Digital payment solutions during coronavirus pandemic

Muhammad Zahidul Islam,

Senior Business Correspondent, The Daily Star and Moderator of the session

Today's discussion will focus on how we can make the best use of our existing digital payment structure during the ongoing coronavirus pandemic. According to the latest data released by Bangladesh Bank in February 2020, more than Tk 41,000 crore worth of transactions took place in that one month. However, in March and April, the transaction has not been the same.

Tanvir A. Mishuk,

Managing Director, Nagad

If a recession takes place and we choose to save all the big corporations and disregard the daily wage earners, farmers, and small businesses, our country will not be able to recover. Even though our country is on lockdown and everything has come to a halt, our economy cannot stand still. If our economy comes to a halt, it will take a long time for our country to get back up on its feet.

Around seven crore people in this country are daily wage earners and bringing all of them under government stipends is not possible. A long-term solution is required for the current economic problem. We need to figure out a way to slowly keep the economy moving while maintaining social distancing. Everyone, including marginal workers, must be brought under financial inclusion.

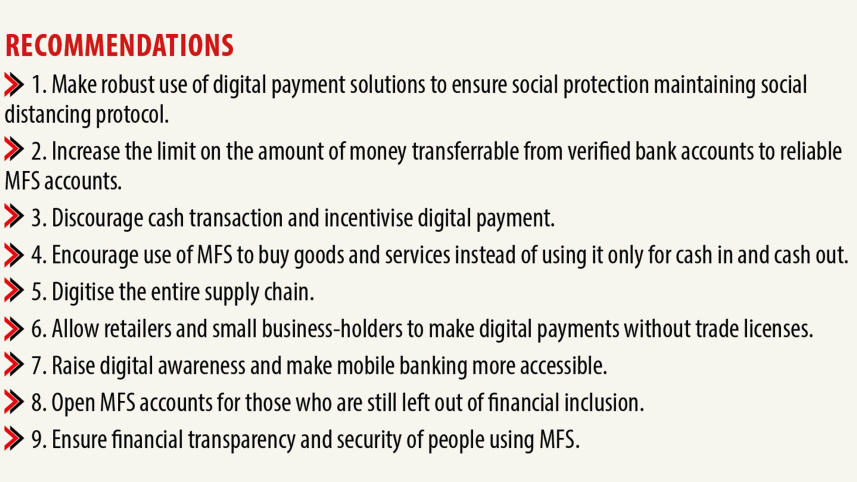

It's time we had one eye to the microscope and the other in the telescope, meaning we have to maintain the right balance in terms of our way forward, both including the short-term and long-term strategies. Hence, in the short-term there's no alternative to making robust efforts to bring as many people as possible under the digital payment solution ecosystem, to ensure social protection maintaining social distancing protocol.

Ashish Chakraborty,

Director and Chief Operating Officer (COO), SSL Wireless

We have been trying to find the solution to two problems that people will most certainly face in the present situation. Firstly, we have been trying to come up with easy ways to deliver groceries to people. Secondly, we have been working on the digitisation of the payment procedure.

After the announcement of the lockdown, there was quite a bit of confusion surrounding who was to be allowed on the streets. This created a big challenge in our delivery system. The government and law enforcers need to look into these matters to ensure deliveries take place. There is no point in ensuring digital payment if deliveries themselves cannot be properly made.

There are two prominent challenges in digital payment. Firstly, there is a general distrust among people here when it comes to online payment. They have concerns surrounding receiving the right products at the right time. Hence, they tend to prefer cash on delivery. This cannot be changed overnight. To try to overcome this problem, we have started link-based payment where a customer will get a text message containing a link after receiving their delivery. Upon clicking that link, they will be able to complete the payment using their mobile financial service account or bank account. We have also tried to start QR-based payment, but there are still some issues with this method. We have also helped some local delivery companies set up digital payment systems.

