MFS industry swells riding on low-income groups

Mobile financial services have gained immense popularity in Bangladesh, particularly among lower-income groups, but the charge to withdraw funds has remained almost unchanged since the inception of the digital platform in 2011.

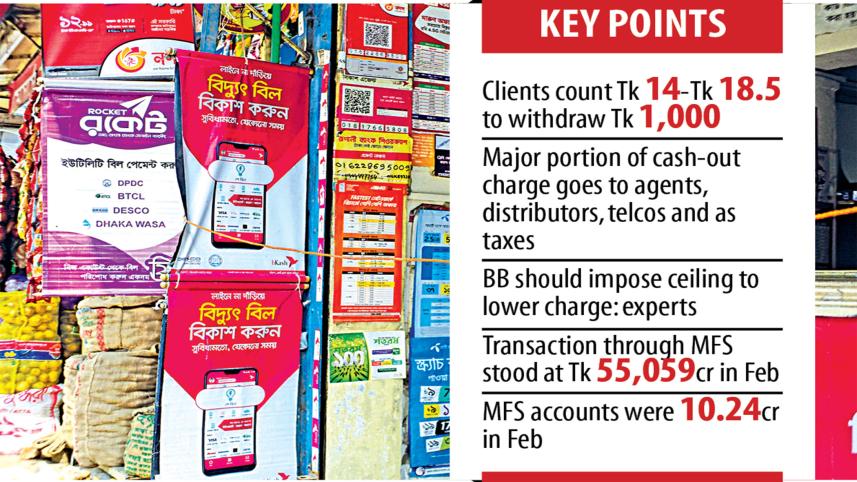

As a result, most clients have to fork out Tk 18.50 to withdraw Tk 1,000 from their accounts. It was the same when the service was rolled out.

Although some MFS providers have recently slashed the charge to Tk 14, users and analysts say the rate is still higher, and a further reduction will benefit the poor, who avail the money withdrawal service through mobile phones most.

Wahidur Rahman, a caretaker of a multi-storied building located in Mohammadpur in the capital, said that he got Tk 15,000 as salary per month and sent more than half of the amount to his family in his village home.

He has no bank account, so he sends the money through agents of mobile financial service providers.

"But the high cash-out charge is not convenient for me. A cut in the rate would benefit us," Rahman said.

Saiedul Hoq Nissan, a student of the University of Dhaka, has been depending on tuition for years in managing his academic expenditure. In addition, he sends a portion of his income to his parents to meet family expenses.

"I send money to my family through MFS, but the high cash-out charge has become a burden for me," Nissan said.

Experts say that the fund withdrawal charge of Tk 14 to Tk 18.50 is illogical as such type of high charge is rare while settling small financial transactions in the banking sector.

The central bank should intervene to this end as there is no ceiling on the cash withdrawal charge, they said. This will ultimately help the poor.

"The central bank should impose such ceiling on the financial transactions through MFS providers," said Fahmida Khatun, executive director of the Centre for Policy Dialogue.

The Daily Star talked with some MFS providers on the issue, and a majority of them opined that only the central bank could cut the charge by issuing an instruction.

Five stakeholders – agents, distributors, the government, mobile network operators (MNOs) and MFS providers –share the revenue generated from the cash-out charge.

Of the cash-out charge, 77 per cent goes to agents and distributors, 8 per cent to MNOs, 14 per cent to MFS providers, and 1 per cent to the government in the form of tax.

The revenue-sharing model is slightly different for the MFS providers that have imposed a lower charge than the maximum of Tk 18.50. Still, they have to share the same amount with the agents, distributors, MNOs, and the government.

On condition of anonymity, officials of the MFS providers said that they managed a tiny profit from the cash-out charge.

MFS providers usually rely on the clients' unused funds kept in their accounts. The operators keep the money with banks as fixed deposit schemes (FDRs), helping them manage a hefty interest.

There is no scope for a single MFS provider to share lower revenue with the agents and distributors than other providers, the officials said.

If any MFS provider tries to do so, distributors and agents will not provide the service of the provider.

Abul Kashem Md Shirin, managing director of Dutch-Bangla Bank Ltd (DBBL), which runs Rocket, said that almost 70-80 per cent of the charges realised from customers went to distributors and agents.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. "If we bring down the charge, distributors and agents will get a reduced amount per transaction," he said.

All MFS providers should cut the charge collectively, he said, adding that the regulator may fix the charge at below 1 per cent.

Then, clients will be able to withdraw Tk 1,000 at less than Tk 10.

"DBBL will be happy to comply with the regulator's instruction and help the poor customers receive financial services easily," Shirin said.

Fahmida Khatun said that the business volume of MFS providers had widened manifolds in recent time compared to five years ago. "This means the cost of doing business of the MFS providers has declined."

The total number of MFS accounts was 4.42 lakh, and transactions totalled Tk 207 crore in March 2012.

Today, there are 10.24 crore MFS account-holders out of a population of 16.6 crore. Of them, more than three crore accounts are active, and they collectively transact Tk 1,786 crore daily.

Total transaction through MFS providers stood at Tk 55,059 crore in February, up 33 per cent year-on-year, data from the central bank showed.

As the transaction volume has ballooned, any reduction in the commission in the distribution chain, particularly for withdrawal of cash, will not affect the income of distributors and agents, users and analysts say.

Selim Raihan, executive director of the South Asian Network on Economic Modeling, said that the high cash-out charge should be reduced to ensure inclusive growth.

The think-tank has recently carried out a survey on MFS where it found that financial transaction through the digital platform had enjoyed an uptick during the pandemic-induced lockdown.

But the upward trend did not sustain as the poor showed reluctance to embrace the service given the high cash-out charge, Prof Raihan said.

"The central bank should slash the fee to accelerate the use of the digital platform. This will bring a hefty profit for all the stakeholders involved in the MFS industry."

Sydul Haque Khandker, managing director of upay, an MFS run by United Commercial Bank, said the MFS provider found that 70 per cent of mobile money transactions took place via unstructured supplementary service data (USSD), and the users were mostly low-income people who do not have access to smartphones.

Upay charges Tk 14 for withdrawal of Tk 1,000.

Tanvir Ahmed Mishuk, co-founder and managing director of Nagad, said that the MFS operator had always favoured reducing the cash-out charge.

Nagad, a financial wing of Bangladesh Post Office, has taken initiatives to bring it down to the minimum level, he said.

Shamsuddin Haider Dalim, head of corporate communication and public relations of bKash, said the MFS provider was working to enhance the digital payment ecosystem to cut the need for cashing out funds.

Seeking to remain unnamed, a high official of an MFS provider said that there was a scope to lower the portion of the fee given to the MNOs.

MFS providers have to provide Tk 0.85 per session, which is 90 seconds, to settle every transaction.

The central bank should urge the Bangladesh Telecommunication Regulatory Commission to reduce the session charge. This will help decrease the cash-out charge, the official said.

Atiur Rahman, a former governor of the Bangladesh Bank, said that the BB should conduct a study to revisit the cash-out charge.

Rahman played a key role in introducing and popularising MFS when he led the central bank between May 2009 and March 2016.

The central bank should form a committee comprising the members of different regulators involved in the operation of MFS service, he said.

"The committee can come up with a decision after examining the issue," Rahman said.

Md Serajul Islam, spokesperson and an executive director of the Bangladesh Bank, said the central bank might revisit the cash-out charge.

"The central bank will look into the matter as the poor depend on the service," he said.

Comments