Differentiating the FY26 budget

The interim government (IG) is set to present its FY26 budget on June 2. The anticipation is that their budget will depart from the past. Following the unprecedented events of July 36, the IG, unburdened by political motivations, has no need to seek popular acclaim. This positions them uniquely to make a significant reform impact on budgetary planning and management, distinguishing themselves from previous administrations. While a substantial portion of the budget will necessarily reflect ongoing commitments from the past, there is hope that the IG will introduce innovative measures in areas where they have the flexibility to do so.

Smelling our coffee

Eschewing the pursuit of "populism" means the IG will dispassionately weigh the tradeoffs inherent in every budgetary decision, whether related to budget size, expenditure composition, revenue mobilisation, or deficit financing.

We must acknowledge that the IG consists of emotionally driven individuals, not heartless robots. They have their own biases and sensitivities towards societal expectations, which any government budget aims to address across the nation's diverse regions.

The IG members also possess egos that are naturally receptive to praise and recognition, often overshadowing objective calculations. The key difference is that IG leaders do not face elections, thereby positioning them to better meet the challenge without being fixated on public acclaim.

The IG is vulnerable to the lame duck syndrome because of their short tenure. This limits their ability to implement major policies as they are currently discovering. It is human to be drawn to rhetoric that generates popular appeal. The gap between feeling good about perceived economic recovery and actual progress is often larger than we think. The hope is that such aberrations will be significantly more constrained compared to previous governments.

In theory, lame ducks can head in good or bad directions. The public likes to believe the IG has the wisdom to know the difference and the passion for the public good.

Historically, administrations have obsessed over the size of the budget, dooming it to fail from the outset. The IG is expected to punt such impulses. An oversized budget offers only fleeting egoistic satisfaction. At this historic juncture, the IG can do a lot better by being selective in choosing battles that inevitably accompany budgetary financing and expenditure allocation decisions.