We are trying to reduce cash-based payment and make online payments as convenient as possible since cash carries a high risk of COVID-19 transmission. To promote online payment, we have started some discount campaigns and cashback offers. Even though the number of transactions is higher than usual now, companies in the payment industry should still provide more discount offers during this situation to motivate people to stay home and use digital transactions.

Sheikh Mohammad Monirul Islam,

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Chief External & Corporate Affairs Officer, bKash

The government has instructed the factory owners to take credit from banks and disburse wages among the workers through two mediums. The first being bank accounts and second, MFS accounts. We know that these workers will generally prefer to open and use MFS accounts. In the first ten days of May, we will see a lot of these workers getting their payments through their MFS accounts.

MFS is a digital wallet. If its use is not adequately known or understood, first-time users will naturally be a little hesitant. It is our responsibility to raise awareness about this digital wallet and educate everyone about this as much as possible. For a lot of mobile phone users, it might be their first time using their phone for transactions. Apart from this, first time users are also under the risk of facing fraudulence. So, we are starting campaigns to raise awareness about these issues.

Bangladesh Bank has declared us as essential service providers at the right time. But during total lockdowns, the MFS agent points cannot operate. During the period when everyone receives their salaries, there will definitely be a liquidity crunch since everyone will want to convert their digital payments. So, in that period, the law enforcers need to ensure these people are allowed on the streets. We also need to ensure enough liquidity so that a situation does not arise where we have digital money but our banks do not have enough liquidity for the conversions.

Rahel Ahmed,

Managing Director and CEO, Prime Bank Limited

I want to take this opportunity to salute all the MFS service providers. If this pandemic had hit us a decade ago, it would have been very difficult for the government to reach the marginal people and provide them allowances.

This situation has been a huge wake-up call for Bangladesh's banking industry as well as for the consumers. In the past decade or so, Bangladesh has undergone a digital revolution and, with respect to this, the banking industry has come forward quite a bit. For example, in the past, we would have around 400-500 people register for internet banking every month. Compared to that, the data from April shows that this number has gone up to a few thousands. Also, people had a lot of issues and barriers regarding e-commerce but now the consumers are forced to lean towards it. Besides MFS, banks are also helping a lot in this digitisation process through the issuing of debit or credit cards, for example.

It is inevitable for banks to upgrade their digital technology to increase operational efficiency in the future. COVID-19 has shown us that banks can be operated remotely which is something no one had thought of before. We also need to begin the use of e-documentations and through this, we will be able to provide more seamless service to our customers.

Zahid Hussain,

Former Lead Economist, The World Bank

Since we don't have any vaccines for COVID-19, we have no other choice but to keep the spread of the disease under control. We also don't know of any other way except for social distancing to prevent the spread of COVID-19. However, this social distancing is having a profound impact on our economy, and the degree of this impact is varying. Some of us are able to afford to stay locked down in our homes but most people aren't financially capable to remain locked down.

For a country like Bangladesh, fulfilling the conditions of social protection is very important. Without social protection, social distancing will not be effective. It won't be possible to keep those people at home who cannot fulfill their basic needs by staying home and, the number of such people is huge in our country. Economists usually have some fundamental questions regarding social protection such as how fast can it be delivered and how efficiently can we reach our target group. However, in case of COVID-19, another question has been added: how can we ensure social protection maintaining the steps that we are taking to contain the spread of the coronavirus? A health safety dimension is being added here. To ensure social protection, we have to undertake two steps. Firstly, we have to identify the beneficiaries and prepare a list and secondly, we have to ensure that the financial aid or food aid reaches them. MFS can play a big role here.

