What is needed for sustaining high growth in Bangladesh?

We know from growth accounting that GDP growth can be broken into growth in the labour force and growth in labour productivity. Growth in the labour force is largely determined by the stage of demographic transition, the labour force participation rate and net immigration.

Growth in labour productivity comes from improvement in the quality of the labour force (human capital formation thru education and skills development), increase in capital per worker and increase in the overall efficiency of production (often called TFP, total factor productivity). Technological progress and improvement in resource allocation between sectors underpin TFP growth.

The empirical literature on economic growth is vast and diverse. Yet, in developing countries, there always is a disconnect between academic interests and the needs of policy practitioners. The focus of the literature on the very long run and on the incentives for expanding the technological frontiers is not as exciting as insights on accelerating short-to medium-term growth by catching up with already known innovations.

A very readable piece in February 2018 on The Financial Express titled “Why investment and productivity is key to India’s GDP growth” by Samiran Chakraborty, chief economist of Citigroup, analyses annual growth data in a panel of 26 developed and developing countries from 1950 onwards.

This piece identifies threshold levels of growth in labour productivity, investment and TFP as the key drivers in most cases of sustained high growth. The exercise is extremely useful for putting into context the growth aspirations of an emerging economy like Bangladesh.

It helps get a sense of what would it take to accelerate and sustain growth to levels such as 8 percent plus, as envisaged in the government’s Medium-Term Macroeconomic Policy Statement 2019-20 to 2021.

Labour productivity growth was more than 6 percent in 75 percent of cases where GDP growth exceeded 8 percent. Labour productivity growth below 6 percent keeps GDP growth below 8 percent. Note that labour productivity shortfalls explain 80 percent or more the per capita GDP gap with the United States (US) for most Asian countries.

Growth of per-worker GDP in Asia outstripped that in the US, allowing catch-up. The low-income countries experienced a labour productivity growth spurt in 2010-2015. Mongolia achieved the fastest labour productivity growth of 7.7 percent on average per year, followed by China’s 7.2 percent, the Lao PDR’s 6.9 percent, Sri Lanka’s 5.7 percent, India’s 5 percent, and Cambodia’s 4.9 percent, according to APO Productivity Databook 2017.

Labour productivity growth in Bangladesh approached 6 percent only in 2018. It was below 4 percent as recently as 2013 and varied between 5 to 6 percent during 2016-18.

Growth in labour productivity depends on capital deepening and growth in total factor productivity. An 8 percent GDP growth rate was associated with more than 10 percent growth in investment in that year in 45 percent of the panel data points analysed by Samiron. If investment growth is even slightly lower, say between 8 and 10 percent, the possibility of 8 percent GDP growth falls dramatically.

Net investment increases the physical capital stock, thus resulting in a high correlation between long run economic growth and high rate of net investment. Japan, South Korea, China, Indonesia, Vietnam and Singapore managed to have 10 plus percent annual investment growth for decades.

India struggled between 5 to 8 percent annual investment growth between 1950 and 2003 when GDP growth ranged between 3 to 7 percent. Investment growth averaged 11 percent during 2005 to 2011 taking Indian GDP growth to 8 plus percent before it slowed again to below 7 percent after 2011 when investment started moderating.

