Future of G2P in Bangladesh: The case of social protection system

Dr Ahsan H Mansur, Executive Director, Policy Research Institute of Bangladesh (PRI)

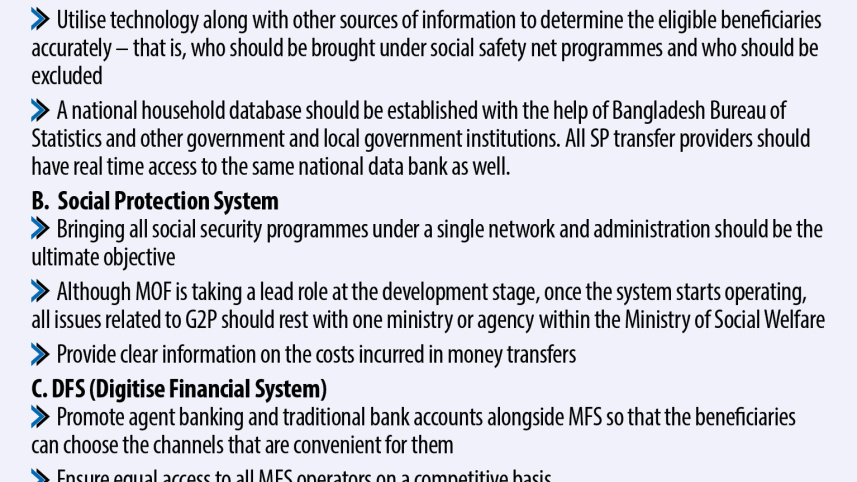

Many social protection programmes which are operating under different ministries need to be consolidated; otherwise, there will be multiplication of the same process. Thus, reaching the deserving beneficiaries will not be possible. We must ensure that we select the beneficiaries who deserve to be supported by the programmes the most.

Currently the Bangladesh government runs more than 150 social protection programmes under more than 20 ministries/divisions that creates inefficiency and mis-targeting. Global experience suggests that a single authority is generally most desirable in administering the social protection (SP) system because the database involves issues of quality control, maintenance, classification, across geographic regions and social groups, updating through addition of new beneficiaries and deletion of ineligible ones, after reviewing new applications for support and other information. A dedicated data bank (may be under a separate Division within the main ministry) with data specialists is required to maintain and upgrade the massive databases. NID operations should be moved to the central database and made accessible to all relevant government agencies or eligible institutions. Equal access for all service providers on a competitive basis is a doctrine that should always be protected to ensure quality and enhance efficiency.

Government agencies engaged in commercial operations must operate on equal terms with private sector operators. This principle of even playing field is sometimes violated, giving exceptional privileges to some companies and consequently putting other companies in the same market at a disadvantage. There should also be no discrimination based on the ownership of companies by foreign and domestic entities.

Md Azizul Alam, Additional Secretary, Finance Division, Ministry of Finance

Since 2019, all major cash transfer programmes have been brought under G2P programmes. 70 percent of the social protection budget are under the cash transfer programmes.

The government has declared a few cash transfer programmes under the purview of 20 stimulus packages, and the resource allocation for the overall stimulus, mostly through the banking channel, is almost four percent of GDP. A big portion of this budget is also allocated to enhance and expand social protection programmes. One such programme is designed to give 2,500 taka per month to 50 lakh unemployed people. 38 lakh of these beneficiaries have already been provided with the stimulus through Electronic Fund Transfer (EFT). Bangladesh Bank's Bangladesh Electronic Funds Transfer Network (BEFTN) infrastructure was used to execute this programme. The current daily EFT capacity of BEFTN is about ten lakh, which may be doubled if run on two shifts. Monthly, we may need about three to four million EFTs.

In the previous fiscal year, one crore EFTs were made to beneficiaries under G2P operations. 46 lakh beneficiaries have been brought under the G2P programme. There are two types of programmes for the three major social welfare programmes, which include the distribution of allowances to the elderly, widows, and the disabled. One is for existing beneficiaries, and the other is for those who are newly enrolled.

G2P is an MIS-integrated electronic payment system; every department has its own MIS. When their MIS is formed, the databases that are created are interchangeable and can inter-cross. Therefore, the data from the 2,500 COVID-19 allowances that were to be provided to five million families was cross-checked with the data from other databases for pension, national savings deposit, old-age allowance, and widow allowance. At the back end, the G2P system provides electronic facilities that allow for integration with different national databases and help rectify and update the selection process.

Debdulal Roy, Executive Director (Programming), Bangladesh Bank

After National Payment Switch Bangladesh (NPSB) and MFS become intertwined, users will have access to financing through NPSB, even without EFT. NPSB, with the current setup, can make 220 transactions per second. If the capacity of the EFT-based system is insufficient, Bangladesh Bank can adjust this with the NPSB-based system to process the transactions faster.

