Why is tax-GDP ratio so low in Bangladesh?

Tax compliance means registration of a taxpayer in the system, timely filing of tax returns, completion of accurate reporting and payment of taxes on time. It can be voluntary or enforced.

There are two dimensions of voluntary compliance: committed compliance and creative compliance.

Committed compliance is the willingness to discharge tax obligations by taxpayers without grumbling. On the other hand, creative compliance refers to any act by a taxpayer aimed at reducing taxes by reducing one's tax liability.

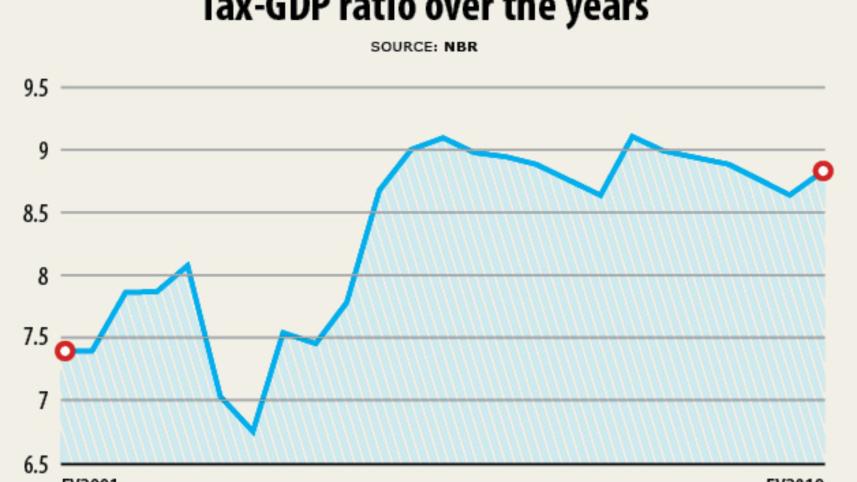

With tax-GDP ratio of 9.3 per cent, Bangladesh's tax-GDP ratio is much below the average of developing countries (15 per cent).

This is mainly because of poor tax compliance rate in both income tax and value-added tax (VAT), which contribute about 85 per cent of the revenue collection of the National Board of Revenue (NBR).

In Bangladesh, a large number of individuals and firms are unregistered and the vast majority of registered individuals and firms fail to pay right taxes.

Out of more than 10 million potential individual income taxpayers, 3.8 million are registered in the system, but about 1.5 million people file tax returns along with tax, according to NBR data.

Therefore, the personal income tax compliance rate is 14 per cent. On the other hand, out of about 213,505 companies registered with the Office of the Registrar of Joint Stock Companies and Firms, only 45,000 companies submit returns with taxes. So, the compliance rate of corporate income tax is 21 per cent.

Personal income tax contributes only about 40 per cent of the income tax revenue. The remaining 60 per cent of the revenue comes from corporate income tax.

The compliance rate of VAT registered firms is 11.56 per cent. The figure does not include those firms which are neither registered nor do they submit monthly VAT returns to the NBR (non-filers).

Bangladesh faces the problems of both creative compliance (tax avoidance) and enforced compliance (tax evasion). Apart from this, tax exemption and tax evasion are rampant.

Litigation management is a key issue of taxation. Moreover, the size of the informal economy constitutes 35 per cent of GDP.

The Eighth Five-Year Plan for fiscal year 2020-21 to fiscal year 2024-25 has set the target of raising the tax-GDP ratio to 14.2 per cent by 2025.

The plan underscores the need for consolidating efforts for revenue mobilisation, which can eventually be used for public investment.

More generally, the investments in health, education and social protection largely rely upon the size of the government revenue.

In order to attain the sustainable development goals (SDGs) by 2030, the NBR needs to prepare and implement a five-year tax modernisation plan. The plan may aim at reforming both tax policy and tax administration in order to improve tax compliance in the country.

The present Income Tax Ordinance, 1984 is outdated to keep pace with the changing need of time. So, a new income tax code is needed to put in place an efficient and modern income tax regime in the country.

The design of the new code will encourage wide voluntary compliance by the overwhelming majority of taxpayers. This will be achieved by a strong and efficient third-party reporting system.

Moreover, the new act must give emphasis on withholding tax.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. It is gratifying to note that by replacing the Value Added Tax Act, 1991, the government implemented the Value Added Tax and Supplementary Duty Act, 2012 from fiscal 2019-20.

The new act is definitely an improvement over the previous one in terms of coverage, registration, payment, audit, refund etc.

However, the multiple VAT rates have created distortion in taxation, which need to be reviewed. The new act will be fully operational when the VAT system goes digital.

The Customs Act, 1969 needs to be modernised with the launch of provision for full implementation of Revised Kyoto Convention, introduction of WCO SAFE Framework of Standards, introduction of authorised economic operators, and tariff rationalisation to promote investment and prevent mis-declaration and eliminate distortions.

The NBR has taken an innovative programme like holding income tax fair. Similar programmes may be undertaken in cases of other taxes. The NBR has put in place the mechanism of alternative dispute resolution (ADR) to reduce the tax pendency in the courts.

Now time has come to strengthen the mechanism by bringing all related stakeholders in compliance.

IGC research findings show that social incentives and peer effects are an effective way to improve tax compliance. The government may scale up the programme to a larger geographic area for enhancing tax revenue in Bangladesh.

The NBR should link electronic government (e-GP) with the tax system.

The NBR may be strengthened by redefining its status and regulatory powers and its relationship with the government, restructuring it and its field formations by function and type and by providing customer services to all taxpayers through a web-enabled tax administration (e-registration, e-filing of tax returns, e-payment and e-refund).

The tax administrator can also be strengthened by developing a strategic communication and taxpayer outreach and education programme and developing human resources and institutional capacity of the NBR.

The government may form a platform of think tanks for undertaking research and advocacy on taxation.

The writer is a former chairman of the National Board of Revenue

Comments