provide financing to companies who have a capital deficit. One way of considering the valuation of an individual stock is as a claim on the future earnings of a company discounted for the value of time. The level of stocks is also affected by broad liquidity conditions in the economy, the level of interest rates and the macroeconomic outlook (which clearly affects the earnings outlook).

The level of individual stocks will also vary with investor expectations on the prospects for individual companies earnings as well as those for their sector overall. A well functioning financial system should also see equity investors play an important role in terms of market discipline rewarding the management of those companies who deliver good earnings growth/strong dividends growth and punish those companies who misuse or ineffectively use capital.

If the stock market is working effectively, it should also reward those companies with good corporate governance, openness and transparency by awarding them a premium in terms of higher price earnings (P/E) ratios.

On the other hand, the market should punish the management of companies who not only operate poorly in terms of generating earnings or the return on capital but also give investors either misleading or inaccurate information. This risk premium would be manifested in a valuation discount or low P/E versus other more transparent companies in the market.

An important role for stock market regulators is to ensure that there is transparency and a level playing field in the market, and that either companies or large investors do not trade on inside information. In increasingly complex markets, this requires substantial investment in market-monitoring technology. They also need to ensure that companies that raise capital in the market for the first time in an Initial Public Offering (IPO) do so on the basis of honest and accurate information about the state of the company's finances/balance sheet as well as the current and future prospects for the basis. A key role for market regulators should also be to ensure that companies ongoing reporting of their financial results is honest.

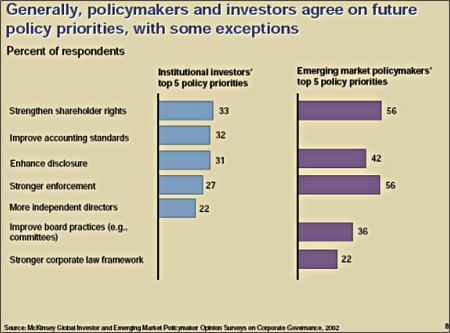

In terms of assessing what market reforms are considered priorities in other developing markets, it is worth considering two surveys done by consulting firm McKinsey and Co of both 40 policymakers from 20 countries as well as 201 investors from more than 30 countries. Although the survey was done in 2002, the results are still relevant for an emerging capital market like Bangladesh.

McKinsey notes governance reformers need to devote more emphasis to driving change through institutional reform of capital markets - and the underlying structure of property rights - to complement practical improvements to governance at the corporate level.

Secondly, the importance of family owned businesses in emerging markets should be recognised more explicitly. Without incentives to change, they could continue to act as a major obstacle to reform. Institutional reform could provide some of these incentives. Enabling family owned businesses to adopt a sequence of incremental changes could help them share in the benefits of reform.

As I have highlighted above, if Bangladesh is to develop an effective capital market, where valuations are driven by economic and corporate fundamentals, it is important for the regulators to ensure that companies report genuine financials and on a timely and systematic basis. Any lack of transparency or honest accounts will undermine both investor confidence and the effective functioning of the market.

As there is greater fundamental research in the marketplace, Bangladesh also needs to develop a framework to avoid analyst conflicts of interest. A lack of fundamental analysis is a recipe for a speculative capital market that is news-driven and an inefficient allocator of capital to the corporate sector. But one needs to recognise the need for effective regulations to avoid market manipulation and insider trading.

The United States, the largest and most sophisticated economy and capital market in the world, suffered accounting scandals as recently as 2002. Worldcom overstated its results by $ 3.9 billion resulting in bankruptcy. Energy trading giant Enron suffered a similar fate. This followed the bursting of the Tech bubble in 2000 when many internet stocks were artificially boosted by analysts publishing glowing reports that exaggerated the positive fundamentals to get more investment banking/IPO business for their capital markets decisions.

As a result, the US Congress passed a bill, Sarbannes-Oxley (popularly known as “SOX”).

Among other things, it established the Public Company Accounting Oversight Board, to provide independent oversight of public accounting firms providing audit services ("auditors"). It forced company CEOs and auditors to personally sign and imposed substantial penalties for false reporting or manipulation of accounts. It also legally mandated substantially greater resources to the SEC to ensure they had the capacity to enforce the more complex rules.

The arrival of the Grameenphone IPO and the prospects for a number of large issues in the pipeline from telecoms, privatisations and infrastructure all bode well for the growth of the capital markets. But more significant progress in corporate governance and accounting transparency is an important objective for both the current and the next government. It may be time for Bangladesh to consider its own version of SOX.

Comments