If all customers could access their finances whenever necessary and at convenient places, a cashless payment method could be introduced. A uniform QR code can be provided so that anyone can access it to make a transaction. However, this method needs proper promotion. Moreover, if the transaction process requires a fee, the fee needs to be reduced so that the method can be utilised by younger people (students) and people living below the poverty line or in rural areas. The government is trying to introduce an interoperable digital transaction platform under the initiative of the ICT Ministry, which can allow the social safety net funds to be readily accessible to the general population.

The national household database should be organised with the help of Bangladesh Bureau of Statistics (BBS) to provide access to uniform data to all relevant agencies. Linking NBR's taxation or bank account information with the data can also help find the right beneficiaries and the amount of fund needed for a beneficiary.

Dr Shahadat Khan, Founder and CEO, SureCash

The two most important things to consider are the beneficiary selection and the payment process. G2P payments are digital now and a payment platform is already available. All we need now is a reliable beneficiary database. But data collection, data management, and data processing are quite different from the payment of benefits. If we look at the architecture of G2P, the disbursements will be made by the relevant ministries and we understand data collection is a weak point for our country.

We usually think that financial service operators will do the work of data collection but G2P architecture says otherwise. There is a lot of work to be done in terms of data collection, data filtering, and data management by the government and local government officials who will be selecting the beneficiaries. There is also scope for collaboration here. After this comes beneficiary selection and then after collecting enough information, the MFIs open the beneficiaries' e-KYC accounts. The disbursement process that follows is a bit easier compared to the beneficiary selection and updating processes.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Through collective efforts along with ministries and other stakeholders, the responsible agency can check if there is duplication of beneficiaries or double dipping of benefits by recipients.

Kamal Quadir, CEO, bKash

A lot of work is being done for G2P payment. The current crisis would have been exceedingly difficult to tackle without the support of e-KYC. Even a few months back, MFIs could not open accounts digitally and the proactive policy support from the central bank in this matter is highly appreciated. MFIs need to focus more on the NID issue. Even after many years since the introduction of NIDs and the pandemic which struck Bangladesh, there are a lot of debates about whether enough people have NIDs. According to the Secretary of Finance, 110 million people have their NIDs, which is a large number. Therefore, we must make maximum usage of this infrastructure.

Sometimes the customers face inconveniences when the government agencies inform them about using certain services without considering their choices and convenience. Thus, we need to look into this issue.

Lastly, it is important to share the practitioners' experience whenever policy decisions are being made. Although our resources are increasing, most of the time we do not know where to find the proper resources. This is why we come up with solutions that make things more complicated.

Abedur Rahman Sikder, Deputy Managing Director (DMD), Dutch Bangla Bank Limited (DBBL)

We need to consider two parts of G2P. The first is the selection of the right beneficiaries which is quite challenging. The payment solution providers are usually not directly involved with this part. Our involvement comes during the payment process and when opening accounts where we must ensure the KYC procedure. After the selection of beneficiaries, the responsibility of making e-KYC falls on the payment solution providers. This payment can be through MFS, through the large agent banking network in our country, or through banks.

The costs must be considered as well. Through mobile banking, this cost can be a bit more sometimes and that is why for G2P, the authorities should look into other channels such as agent banking or bank accounts.

We hope that within the next financial year, all payments associated with various social security programmes will be made digitally. The stakeholders should equally promote agent banking accounts and bank accounts along with MFS since there are cost variations among these channels. This will provide the beneficiaries to choose from suitable options.

Md Shafayet Alam, Executive Director, Nagad

There are mainly three challenges to G2P. Firstly, the organisations providing allowances must want to adopt it. Next, they must have the ability to implement it. And, lastly, these organisations must be able to provide complete transparency throughout the whole process. As an MFS provider, Nagad works with the distribution channels. It is our job is to ensure that the remitted amount reaches the customer safely and they can use it conveniently. But the beneficiary selection process is not the job of MFIs. This is the responsibility of the allowance providing government organisations. The ultimate goal of the MFS providers is to get closer to a situation where the need for physical money will be eliminated.

MFS accounts can be integrated with ATMs and bank accounts very easily, within two to three months as the MFS operators are technically sound. However, challenges to this approach include: whether the concerned ministries are interested to implement it; the need for all stakeholders to work at the same pace, as this will help eliminate the risk of misunderstandings; and eliminating the perception that MFS operators take high service charge mostly for their own gains.

The efforts required and the stages and players involved in providing instant services to customers are huge. The MFS operators must pay retailers, distributors and other associates as well as pay fees to BTRC for these transactions.

Muhammad Solaiman Shukhon, Head-Market Development, Nagad

It is possible to conduct daily transactions by maintaining social distancing through MFS, especially if the service providers are dispersed. This will also help reduce the crowding that is still happening at banks. However, data authenticity is an issue because there can be cases where a person may not possess a mobile phone and/or NID and request the local representative to conduct transactions on his/her behalf. In such a scenario, manual intervention can play a part. No matter how much technology we bring in forward linkage, someone is selecting the ultimate beneficiaries and during that selection, we face the problems associated with the lack of honesty and authenticity. To resolve this, the local representatives can be brought under a disbursement channel. The agents who recruit these local representatives can be incentivised to provide authentic data and prevent malpractices. This may encourage local representatives or those involved in data collection at core levels to give authentic data, due to the commercial benefits involved.