Most of the social protection programmes we have are food-centric. We also have well-targeted programmes such as Vulnerable Group Development Programme. Currently, we are facing the problem of delivering social assistance at a massive scale. The logistical challenge of these initiatives is huge. Moreover, the givers and receivers of such assistance are both vulnerable to health risks. We are also hearing about mismanagement in these initiatives. The alternative to this is providing cash but that too poses health risks. We need to figure out how we can provide people with purchasing power so that they can get their essentials as required. We can analyse the data our MFS has. The Ministry of Social Welfare, Ministry of Disaster Management and Relief, Ministry of Finance, Bangladesh Bank, are all linked to this. If all experts can identify variables together based on this data, we can identify beneficiaries so that after the pandemic, we can look at their transaction patterns and see who has been affected. The government has already announced some programmes which include food distribution through ration cards, adding money to old-age transfer schemes, allocating money in the informal sector through cash transfer. But no list has been made in this regard and which ministry will do it has also not been clarified. Therefore, we have a big scope of utilising our MFS system here.

If we are to rid ourselves of coronavirus, then every individual has to be free from it. We need to look into using digital technology for food delivery. We also need to look into how e-commerce can play a role in eliminating long queues of food distribution which are continuing to pose health risks.

AKM Shirin,

Managing Director and CEO, Dutch Bangla Bank Limited (DBBL)

There is no alternative to digital payment in this situation. Components of digital payment include salary disbursement which, if handed over physically to the workers, would create a disastrous situation. We are now being able to provide salaries through MFS. We have already opened around 30 lakh accounts and this number will continue to increase. Before this, around 16 lakh accounts used to exist through which salary disbursements took place.

If we look into the physical aspect of merchant payments, we can see that QR codes are being used which are enabling payments through MFS and cards. E-commerce is also enabling two types of payment. One is online payment – payments are being made directly through the MFS accounts and goods are reaching customers. Cash-on-delivery is the other type of payment that also requires the usage of QR codes in some cases. Utility payment is another sort of payment. Since it is difficult to go outside our homes now for making utility payments and since banks have limited operating hours, we can use MFS apps to make these payments.

The government is providing different types of allowances. Beneficiary identification is extremely important for proper provision of these allowances. We can make it mandatory for the beneficiaries to open MFS accounts to receive the allowances. MFS accounts are also very secure so there is less chance of fraudulence. At DBBL, we have experienced higher disbursement of cash with MFS – around Tk 10,000 crore – surpassing the disbursement that takes place via ATMs which is around Tk 7,000 crore.

We need to reduce our dependence on cash. For instance, when people receive their salary, it can be checked whether they have cashed out their salaries. We need to look into how we can make digital payments easier in this regard. The government can also help us. If incentives can be provided to customers by both the government and MFS providers, it can encourage digital payments. Also, discouraging customers, for example, by charging more for cash payments can be an option.

Kamal Quadir,

CEO, bKash

If economists highlight certain variables then operators like us can identify excluded groups such as the ultra-poor people in order to include them among the beneficiaries. In this way, errors will be minimal.

People who have NIDs can easily open accounts using their own phones or their relatives' phones or through digital KYC centres. Therefore, opening accounts is not a challenge in Bangladesh anymore. Moreover, even if the individual handset ownership is not 90 percent, family-wise handset ownership is very high which will reduce the need to go to agents to open accounts.

We can see that MFS usage has increased in the last one month among both city-dwellers and those residing in mofoshshols. It is a good thing that a group of those above the poverty line are also adapting to MFS. If we see the overall data of the past two months, total MFS transactions have reduced, however. This is mainly due to lesser bank hours. If liquidity cannot be ensured among the agents, then services cannot be provided.

Moreover, some banks claim to be open, but in reality, a lot of branches are found closed. This hampers transactions, since consumers withdraw money from banks to pay agents, and agents collect money and deposit it in banks.

Small merchants are under difficult legal regulatory requirements when taking payments. All of them must present trade licenses which can only be approved by the Ministry of Commerce. It is not possible for many merchants to acquire a trade license in the current situation and also the cost of obtaining the license is too high for them to bear.

Central bank should increase the limit on the amount of money transferrable from a qualified account, with complete transparency in identity, to a fully verified bKash, Rocket, or Nagad account. This would decrease dependency on agents during the COVID-19 situation.

