Interest on savings tools: Tax receipts treble in 3 years

The surge in sales of state-backed savings instruments has become a major source of income for the revenue collector in recent years as it charges up to 10 per cent tax on the profits made mainly by pensioners and middle-class families.

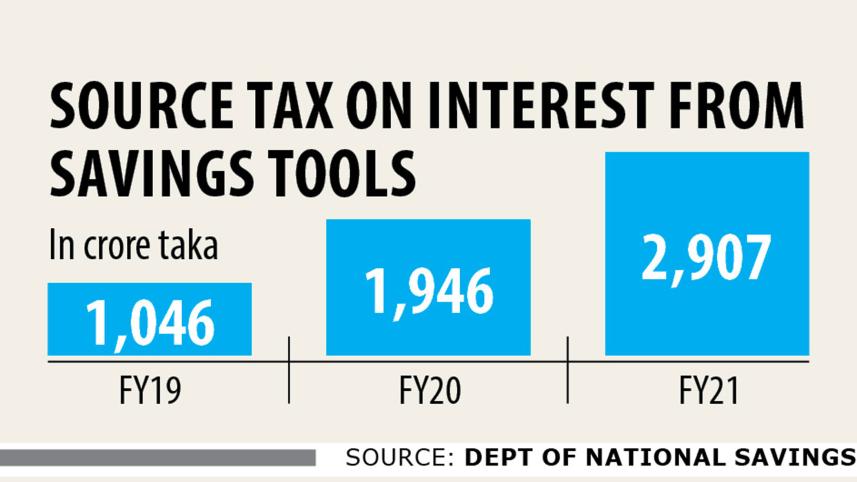

The Department of National Savings (DNS) said it deducted Tk 2,907 crore as the source tax on interest income of investors of pensioner savings certificates, family savings certificates and Bangladesh savings certificates.

The source tax deducted in the last fiscal year was 49 per cent higher from Tk 1,946 crore from the previous year. It was Tk 638 crore in the fiscal year 2016-17.

The increase came as many people parked their money in the savings tools in the last two years to earn higher interest against the backdrop of lower returns on the deposits offered by banks.

Savings instruments yield more than 11 per cent interest, whereas the weighted average interest rate on bank deposits was 4.05 per cent in August, according to the Bangladesh Bank and the DNS.

And lured by the higher interest rate, people bought savings certificates heavily in the last fiscal year, fetching a good amount of source tax for the National Board of Revenue (NBR).

Sales of savings certificates surged 67 per cent year-on-year to Tk 112,188 crore in 2020-21.

Currently, a 5 per cent tax is payable on the interest earnings for accumulated investments of up to Tk 5 lakh in savings certificates. No tax is payable for the same amount of investment in pensioners savings certificate, according to tax officials.

Investors of all types of savings certificates see a 10 per cent tax from their interest incomes for investment above Tk 5 lakh.

The tax deducted by banks, post offices and DNS offices on behalf of the NBR, is final, meaning that a person whose annual income stands below Tk 3 lakh will not get any refund—a provision that goes against direct tax principles, according to analysts.

As the tax deducted from the interest income from the savings certificates is not adjustable with other incomes, marginal taxpayers have to pay higher taxes.

Jasim Uddin Rasel, a tax analyst, said marginal taxpayers would have benefited if the NBR had kept the scope for adjusting the interest income from the savings certificates with other incomes.

Giving an example, he says if a taxpayer's annual income is Tk 4 lakh, including Tk 1 lakh from interest income from the investment in savings instruments, the person will have to pay a higher tax in the absence of the opportunity to adjust the interest earnings.

The individual would have paid only Tk 5,000 in tax had the NBR allowed the adjustment. In the absence of such a provision, the tax amount doubles to Tk 10,000.

The analyst called for fixing a ceiling for the smaller investors to give a relief to them from the tax burden.

Syed Iqbal Mostafa, a former president of the Dhaka Taxes Bar Association, says many families meet their regular expenses on the basis of the interest income from savings certificates.

"This is a big burden on the low-income families," he said.

Syed Md Aminul Karim, a former member of income tax policy at the NBR, says the provision of the final settlement is a burden for those who do not have taxable incomes.

"This is becoming a regressive tax. There should be scope for refunds for those who do not have any taxable incomes."

A regressive tax is a tax applied uniformly, taking a larger percentage of income from low-income earners than from high-income earners.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The tax authority should extend scopes to adjust incomes up to a certain threshold, said Karim, now an adjunct faculty of the banking and insurance department of the University of Dhaka.

Comments