Govt has a new headache. It’s the high interest rates on T-bills and bonds

The interest rate on government Treasury bills and bonds, the main instruments for bank borrowing, doubled in the last one year -- a development that will fuel budgetary expenditure and may discourage private sector credit, both of which are already sources of concern.

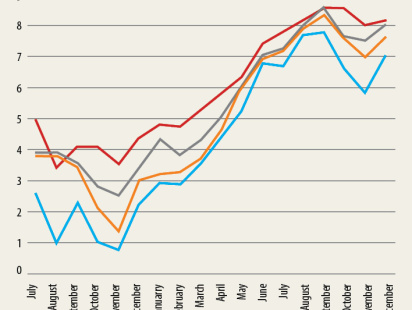

Yields on Treasury bills and bonds have increased by 3 to 5 percentage points in the last year and a half. They now range between 7 to 9 per cent depending on the tenor of the instrument, according to central bank statistics.

For one-year Treasury bill, the weighted average interest rate was 3.40 per cent in December 2018. A year later it was 8.04 per cent.

The two-year Bangladesh Government Treasury Bond, another borrowing instrument, had interest rate of 4.33 per cent in December 2018, which soared to 8.80 per cent.

The high interest rate of Treasury bills and bonds tempted banks to be conducive towards the government’s huge bank borrowing demand.

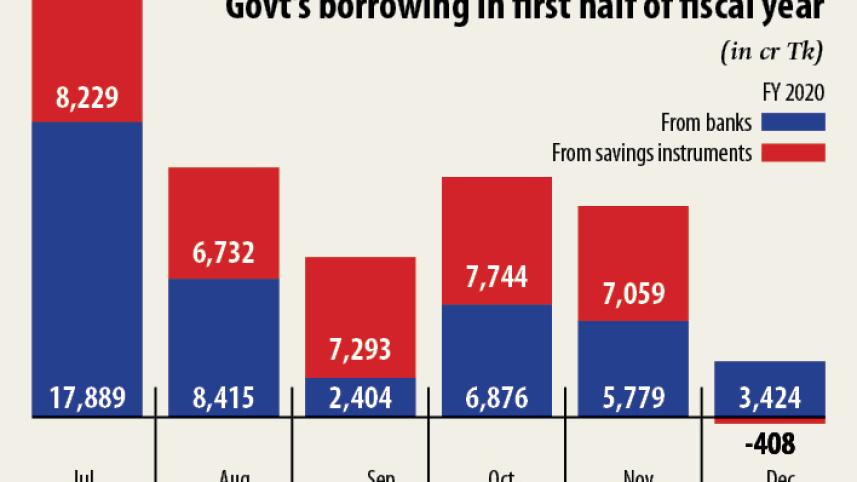

In the first half of the fiscal year, the government’s domestic borrowing reached Tk 49,020 crore, which is 63 per cent of the full-year target.

The government set a target to borrow Tk 77,363 crore from domestic sources in fiscal 2019-20 to meet the budget deficit.

Interestingly, the borrowing from savings instruments declined as the government has taken various measures to ward off savers to reduce the interest burden as well as shift the public money to banks.

Net borrowing from savings instruments in the first half of fiscal 2019-20 was eight times lower at Tk 3,257 crore from a year earlier, according to data from the Bangladesh Bank.

In December last year, the government did not borrow any money from savings certificate; rather it made repayment of Tk 408 crore.

But the government’s choking of savings instrument sales had the desired effect.

On Thursday, Finance Minister AHM Mustafa Kamal told the parliament that there was no liquidity crisis in the banking sector.

The scheduled banks have extra liquidity even after keeping essential cash reserve ratio and reserving the required statutory liquidity ratio.

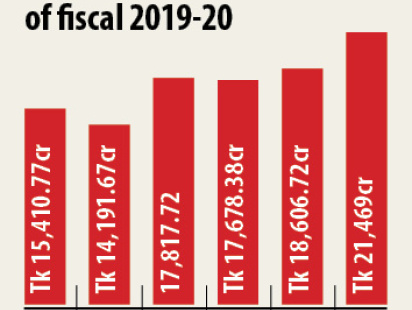

The amount of such liquidity increased to Tk 106,101 crore in December last year from Tk 67,601 crore at the beginning of 2019.

A recent study of the International Monetary Fund also attributed the declining saving instrument sales to the higher liquidity in banks.

It was also the cause, along with low revenue collection, for the spike in public sector borrowing.

In the first six months of the fiscal year, the government’s bank borrowing increased eight times to Tk 43,587 crore, according to central bank statistics.

Earlier, the IMF and the World Bank suggested the government to reduce borrowing from savings certificate due to high interest rates: about 11 per cent.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. But the recent high interest of Treasury bills and bonds suggests a similar problem has been created: it fuel the borrowing cost of the government through the banking system.

Not just that, banks will be tempted to lend to the government instead of the private sector because of high interest rates of Treasury bills and bonds.

The central bank data shows private sector credit increased only 4.25 per cent between the months of July and December last year. A year earlier, it had increased 5.65 per cent.

Zahid Hussain

..................................................

The surge in public borrowing from banks has significantly elevated the risk of further reducing the availability of credit to the private sector through two channels.

One channel is through reducing the availability of liquidity for lending to the private sector.

Bank liquidity was already constrained by weak deposit growth and their inability to recirculate money through recovery from legacy loans.

Large scale borrowing by government through default risk free instruments is increasingly eating up large chunk of whatever liquidity was left.

Add to this the mandatory transfer of so-called surplus funds of the 60-plus public institutions to the central government exchequer, which will further strain bank liquidity until they are spent by the government.

The other channel is interest rates. Yields on Treasury bills and bonds have increased by 3 to 5 percentage points in the last year and a half. They now range between 7 to 9 per cent depending on the tenor of the instrument.

At a time when the government is imposing a 9 per cent ceiling on bank lending rates to the private sector except for credit cards, and when no effective measure is being taken to reduce the default risk of private lending, banks will naturally be much more inclined to lend to the government where they can get close to 9 per cent with zero default risk.

The increase in interest rates on public bank borrowing has also negated the potential fiscal benefits from the tightening of sales of the National Saving Certificates.

The parts of the private sector most vulnerable to crowding out are the high risk segments such as cottage, micro and small enterprises.

Given the 9 per cent ceiling and plenty of volume in the alternative risk-free lending to the government and relatively low-risk lending to large corporate borrowers with a good repayment record, banks will have to be extraordinarily unwise or philanthropic to be forthcoming in lending to these sectors.

The government needs to consider relaxation of lending rate ceiling for these credit-deprived sector to ensure that progress on the financial inclusion agenda is not set back.

Moving forward, the government will have to find ways to contain public borrowing or even repay the amount already borrowed.

This will require stronger revenue mobilisation, better utilisation of the foreign aid pipeline and expenditure rationalisation.

We have seen a tendency to add to subsidies one after another without any serious thought on their economic justification.

We also hear about wasteful expenditure by public officials on travel, vehicle purchase, and many other amenities.

Individually they appear small, but collectively they add pressure on the budget. There are many domestically funded projects in the annual development programme that can be put on hold without hurting the economy.

Prioritising expenditures must be the first priority in the efforts to contain public borrowing.

Revenue mobilisation can be strengthened first by not adding to tax expenditures through extension of new tax waivers and rebates and second through improving governance in tax administration by expanding in particular the use of automation processes.

Greater focus on accelerating the implementation of foreign-aided projects will help increase aid disbursements.

Particular attention is needed on addressing bottlenecks in public procurement and fund release processes.

The author is an economist

Comments