Relaxed policies fail to bring down bad loans

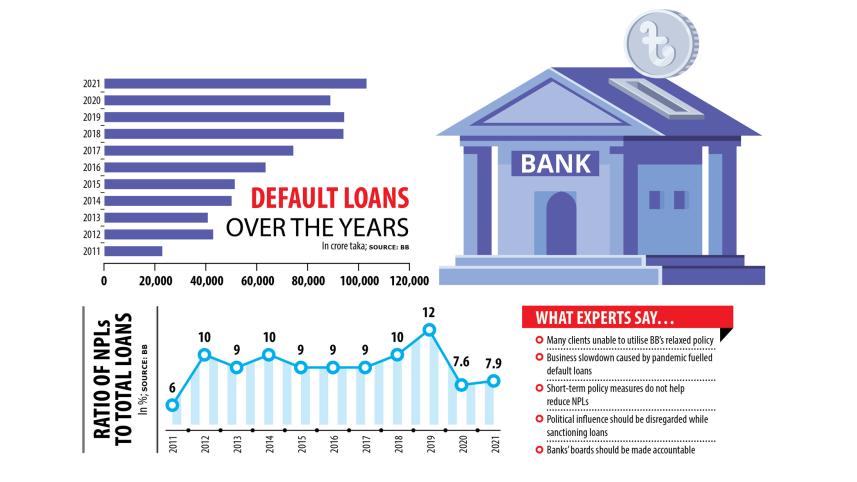

Default loans in the banking sector surged 16.38 per cent year-on-year to Tk 103,274 crore in 2021, rendering the relaxed loan classification policy unveiled by the Bangladesh Bank largely ineffective.

So, analysts have urged the central bank to take long-term policy measures in order to rein in non-performing loans (NPLs) instead of putting in place short-term steps.

The central bank earlier took various measures, including relaxing the loan rescheduling and classification policies, to get rid of NPLs. But the measures have proved to be ineffective and have not brought any good for the banking sector.

The ratio of NPLs to outstanding loans and advances stood at 7.9 per cent last year in contrast to 7.6 per cent in 2020, according to the BB data released yesterday.

A BB official says that borrowers enjoyed policy support in 2020 and 2021 as the government stepped up to help them withstand the impacts of the pandemic.

For instance, the central bank declared a moratorium facility for borrowers throughout 2020 that helped reduce NPLs to Tk 88,734 crore, down 6 per cent from 2019.

The relaxed policy continued last year as well.

Under the policy, borrowers were also allowed to avoid slipping into the default zone in exchange of giving only 15 per cent of the total instalments payable last year.

The central bank official says that some borrowers had early filed writ petitions with the High Court so that their loans were not shown as classified. But, the High Court later vacated the petitions following submission of pleas from lenders. As a result, classified loans rose.

Sadiq Ahmed, vice-chairman of the Policy Research Institute of Bangladesh, said that the business slowdown emanating from the pandemic was one of the factors for the rise in NPLs.

"We have to make concerted efforts to reduce bad loans. Short-term policy measures have not brought down NPLs. The authorities should take measures on a long-term basis," he said.

Politically linked influential persons frequently intervene in the loan sanction process of banks, causing the health of banks to worsen, said Ahmed.

"Such interventions should be stopped in order to ensure corporate governance in the banking sector."

Syed Mahbubur Rahman, managing director of Mutual Trust Bank, said that default loans might increase further in the second quarter of 2022 as the impact of the withdrawal of the relaxed loan classification policy would take hold.

He said that many clients had not used the relaxed policy, so banks were compelled to classify a good portion of loans.

"In addition, some habitual defaulters had not repaid instalments despite repeated attempts from banks. We have to speed up our loan recovery programme in the coming days to decrease NPLs."

Some borrowers who rescheduled their default loans before the pandemic were unable to repay the fund, according to Emranul Huq, managing director of Dhaka Bank.

The private commercial bank recovered a good amount of default loans last year.

BB data showed that 47 per cent of the defaulted loans were with the nine state-run banks.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. NPLs in the state-run banks rose 6 per cent year-on-year to Tk 48,968 crore last year.

Forty-one private commercial banks held defaulted loans of Tk 51,521 crore, up 28 per cent from a year ago. The NPLs in nine foreign banks increased to Tk 2,785 crore in contrast to Tk 2,038 crore.

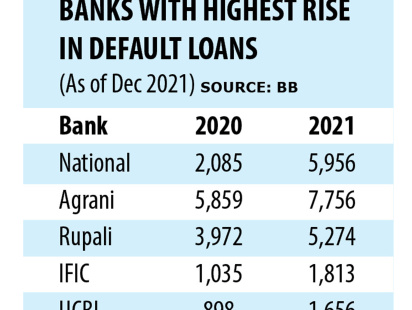

Five lenders that saw the sharpest spike in default loans are National Bank, Agrani, Rupali, IFIC, and UCB.

Mohammad Shams-Ul Islam, managing director of Agrani Bank, said that classified loans at the bank rose by 20 per cent last year.

BB data, however, showed that NPLs at the bank stood at Tk 7,756 crore last year in contrast to Tk 5,859 crore the year before, an increase of 32 per cent.

Islam explained that the actual default loans at Agrani Bank increased to Tk 6,472 crore in 2020 after the completion of the audit carried out by the BB.

The ratio of classified loans at the bank is still lower among the state-owned commercial banks, he said.

Comments