Interest rate cap can blow up in BB’s face

This is not the first time that the central bank has engineered to impose a cap on interest rates on lending. It did something similar back in April 2009, just after Atiur Rahman assumed the role of governor of the banking watchdog.

Then, the Bangladesh Bank set a maximum 13 percent per cent interest rate on all major loan products such as term and working capital for medium and large industries, trade financing, home and agriculture sector. It also fixed the exchange rate at Tk 69 for per dollar.

But the measures turned out to be glorious failures.

Between 2009 and 2010, a group of borrowers had taken a large amount of loans in the name industrial loans at the low interest rate and diverted the funds to the capital market and the real estate, said Ahsan H Mansur, executive director of the Policy Research Institute.

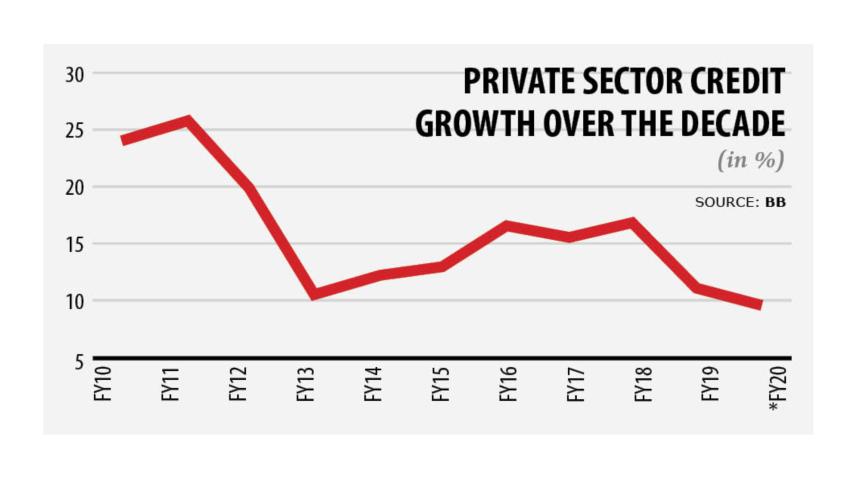

Private sector credit growth also saw a bubble during the period, which raced as high as 27 per cent in December 2010, up from 19.15 per cent a year earlier.

"Against the backdrop, banks faced a severe liquidity crunch. And the central bank was forced to take an expansionary monetary policy to inject money into the market in order to tackle the situation," Mansur said.

The price of land also increased manifold between 2019 and 2011.

But the expansionary monetary policy fuelled inflation, which went up to 8.14 per cent in November 2009, creating an extra pressure on people.

That is not all: a good number of people had failed to pay back the loans on the back of the stock market crash in 2011.

Many businesses that poured the fund in real estate also faced crisis in running their enterprises as a result.

"The aftermath of the interest rate fixation finally hit defaulted loans as well. Delinquent loans hopped on an upward trend as many became defaulters," said Mansur, also a former official of the International Monetary Fund.

Default loans in banks stood at Tk 42,725 crore in 2012, up 90 per cent from three years earlier.

The government realised the folly of its ways in 2011 and requested Mansur to give a presentation depicting the situation.

Mansur described the adverse impact of the interest rate capping at a meeting in presence of then Finance Minister AMA Muhith in the first week of March 2011.

Both the central bank and the government accepted the proposal and started to withdraw the cap from March 9, 2011. And all types of cap were lifted in January 2012.

"The central bank has done the same mistake. This will not bring any good for the banking sector," Mansur added.

The BB instructed banks on Sunday to set a maximum 9 per cent interest rate on all loan products except credit cards from April 1.

However, credit growth may not see an expansion this time as many banks will face liquidity crunch due to the 6 per cent interest cap on fixed deposit schemes, according to Salehuddin Ahmed, a former central bank governor.

Back in 2009, there was no ceiling for the interest rate on savings.

"So, there is a little scope for increasing private sector credit growth," he added.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The latest central bank decision will create the same problem that the financial sector faced during 2009-2011, said Zahid Hussain, former lead economist of the World Bank's Dhaka office.

Small and medium enterprises (SME) will face the most hurdles as banks will shy away from disbursing loans to them. In that case, both the country's employment generation and economic growth will be hampered.

The SME loan amount per borrower is way lower than corporate loans', so banks have to impose a relatively high interest rate to minimise their operational and monitoring costs.

Banks have to bear more cost for a SME client than a large borrower.

Lenders do not hesitate to hand over Tk 100 crore to corporate clients but such an amount can be disbursed more than 100 customers in the form of SME loans.

The country had followed a fixed interest rate model before the 90s. But from 1991, under the financial sector, the interest rate was left to the interaction of demand and supply of funds.

"We cannot go back to the old method as banking sector was completely dominated before 90s by the government. And there were a few private banks."

Besides, the country's private sector has significantly flourished in recent years, he said.

"A haphazard situation will be created if we now follow a fixed interest rate model," Hussain added.

Large loan disbursement by lenders will go up significantly as banks will have to follow the latest central bank's instruction.

From this year, banks also cannot cut back on their lending to the industrial sector to less than their three-year average for the segment, said the central bank notice.

Banks had faced a liquidity crunch when credit growth went up during 2010-11, said Nurul Amin, the then chairman of Association of Bankers, Bangladesh, a forum of managing directors of banks.

"Default loans escalated. Banks had to deal with the repercussions until 2015," said Amin, also a former managing director of both National Credit and Commerce Bank.

Comments