Financing footprint

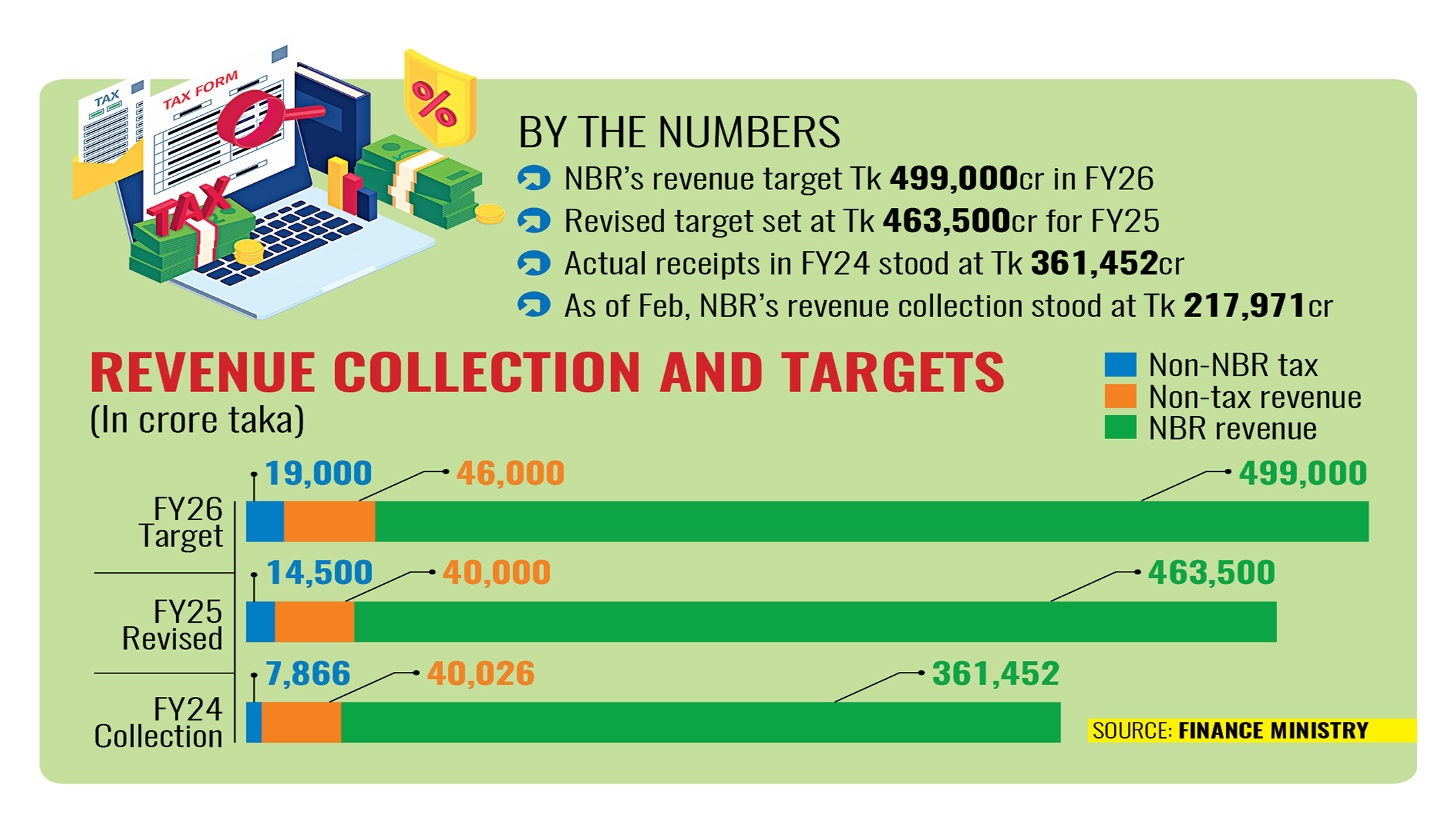

Efforts to enhance revenues are often resisted by pockets affected by the increases. Rhetorics pledging to generate more funds and causing pain to none lacks credibility. Honest taxpayers get an incentive to stay honest when the enhanced mobilisation effort focuses on tackling evasion, estimated recently at over Tk 2,20,000 crores in FY23, equivalent to at least four Dhaka metros, by the Centre for Policy Dialogue (CPD). Evaders will find ways to resist, as will those who lose benefit from tax exemptions. How much progress the IG can make within a single year in implementing measures to reduce evasion is uncertain, especially given the ongoing intra-bureaucratic conflicts on the legislation separating tax policy and administration.

We won't know unless they find a way to try. Evasion cannot be curtailed without limiting the discretion of tax officials and minimising face-to-face interactions between officials and taxpayers. To limit discretion, we must reduce the complexity of direct and indirect tax rates. Progress in the automation of tax administration is essential to minimise personal interactions.

Public borrowing is the other source of financing. Choosing a deficit size trades off inflation, interest and exchange rate risk depending on how it is financed. The macroeconomic risks of an oversized deficit are currently elevated.

External financing mitigates the crowding out and inflation risks, but adds to the existing stock of debt that future generations will have to repay. Prudence requires using credible metrics to assess the limits of external debt as we enter FY26 and leveraging all available options for policy and project finance from the creditors. Approaches fueled by overconfidence often backfire. The IG's assertions about readiness for specific reforms to tap external financing should align with their narratives about the state of the economy and their concerns about the outlook.

Domestic borrowing poses the greatest risk of crowding out private credit. The banking system's deposit growth is sluggish, and the government's domestic debt to revenue ratio is already high. To mitigate inflation risk, it is crucial to avoid deficit monetisation and allow private credit to expand as political and policy uncertainties clear in the medium term. Risk-free rates fall when the government reduces domestic borrowing which in turn poises fiscal policy to be growth-friendly.

Expenditure footprint

With the expenditure size bounded by revenues and prudent deficits, leaving a footprint means taking a hard look at the composition to identify where budgetary allocations need increases, where rearrangement is possible, keeping the envelope the same, and where decreases are warranted.

The most apparent sectors deserving increased budgetary allocations are health, education, and social protection. These collectively constitute no more than 20 percent of the budget when properly accounted for. Although they often struggle to utilize even the limited funds they receive, the solution is not to maintain stagnant allocations. Instead, it is essential to determine why they are unable to spend, aside from buildings, vehicles, and travel, where overspending is prevalent across various sectors.

Considering the World Bank's forecast that the number of impoverished individuals may have risen by 30 million in one year (2025), addressing poverty through budgetary channels in education, health, and social assistance is a social imperative that will synergise efforts in poverty reduction and human capital development.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Realignment and austerity based on value for money are likely to be more feasible in the Annual Development Program. Many lament the slow pace of expenditure releases for development projects this fiscal year. This deceleration partly stemmed from efforts to repurpose wasteful spending to useful spending. The IG has already shown a commitment to revisiting the fundamentals of ongoing projects, ensuring that sunk costs do not influence the decision to continue or discontinue them.

Austerity is possible in subsidies, which account for 11 percent of the original FY25 budget. Food, agriculture, energy, exports, and remittances are most subsidised. There isn't much room for manoeuvre in food and agriculture, except for the well-known abuse of subsidies given for farm mechanisation and the costs of delivering food rations to the target groups. The rest of the subsidy budget deserves a thorough reconsideration of the efficiency, equity and sustainability objectives they are supposed to have supported.

Leaving with collars high footprint

The present global landscape is marked by both obstacles and prospects. Nations involved in the initial round of tariff disputes are key partners in our international trade and finance. The populace anticipates that the budget speech will highlight advancements in tariff negotiations with the US administration. Relying on a timeline extension may be imprudent, given the likely deterioration in global activity and heightened risk perceptions.

For countries like Bangladesh, there are favourable developments such as the US dollar reaching a three-year low and a broad decline in commodity prices, driven by reductions in energy and agricultural prices. Should the uncertainties surrounding the Trump tariffs dissipate sooner rather than later, new avenues for exports and foreign direct investment may open up as buyers adjust their orders and supply chains are reshored.

The IG is anticipated not only to manage the tradeoffs arising from financial limitations and the shifting external conditions but also to ease tradeoffs within the domestic economy through structural reforms. The budget speech should outline specific economic benchmarks leading up to the conclusion of the IG's term.

An essential yet often overlooked tenet of economic policy is that unintended consequences frequently overshadow the intended ones. Our desire to exert control notwithstanding, genuine humility is crucial for staying attuned to the unfolding reality. Words hold weight, regardless of the context in which they are written or spoken.

Comments