Besides, technologies such as blockchain can be used to prevent trust manipulation since data is usually dispersed and therefore maintaining the authenticity will require such strong implementations.

Mohammad Ismail, Additional Secretary (Budget, Program and Assessment) and Additional Secretary (Institution and Disability), Social Welfare Ministry

There are some root level problems due to which our success rate is low in G2P expansion despite our efforts. Firstly, we are unable to motivate the union (local level) social workers who implement projects at the field level. Secondly, according to our estimates, around 10 to 15 percent of the people do not have mobile phones. The mentally disabled people who meet the age requirement, still rely on their guardians. We have created a categorical database of 19 lakh such people whom we give Suborno card, through which they obtain 450 taka per month.

The cards for widows, aged people, etc., that exist at the field level are misused. Cases arise where the actual beneficiaries do not get their money whereas the money is withdrawn by people whom the authorities are unable to trace.

There are very few banks which provide allowances every three months. Most banks tend to keep the money for a year and pay a lump sum amount in the thirteenth month. This approach often leads to people accompanying the owners to steal a portion of that money.

Moreover, it is extremely difficult for aged, mentally disabled, widowed people to reach banks as they are often situated far away.

Dr Fahmida Khatun, Executive Director, Centre for Policy Dialogue (CPD)

Those who need aid from social safety net programmes are excluded from the list whereas those who do not need this aid are in the list. We can do need assessment if we can prepare lists by utilising technology from the very beginning, to fix this exclusion and inclusion error.

We should ensure that besides stipends, loan assistance also reaches the small entrepreneurs, especially women, in both urban and rural areas, and farmers and other people in such occupations, through MFS. We can utilise e-KYC for providing these services as well. The effectiveness, efficiency, and transparency of all these services, including data preparation and selection, must be ensured from the beginning. BBS can help in this regard. Inclusive lists can be prepared by involving the local administration and the local NGOs. The overall efficiency will increase if we can bring everyone under MFS.

Khondoker Shakhawat Ali, Founder, Knowledge Alliance and Emeritus Fellow, Unnayan Shamannay

The main objective here is proper utilisation of public money while implementing the social safety net programme. There are both social and technical aspects of such objectives. We need to create a balance between these two to ensure transparency and accountability, otherwise government's initiatives will not reach the right people, no matter how much money we spend on these programmes. Our objective of alleviating poverty will eventually fail.

There are mainly three stakeholders here: designers and supervisors—they are the government bodies and the regulators; implementers—service providing organisations such as banks and MFIs; and the beneficiaries—whose interest should receive the highest priority.

Improvement of the social protection system is a governmental prerogative, whereas money transfer concerns are determined by the market dynamics of service quality. Governance and compliance issues are important in maintaining the balance of the two. We understand that platforms such as Rocket are a single bank-owned service, bKash is a subsidiary of a bank, SureCash is a technology provider for banks that offers the service, and Nagad is a service offered by Bangladesh Post Office. This gives us four different models in the MFS sector. However, all must work under the common MFS regulation under the purview of Bangladesh Bank to ensure compliance and governance; otherwise the interest of the beneficiaries will be grossly compromised.

Dr M. A. Razzaque, Research Director, Policy Research Institute of Bangladesh (PRI)

In the case of social security, despite having goodwill, we face the problem of selection error. We plan to support 50 lakh families during the COVID-19 crisis, but what is the basis of targeting specifically 50 lakh families? This programme of reaching 50 lakh families will only exist temporarily for one year and hence, will not be part of the social security structure. All the attention and manpower that will go behind this programme will give us no lasting benefits in the future.

Dr Bazlul Haque Khondker, Director, Policy Research Institute of Bangladesh (PRI)

The most important ministry working in the field of social security is the Ministry of Social Welfare. Many issues and challenges, particularly a problem with motivation, exist within this ministry because the personnel probably feel that G2P poses a threat to their jobs.

Even though a database of 19 lakh persons have already been created, a total of 92 lakh beneficiaries need to be covered, so a further 73 lakh persons should be added to the database for the expansion of the G2P. This will be difficult to accomplish in one to two years. Therefore, mitigating the challenges within the Ministry of Social Welfare is crucial. The government has stated that by 2025, all elderly eligible citizens will be given an old-age pension, which will effectively approach a universal pension system for all Bangladeshi citizens. This means that the ministry's work will increase drastically and managing the increased workload will be a significant challenge.

Clear information is required on the exact costs incurred in money transfers for the SP system which is now valued at 2.9 percent of GDP. Besides, letting customers choose which operator works best for them will create competition which, in turn, will give them more benefits.

Comments