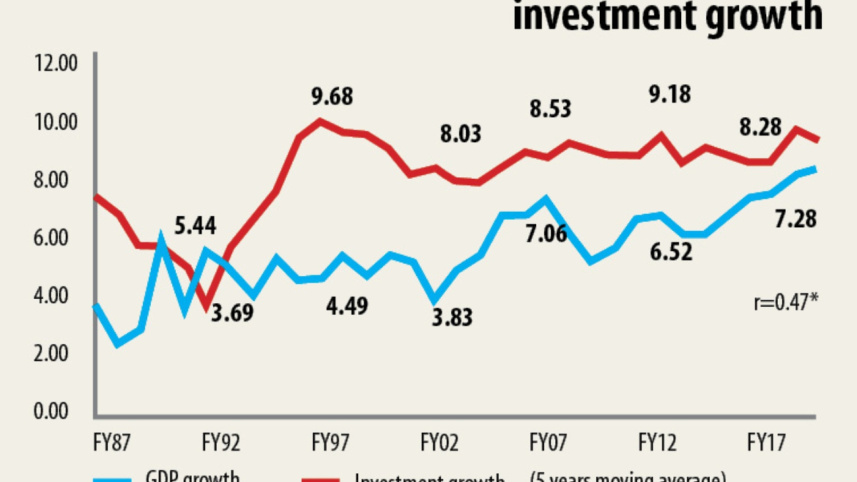

Investment growth in Bangladesh exceeded 10 percent on an annual basis only in 2018. There is statistically significant correlation between the five-year moving average growth rate of real investment and the GDP growth rate in Bangladesh.

TFP growth comes from technological upgradation and improvement in resource allocation between different sectors of the economy. In Samiron’s sample, 60 percent of economies experiencing more than 8 percent GDP growth had TFP growth of 3 percent or more. Anything less was associated with GDP growth ranging between 3 to 7 percent.

A recent survey by the General Economics Division finds around 1 percent TFP growth in Bangladesh historically, well behind India, China and Vietnam.

Low production efficiency has been a major drag on growth in Bangladesh. Capital per worker (in real terms) in the large and medium establishments increased 9.9 percent annually while that in micro and small enterprises increased 2.6 percent between 2013 and 2019 (according to BBS Survey of Manufacturing Establishments 2019), but this apparently had no impact on raising the trajectory of TFP growth.

In India labour intensive growth until the 1980s gave way to a more capital-intensive growth with TFP sharing the burden. Resource misallocation resulting from distortions in the policy environment can perhaps explain why this was not the case in Bangladesh, but that is a story for another day.

What drives production efficiency? Samiron’s piece misses a crucial piece of the puzzle by not paying any attention to the relation between trade and growth. Sustained positive economic growth has often been accompanied by even faster growth in global trade in most high growth countries most of the time.

Country-level data from the last half century shows countries with higher rates of GDP growth also tend to have higher rates of growth in trade as a share of output. Competition, economies of scale and learning and innovation are among the potential growth-enhancing factors that come from greater global economic integration.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Firms failing to adopt new technologies are more likely to fail; firms exporting to the world face larger demand, enabling them to operate at larger scales where the cost per unit of product is lower; and firms that trade gain more experience and exposure to upgrade technologies and industry standards from foreign competitors.

The World Bank’s Commission on Growth and Development in 2008 provided a cautious assessment of how exports should be promoted while underlining its role as a critical ingredient of high growth.

Governments look for ways to diversify exports and generate productive jobs in new industries. Experience shows these efforts should be subject to certain disciplines. They must be temporary, because the problems they are designed to overcome are not permanent; they should be abandoned quickly if an export industry cannot keep going without them; and they should remain as neutral as possible about which exports. Also, export promotion without supportive ingredients such as health, education, infrastructure and predictable regulation cannot take the economy too far ahead.

Evidence on growth convergence provides a strong basis for hoping that Bangladesh will grow faster in the days to come. In Samiron’s sample, countries with 8 plus percent GDP growth had less than 5,000 in purchasing power parity (PPP) adjusted dollars per capita income in 33 percent of the cases with another 28 percent below 10,000 PPP dollars.

This implies Bangladesh can have strong growth to reach upper middle-income status by mid-2030s. It’s per capita GDP of around 3,900 in PPP adjusted dollars is well below the threshold beyond which sustaining high growth becomes very difficult.

However, convergence is not like a natural law that always applies to all countries. The number of low per capita income economies stuck in a low-level growth trap is not insignificant. Bangladesh is still short of meeting the thresholds for sustained 8 percent plus GDP growth on all three fronts: labour productivity growth, investment growth and TFP growth.

The World Bank’s South Asia Economic Focus (April 2019) found Bangladesh’s potential exports are 2.3 to 2.7 times larger than the actual. It is therefore vulnerable to the perils of being trapped unless it corrects resource misallocation and balances tangible capital accumulation with skills and innovation.

The author is an economist.

Comments