Cash crisis fuels cost of funds for NBFIs

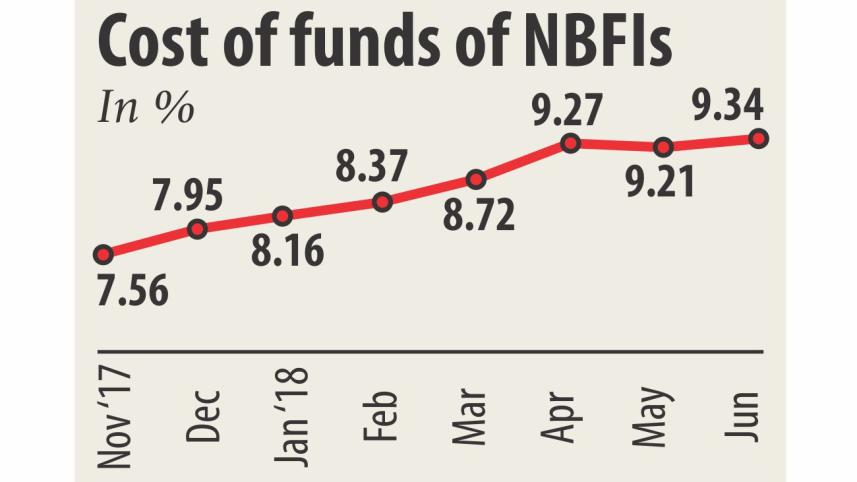

The weighted average cost of funds for non-bank financial institutions rose by 1.61 percentage points year-on-year to 9.34 percent in June this year thanks to the liquidity crisis in the banking sector.

The rising cost of fund is fuelling the interest rates, which is ultimately putting pressure on the borrowers, industry players said. The cost of funds is the interest rate paid by the banks and non-banks for the funds they collect as deposits from individuals and institutions.

The cost of fund serves as the reference rate for pricing the variable interest rate of the loan products. Lower cost of funds helps the NBFIs to set a reasonable interest rate for their loan products.

Uttam Kumar Saha, chief financial officer of Uttara Finance and Investment, attributed the rising cost of funds to the last fiscal year's liquidity crisis in the banking sector.

“Once the NBFIs were heavily dependent on the banks to collect fund, but they (banks) have recently become our competitors because of an acute liquidity crisis in the market.”

Uttara Finance has mobilised 85 percent of its funds from the business groups and general clients and the rest from banks.

Last year, banks collected funds from depositors at interest rates ranging from 9 percent to 12 percent, Saha said. The NBFIs were also forced to impose same interest rates to mobilise deposit, he said.

Uttara Finance offers 7 percent interest rate for three months fixed deposit receipt (FDR), 7.5 percent for six months and 8 percent for one year.

The NBFI now charges a minimum of 12 percent to 13 percent from its SME and corporate borrowers.

As per the central bank rule, the NBFIs are allowed to add at least 3 percent spread with their cost of fund to set interest rates for loan products.

The cost of funds increased both for the NBFIs and banks due to the liquidity crisis, Arif Khan, managing director of IDLC Finance, told The Daily Star yesterday.

Interest rate on deposit sharply went up last fiscal year in the entire banking sector which ultimately pushed up the interest rate on lending, he said.

“The NBFIs have to fix the interest rate on deposit considering the rate imposed by the banks. Under the circumstances, the cost of funds of the NBFIs increased gradually over the last fiscal year,” he said.

IDLC now charges 10.5 percent to 13 percent from its retail and corporate borrowers.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments