In search of strategies for export diversification

The export structure of Bangladesh looks like a 'tadpole'- an early phase of a frog's life cycle where a big upper part of the body is linked with a shallow middle part and a long tail in the lower part. A limited number of 'dynamic' export products at the upper part dominate Bangladesh's export basket. This is followed by a list of 'new' products at the middle which have consistently maintained high growth, and further below a long list of 'surviving' products which have struggled to survive due to fluctuations in export growth. Unfortunately, there has been no sign of change in this 'tadpole' shape of the export structure over the years into a 'young frog' with a more balanced distribution of new and surviving export products. This high concentration in exports put policy makers under pressure towards achieving export diversification in order to ensure a broader basis fot the export-led growth of the country.

Exporters' ability to export different kinds of products consistently over a long period has been considered as an indicator for success in terms of export diversification. According to Rauch and Watson (2003), trade relationship between exporters (suppliers) and buyers (retailers) evolved in three stages- search, investment (deepening) and rematch (abandon current relationship). Structurally, dynamic products pass these stages and become the country's main source of export earnings. A limited number of new products are able to pass the challenges in the initial stage and enter the stage of deepening in trade relation. But a large number of surviving products are unable to pass the initial stage and struggle to ensure their survival in the international market. According to UNCTAD (2013), 41 percent of LDC products could not survive over a year. The survival rate for Bangladesh is the highest among the LDCs - only 29 percent of Bangladeshi products could not survive a year while the average period for survival is 2.4 years.

The export structure of Bangladesh

Bangladesh exports about 2,000 different types of products out of 6,049 (at HS 6 digit level) and exportable products have increased over time - from 1,565 in 2005 to 1,965 in 2013. It is important to note that the rise in number of products is entirely led by non-apparel products - from 1,364 to 1,770 in the same comparable period. Despite such encouraging growth in the level of products, the export structure is yet to be termed 'diversified'. Analysis of export products reveals that the top five products account for about half of the total export; about160 products each have an export value above USD 10 million, while another 230 products have a total export value between USD 1 million to 10 million each. In other words, less than 20 percent of total export products possess a considerable amount of export value (i.e. over USD 1 million) while the rest 80 percent possess an export value less than USD 1 million. Even more striking is the fact that over 50 percent of these products have been exported at a value less than USD 50,000 (BDT 4 million). Overall, Bangladesh's export basket is full of new and surviving products.

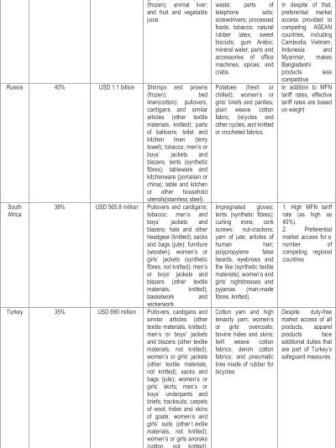

Although an overwhelming share of Bangladesh's export (in terms of value) is targeted towards the markets of the northern region (85 percent of total export value), a higher share of the total number of products is exported to the southern region (52 percent of the total number of products). Dynamic export products are mostly targeted to the northern region (54 percent) while new products are mostly targeted towards the southern region (64 percent). Products with an export value above USD 10 million are largely targeted towards the traditional markets of the northern region (e.g. EU, USA and Canada). On the other hand, products with a lower export value (USD 1 million or less) are largely targeted towards the markets of the southern region (e.g. Brazil, China, India, Malaysia, Russia, South Africa and Turkey).

Challenges for developing export competitiveness of 'new' and 'surviving' products

Major challenges facing the competitiveness of new and diversified products include the lack of comparative advantage in efficient use of available resources, poor capacity to ensure product and market diversification, high trade costs, low level of initial export value, poor physical connectivity and size of the economy of the importing country. In most cases, LDC products fail to attain comparative advantages and find other conditions burdensome; hence, it's likely that their products will survive for a short period of time. Present papers have applied the Revealed Factor Intensity (RFI) method to measure the comparative advantage of major manufacturing industries of Bangladesh.

Industries which are efficient in labour use (considered as an abundant factor) against capital and energy (considered as scarce factors) are found to have a higher share in export; dynamic products are likely to be the output of these industries. In contrast, industries less efficient in resource use have limited share in export; new and surviving products are likely to be the output of these industries. Along with factor use efficiency, a number of other conditions, as mentioned earlier, influence the structure of export of Bangladesh.

Strategies for export diversification

Strategies for export diversification should put more focus on new and surviving products along with dynamic products. Since developing competitiveness starts at the domestic level, measures for improving efficiency in resource use, building capacity to supply large volumes of export orders, higher spending on research, and developing the quality of products should receive greater priority in the strategy for diversification.

Identification of potential industries

Bangladesh's manufacturing industries, which are efficient in using abundant resources, are found to possess a higher share of export out of their total production. These industries include spinning and weaving textiles, wearing apparel, knitted apparel, footwear, non-metallic products, computers and equipment, communication equipment, consumer electronics, electrical equipment, jewellery and medical instruments. Besides these, there are industries which are less efficient in using resources but still possess a high share of export out of total production, such as processing of meat, fish and animal feed, beverages, paper products, batteries, ships, games and toys. Because of their capital-intensive nature, some of these industries are less efficient in resource use. On the other hand, a number of industries, despite having efficiency in resource use, are unable to raise their share of export, such as processed fruits and vegetables, tobacco products, manufacture of trailers, metal furniture and fabricated metal products. These industries possibly have yet to develop their critical minimum level of export capacity in terms of size, quality, initial export value and network.

Identification of diversified markets and diversified products

Identification of suitable products for potential markets is the first step to set strategies for export

Negotiation for reduction of tariff and non-tariff barriers

Discussion shows that Bangladeshi products face MFN tariff rate in a number of non-traditional markets which makes them less competitive against other countries. Bilateral and regional FTAs of these countries with one or more competing countries further reduce Bangladesh's trade competitiveness. On the other hand, Bangladesh cannot fully enjoy the duty-free market access provided by a number of countries due to stringent RoO. Hence bilateral negotiation with major potential non-traditional markets for lowering tariff on Bangladeshi products is urgently needed. In this case, WTO Provisions and Preferential Market Access for LDCs could be referred to for Bangladeshi products. High technical standards followed in a number of countries related to SPS and TBT are considered to be burdensome by the suppliers of new and surviving products. Bangladesh needs to discuss these issues at bilateral, regional and multilateral forums.

Building network between buyers and exporters Bangladeshi products, particularly new and surviving ones, need to be introduced in non-traditional markets. In connection to this, suppliers should take part in international trade fairs organised in those countries. Buyers of non-traditional markets should welcome international events organised by local trade bodies associated with industries of new and surviving export products. Such mutual exchange between buyers and suppliers would reduce the information gap and bring both sides closer for building a long-term trade relationship. In this context, local trade bodies should play a more proactive role. Existing network of buyers or retailers and suppliers of dynamic export products could be used to introduce new and surviving export products in traditional and non-traditional markets. Easy visa process is a necessary prerequisite towards ensuring flexible movement of buyers and suppliers.

.................................................................................................

Dr. Khondaker G Moazzem is an Additional Research Director at Centre for Policy Dialogue (CPD). Meherun Nesa is a Research Associate at CPD.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments