Sri Lanka’s economic plight a caution for Bangladesh

That Bangladesh is in a position to bail out Sri Lanka, a middle-income country by the World Bank's classification since 1997, by extending up to $500 million -- is a nice lift to the country's morale.

But this episode is also a cautionary tale for Bangladesh: if the government does not get its act together now, the country could very well be in Sri Lanka's position in a few years.

The Achilles heel of the two economies is the same: low tax base, overreliance on a single item for exports and insubstantial foreign direct investment.

What Bangladesh has on its side is time.

It is still a least-developed country, meaning it has access to concessionary loans from multilateral and bilateral lenders like the World Bank, the International Monetary Fund, the Asian Development Bank and the Japan International Cooperation Agency.

The loans have a protracted tenure of 25-40 years as well as a reasonable grace period and interest rate of less than 2 percent.

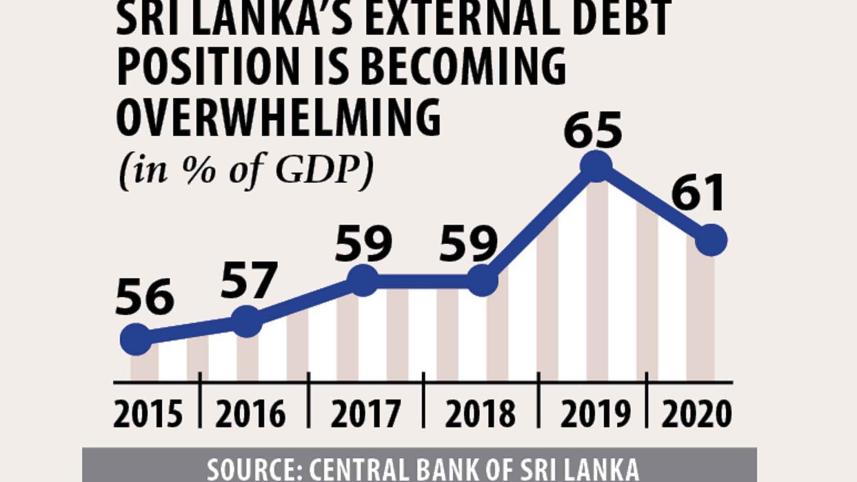

A casualty of a quarter-century-long civil war, Sri Lanka relied much on such foreign debt to build its infrastructure -- an economical practice, for the most part.

But at the turn of the century, following its graduation to a lower-middle-income country in 1997, Sri Lanka's access to such loans had dwindled, meaning it had to look elsewhere for funds.

In 2007, Sri Lanka issued its maiden international sovereign bond (ISB) -- worth $500 million -- and increasingly started to turn to this commercial borrowing channel.

The ISBs have a repayment period of 5-10 years, carry interest rates of upwards of 6 percent and no grace period.

To compound matters, there are principal payments: the total borrowed amount of an ISB is settled at the bond maturity date at once; the repayment is not spread across years, as is the case with concessionary loans.

So, when an ISB matures, there is a big hit to a country's foreign currency reserves.

At the end of 2020, up to 50 percent of Sri Lanka's outstanding external debt was tied to ISBs, according to its central bank data.

This would not have been a problem had the Sri Lankan government the means to pay back, had it addressed the structural weakness in its economy when it started leaning heavily on commercial borrowings.

In 2019, Sri Lanka's tax-GDP ratio stood at 12.2 percent, which is not too better off than Bangladesh's at around 10 percent.

Its foreign direct investment figure hovers in the millions, whereas Bangladesh's is in the early billions.

Its $88 billion-economy is heavily reliant on tourism and garment exports, leaving it at the mercy of external factors.

Bangladesh's solid foreign currency reserves are thanks to garment exports and remittance sent by unskilled workers, both heavily exposed to external shocks.

Sri Lanka has $3.7 billion of foreign debt maturing this year and about $4 billion of foreign currency reserves at the end of April, and hence the desperate scramble for dollars.

To make matters worse for Sri Lanka, global credit rating agencies unilaterally downgraded its sovereign rating, so the option to issue more ISBs to service the ones maturing this year is off the table.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Fitch downgraded Sri Lanka's sovereign credit rating to "CCC" last year, indicating the country's chances of default "a real possibility".

Rival rating agency Moody's downgraded Sri Lanka to an equivalent level too.

"The problems that Sri Lanka and Pakistan are facing right now did not show up overnight," said Ahsan H Mansur, executive director of the Policy Research Institute, a private think-tank.

So Bangladesh should watch closely how the crisis has unfolded in the two countries and take lessons from those.

In fiscal 2018-19, which is the latest available data from the Economic Relations Division, Bangladesh's foreign debt to GDP ratio stood at 14.7 percent, up from 13.2 percent in fiscal 2015-16.

While the ratio is well within the threshold go 40 percent, Bangladesh's foreign loan is on the uptick.

"When a car loses control uphill, it descends at an accelerating pace and can't do anything about it. We are not in that stage yet," said Mansur, a former economist of the International Monetary Fund.

Bangladesh is on course to becoming a middle-income country by 2024, so its window to concessionary funding will slam shut by 2027. This is another aspect the government needs to be mindful of.

As much as 84 percent of Bangladesh's exports come from the shipment of garment items largely to developed nations in the west.

"We will be in trouble if we can't diversify our exports at the earliest. Just because of remittance our reserves are high and we are comfortable on the external front."

But remittance's spectacular current trend is not sustainable, Mansur said.

"Once people start to travel freely again, this trend will come crashing down and our foreign currency reserves will contract."

Bangladesh's domestic position is very uncomfortable: the government's debt servicing relative to revenue is high, according to Mansur, also the chairman of Brac Bank.

"Our capacity to pay cannot be assessed by way of GDP as the private sector is factored in that. Debt has to be paid by revenue and our revenue base is low. Our tax to GDP ratio is one of the worst in the world."

Mansur went on to urge the government not to borrow for every project.

"Save for very productive enterprises, the decision to borrow should be considered stringently. Borrowing does not make sense for each and every project," he said, while citing the Rooppur nuclear power plant as an example of a project that does not warrant borrowing.

But for projects like Padma bridge and Karnaphuli tunnel, borrowing is valid as those would be able to pay back their costs over their lifetime.

Comments