Md Abul Kalam Azad,

Former Principal Secretary and Principal Coordinator of SDGs

The number of government-to-private payments was 2.5 million before the COVID-19 situation began. School payments must be added to that as well. Private-to-government payments were very low, at Tk 100 to Tk 150 crore monthly. A system of digital transfer of salaries for government workers has begun, which has ultimately helped develop MFS.

RMG workers already have access to many financial services, but in the context of new government decisions, in the past two to three weeks, around 2.5 million new accounts of RMG workers have been created. Electronic payment was only at five percent previously but has increased to 60 percent according to last week's data.

A mobile platform has been developed for daily necessities, which will hit the market very soon. A massive volunteer group has been formed, along with a large network which includes e-commerce. Volunteers are planning how the digital platform will be used to gain demand for daily necessities and then supply the services. This has created a big opportunity for MFS to develop.

A crowd-funding platform will also be launched soon. Many people are trying to help those who have been worst affected by the pandemic, but are unsure of where to donate the money, due to the fact that they cannot go outside. The crowd-funding platform will encourage digital financing while enforcing safe volunteerism. MFS account fraudulence also remains an issue since people find new ways to commit fraud no matter how many ways are blocked.

Big data analysis is required for rehabilitation work during post-corona times. Systems for providing trade licenses online have been developed by various municipalities and city corporations. The government can come forward to ensure this process can be done in an hour. At the same time, Bangladesh Bank should consider developing the cash-out system. The use of digital financing will allow further capacity-building in relief management.

Mohammad Aminul Haque,

Chief Financial Officer, Nagad

Bangladesh's crying need right now is increased financial inclusion. The number of people who have no MFS or bank account is still very high. However, after the recent RMG circular, there has been a tremendous flow of customers to Nagad, bKash, and Rocket.

The action plan would be to first use a circular and open MFS accounts for those who are still left out of the purview of financial inclusion. The first bottleneck at the moment is with regard to how to disburse incentives, especially cash incentives. This can be cleared now, even though it will be a mammoth job. Only 50 percent financial inclusion has been possible since independence, and so increasing inclusion is not easy, but is still feasible within a reasonable time-frame. Nagad has opened 120,000 accounts using its own marketing channels during regular times. With a government circular in place, Nagad can open 10 to 20 lakh accounts per day with its technological capacity.

In Bangladesh, the percentage of non-cash transactions using digital or electronic platforms is very low. Due to the percentage of cash transactions being higher, total money flow time is longer compared to other countries. The whole cycle of a retailer collecting cash after selling their product, ordering products again, and paying with cash to top up inventories require longer lead time. Bangladesh, therefore, cannot avail the benefits of the money multiplier, while developed countries can.

This problem cannot be solved if Nagad, bKash, and Rocket only focus on cash in and cash out. After G-to-P (government-to-person) disbursal is done, P-to-P (person-to-person) payments must be ensured by creating ways for people to carry out their top-ups and payments through MFS. Next, P-to-M (person-to-merchant) payments must be handled. Then comes M-to-M (merchant-to-merchant), which includes payments that one SME business-holder must make to another SME business-holder. Next is P-to-G (person-to-government) payment, since standing in queues at banks for these payments is not feasible now due to Corona crisis.

Mustafa Jabbar,

Posts and Telecommunications Minister

There is no alternative to digitisation. If preparations for Digital Bangladesh had not begun in 2008, life would be very difficult in the current COVID-19 situation. Bangalis are able to adapt to any situation, and this case is no different. An example would be how quickly we were able to include RMG workers in the scope of mobile financing.

The days of traditional banking are long gone. At some point in the near future, bank counters will become obsolete. These days, more transactions occur through ATMs than through bank counters. Agent banking has great scope for expansion, but I believe the rate of expansion is currently not as high as required. COVID-19 has taught us that the banking sector must find alternative ways to reach people. Since digital methods are available and easy to use, they should be utilised.

The financial system of Digital Bangladesh will, of course, be digital, and the preparations required must be taken. I hope COVID-19 will accelerate the digital journey of our financial sector, which will greatly benefit the people of our country.

Comments