Agent banking was a rough diamond. Pandemic has buffed and shined its great potential.

The ongoing pandemic, no doubt, has been a sucker punch to both lives and livelihoods like no other in recent memory. But, amidst the catastrophe, there are a few bright spots.

And one such bright spot has been the lenders' agent banking window, which has been in operation since 2016.

If harnessed well, the digital banking channel -- thanks to its reach to the remotest parts, where banks have not set their foot in yet -- can make it an important cog in the wheels of the economic locomotive that would pull the country out of the ongoing crisis.

It could help lenders give out loans and mobilise deposits in tandem in the days ahead.

As of March, accounts in the agent banking platform, where 22 banks now give banking services to people, stood at 64.97 lakh accounts, which is more than double that from a year earlier, according to data from the central bank.

The lenders have mobilised deposits and given out loans exponentially in recent months by way of using the model.

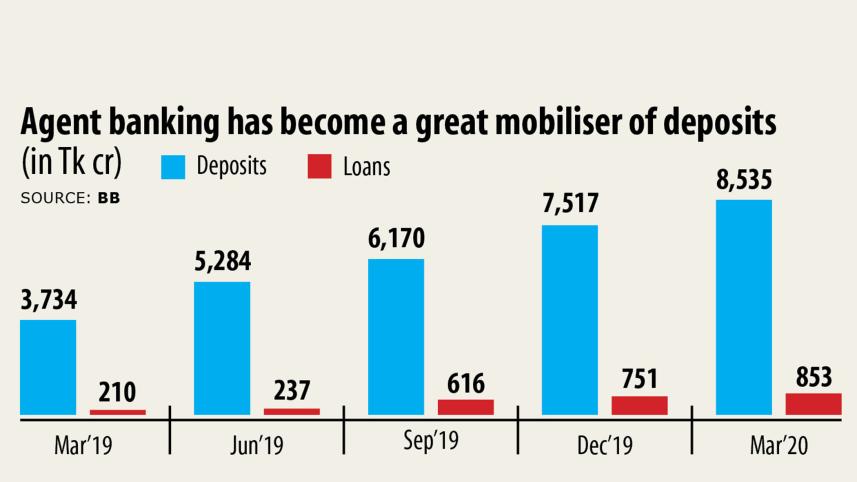

Deposits soared 129 per cent year-on-year to Tk 8,535 crore at the end of March, while loan disbursement grew 306 per cent to Tk 853 crore.

The central bank issued agent banking guidelines in 2013 as part of its effort to bring the unbanked population under the banking umbrella to widen the financial inclusion.

Before that, the Bangladesh Bank took a wide range of financial inclusion programmes to take banking services to farmers, marginal people and the extreme poor.

They were allowed to open accounts with an initial deposit as low as Tk 10.

As of March, the total number of accounts, which could be opened with deposits ranging from Tk 10 to Tk 100, under the programme stood at 2.13 crore and aggregate deposits Tk 2,385 crore.

This means the majority of the accounts, which are yet to be included digitally to the banking sector, are inoperable.

The picture has given a clear indication that the digital agent banking has bagged huge success when compared with the traditional financial inclusion initiatives.

The International Monetary Fund (IMF) has recently said that the countries with strong and vibrant financial inclusion could absorb the shocks from the ongoing recession.

The IMF research paper -- The Promise of Fintech: Financial Inclusion in the Post-COVID-19 Era -- has also given a message that the traditional inclusion will be unable to address the ongoing crisis.

There will be a requirement for digital financial inclusion to address the pandemic-stricken economy. Such financial system also helps people maintain social distancing to avoid the deadly pathogen, it said.

Md Arfan Ali, managing director of Bank Asia, echoed the same, saying digital financial inclusion could help revive the economy faster.

Agent banking, one of the major components of the digital financial inclusion arsenal, can reach many people with the government subsidies under the social safety net programmes and farm and small- and medium-sized enterprises loans.

Besides, rural people now get banking services at their doorsteps, which has encouraged them to park their liquid assets with the formal financial sector, Ali said.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Bank Asia, which has been a pioneer in popularising the model, is thinking about extending its lending operation through the banking window.

The bank, which has so far disbursed more than 50 per cent of its total outstanding loans amounting to Tk 853 crore, will extend its credit programme to a great extent in the near future.

By 2021, the lender hopes to disburse at least Tk 2,000 crore in loans through the window.

Agents are also encouraged to expand their business as banks provide them with a hefty amount of commission for their services.

For lending, agents enjoy a commission of 1 per cent of the sum; for bringing in deposits, they get 2 per cent the sum; and for remittance, they get Tk 50 for per payment.

Branch-led banking will lose its importance gradually due to the growing popularity for virtual banking, said Abul Kashem Md Shirin, managing director of Dutch-Bangla Bank (DBBL).

Lenders have to spend at least Tk 5 lakh to 7 lakh per month to operate a branch.

Besides, banks now spend less amount of funds to collect deposit through the agent banking window than their branches. This is applicable for lending as well.

Customers now allowed to open an account with an agent within 5-7 minutes by filling up the electronic KYC (know your client) form.

"This has attracted people widely."

DBBL, which is another leading bank in the agent banking arena, now provides the debit card to the accountholders of the window.

Customers can even carry out e-commerce by way of using the NexusPay app and also purchase products from different brand outlets through the QR (quick response) code.

Transactions at DBBL's agent banking platform has been on the rise since the inception of the pandemic, he said.

The daily aggregate transaction now stands at Tk 350 crore, which was Tk 250 crore before April.

Lending through agent banking is still much lower than that of the deposit collection by lenders, said Md. Anwarul Islam, general manager of the Financial Inclusion Department of the central bank.

"So, the central bank is morally pursuing the bank to speed up lending through the platform," he said, while acknowledging the platform's potential in helping with the economic recovery.

The IMF paper found that adoption of digital payments is significantly and positively associated with growth.

During the pandemic, technology has created new opportunities for digital financial services to accelerate and enhance financial inclusion, amid social distancing and containment measures, it said.

Smooth access to government electronic systems that are well-integrated with digital financial services platforms such as fintech firms and digital banking are proving to be critical in providing wide-reaching policy support promptly and without contact to the public, the paper added.

Comments