Telcos not welcome in mobile financial services

The central bank continues to flip-flop over letting mobile operators have a slice of the mobile financial services pie, with its latest decision being that carriers cannot hold any shares in companies that provide MFS.

In the board meeting on July 15 that saw the MFS regulation get the green light, the Bangladesh Bank directors decided against letting the mobile operators in the MFS field.

But in the draft Bangladesh Mobile Financial Services Regulations, 2018 the central bank allowed mobile operators to hold a maximum of 49 percent shares in MFS providers.

Mobile operators have long been eyeing the fast-growing MFS industry, whose business runs through their network.

“A conflict of interest will emerge between the banks and mobile operators,” said a BB board member.

Many disputed issues may also emerge and a tussle will be created between the BB and the Bangladesh Telecommunication Regulatory Commission if the mobile operators were to get the approval to provide the service.

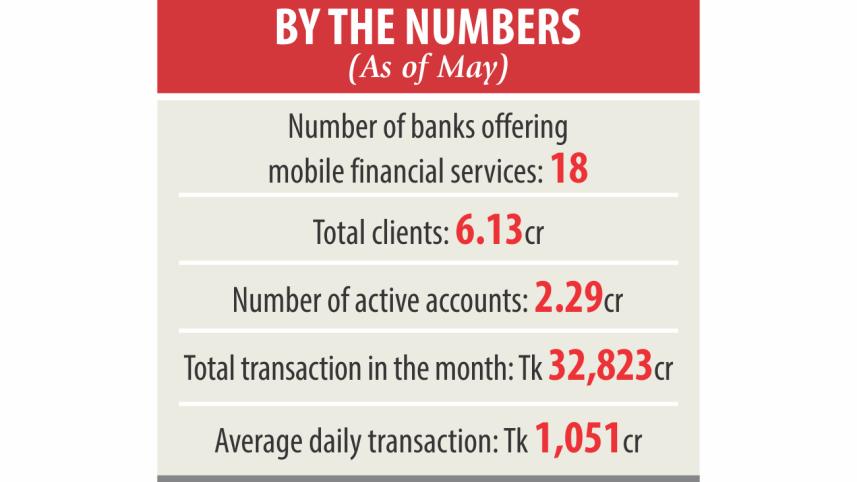

The branch-less banking is now becoming popular and mobile operators will hijack the industry if they were allowed to provide MFS, the BB official added.

Earlier in 2017, the central bank had prepared another draft regulation where it also stated that no mobile operator can hold any share in an MFS provider.

Prior to that, in 2015 the central bank had prepared another draft regulation where it said a single mobile operator would be allowed to hold 15 percent of the shares of a subsidiary company engaged in MFS operation and jointly they would be allowed to hold a maximum of 30 percent shares.

Along with banks and non-bank financial institutions, non-governmental organisations, multinational companies, investment firms and fintech companies with experience of working in banking and finance will be allowed to form an MFS provider company, according to the BB's latest regulation. The MFS providers in the country will be led only by scheduled banks.

The banks, which are already in MFS operation, are permitted to continue with their existing licences or they may form a subsidiary, the BB official said.

In case of new applications, the banks will have to form subsidiary companies to run the MFS operation and the company will play as payment service providers (PSPs).

One single bank, known as the parent bank, should have at least 51 percent of the equity of the PSP working as MFS. The remaining shares will be owned by NBFIs, NGOs and authorised entities.

The subsidiary model-based MFS provider will require a minimum paid-up equity capital of Tk 45 crore.

MFS providers will handle foreign inward remittances only if received through credits in nostro accounts of banks in Bangladesh. The amount will be deposited in MFS accounts of the beneficiaries in Bangladeshi taka.

No outward or cross-boundary transaction will be undertaken by MFS providers.

MFS providers are strictly prohibited from lending from their own funds.

But, they can act as agents of banks and NBFIs licensed by the BB and micro-financial institutions licensed by the Microcredit Regulatory Authority in disbursing loans and in accepting repayments on behalf of the principle concerned.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments