Shocks await banks next year. Should they begin preparations now?

Many businesses are now living on a knife edge, and it is widely expected that the pandemic will leave a lasting legacy of bankruptcies and redundancies.

Common sense would dictate that banks would be doing the groundwork such that when the catastrophe takes place, they would not be dragged six feet under along the way.

In fact, three of the biggest American banks have taken preparations for this eventuality, putting aside a combined $28 billion in provisions for current and future loan losses as part of their efforts to absorb the shocks emanating from the ongoing economic meltdown.

Similarly, the largest UK, Swiss and eurozone lenders are set to keep provisioning of a minimum €23 billion for the second quarter of 2020.

Oliver Wyman, a New York-based financial consulting firm, has projected as much as €800 billion of loan losses for European banks over the next three years in case of a second wave of coronavirus infections.

But in Bangladesh, only a handful of the banks are thinking along this line, with the majority yet to commence any preparation to this end.

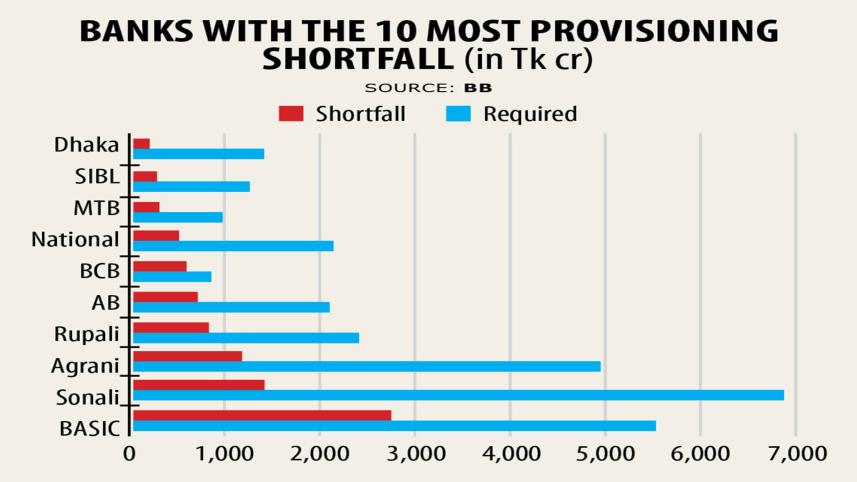

The country's banking sector has faced a provisioning shortfall in recent years due to a lack of corporate governance.

For instance, a total of Tk 3,619 crore was reported as provisioning shortfall against the required amount of Tk 60,493 crore in the first quarter of 2020, data from the central bank showed.

In the past, Bangladesh Bank permitted banks facing provisioning shortfall to preserve funds in phases such that they could manage a profit.

A loan loss provision is an income statement expense earmarked as an allowance for uncollected loans and loan payments.

This provision is used to cover loan losses such as default loans, customer bankruptcy and renegotiated loans. Banks have to set aside the fund from operating profits.

But in Bangladesh, banks are feeling comfortable as the central bank has given a regulatory forbearance, barring them from classifying loans until September in case of a failure to pay instalments by businesses given the ongoing financial recession. The deadline may be extended to December.

As per central bank regulations, banks have to keep provisioning between 0.25 per cent and 5 per cent for unclassified loans, 20 per cent for default loans of sub-standard category, 50 per cent for the doubtful category and 100 per cent for bad or loss category.

The comfort may not last.

The default loans may escalate alarmingly when the moratorium period expires as a large number of businesses are seeing their capacity to pay back loans is eroding gradually.

"If banks don't start preparing to keep provisioning immediately to tackle the future shocks, the entire financial sector will face deep trouble," said Ahsan H Mansur, executive director of the Policy Research Institute of Bangladesh.

Both the lenders in Western nations have received moratorium support to survive during the ongoing economic hardship, but they have also taken a mega programme to protect their financial health by increasing provisioning, he said.

The central bank should carry out a study immediately on the financial sector to take the stock of the actual condition of both businesses and banks, said Mansur, a former high official of the International Monetary Fund.

If required, the central bank may hire a third party to do this.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Based on the findings, BB may pursue banks to put aside the required amount of fund for provisioning. Besides, the central bank should restrict banks to give dividends to shareholders for 2020.

Banks should not be even allowed to pay stock dividends in the interest of the banking sector, said Mansur, also the chairman of Brac Bank.

"None has any clear idea of what will happen when the moratorium period comes to an end," said Syed Mahbubur Rahman, managing director of Mutual Trust Bank.

The majority of banks do not have adequate strength to keep provisioning to tackle the rainy days.

Lenders should set aside funds for provisioning from their operating profits in the next three years so that they could go from strength to strength sidestepping the recessionary hit, he said.

Default loans in the banking sector have been maintaining an upward trend for years, weakening the provisioning base of banks.

In March, the total amount of default loans stood at Tk 92,510 crore, accounting for 9 per cent of the total outstanding loans in the banking sector.

Default loans, however, decreased slightly between January and March due to the regulatory forbearance.

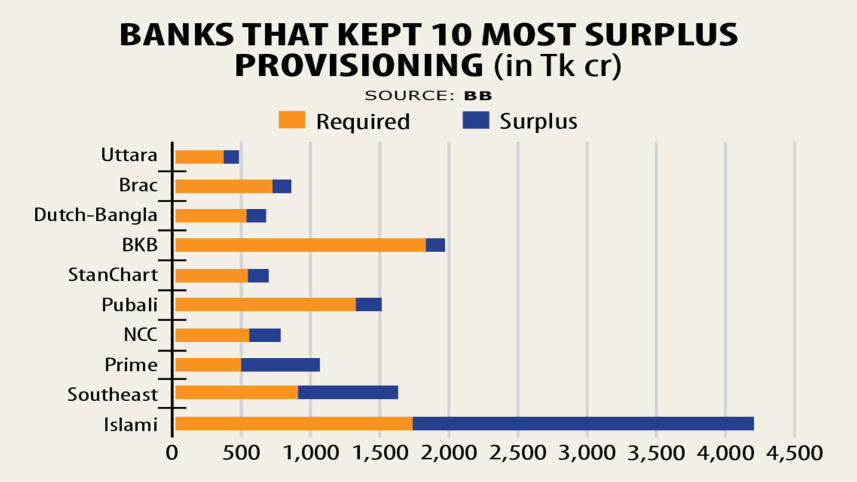

Some banks have taken preparation to strengthen their provisioning base.

City Bank kept aside Tk 41 crore in provisioning in the first half of 2020 to tackle the future uncertainty, said Mashrur Arefin, its managing director.

The bank will build up a satisfactory amount of provisioning in the next three years, he said.

MA Halim Chowdhury, managing director of Pubali Bank, said his bank has taken the same measure.

Comments