Stabilisation need of the hour

Central banks globally are struggling to contain inflation even after raising their key interest rates. And although Bangladesh is experiencing a similar situation, the monetary instrument is largely ineffective in the country because of the 9-per cent lending cap.

Banks have been ordered to comply with the lending rate cap since April 2020 following the government instruction – a move that rendered the central bank's monetary policy statement (MPS) ineffective.

The issue has come to the fore again as the Bangladesh Bank is set to unveil its MPS for the next fiscal year, starting from July 1.

The urgency to reverse the course is ringing louder as higher inflation, which rose to an eight-year high in May, is pummeling households.

A number of officials say the BB is finding it difficult to come up with appropriate tools to address the soaring inflation.

Almost all countries are fighting higher consumer prices, largely caused by abnormally high commodity prices and supply bottlenecks owing to the Russia-Ukraine war. This forced central banks around the world to take a contractionary monetary policy with a view to tightening the money supply.

For instance, the Federal Reserves, the central bank of the United States, hiked the key interest rate by 75 basis points, the steepest climb since 1994, on June 15. The rate is expected to see a further rise.

On June 8, India's central bank raised rates for the second time in as many months.

Other central banks also following a similar path.

In a welcoming move, the BB hiked the policy rate 25 basis points to 5 per cent on May 29, but it frustratingly kept the lending rate unchanged. As a result, the rate hike has hardly brought any positive output to the economy.

The key interest rate, also known as the policy rate, is followed by commercial banks to set the interest rates on both loans and deposits. A spike in policy rates makes loans expensive.

Because of the existing lending rate ceiling in Bangladesh, the appetite for loans from businesses has not diminished despite the escalation in cost of production. A number of central bankers working on drawing up the MPS say that the political economy is dominating the monetary economy in Bangladesh, so the BB's task to contain inflation has become even more challenging than in other nations.

If there is no lending rate cap, the interest rate on all loans, including those for import financing, will increase automatically, said a central banker.

A hike in the lending rate would go on to reduce import payments, the biggest driver of higher consumer prices in Bangladesh. This will ultimately stop the depletion of foreign exchange reserves.

Under the current circumstances, the BB might make the lending rate cap flexible so as to reduce the money supply further.

The country's major macro-economic indicators such as inflation, imports, remittance, trade deficit and current account balance are all now in a stressed condition. The latest floods have added further woes.

"So, the new MPS will face an uphill task in order to bring back stability to the macroeconomy," said a senior central banker.

Ahsan H Mansur, executive director of the Policy Research Institute of Bangladesh, argues in favour of squeezing consumption at any cost in keeping up with the supply shortage of goods.

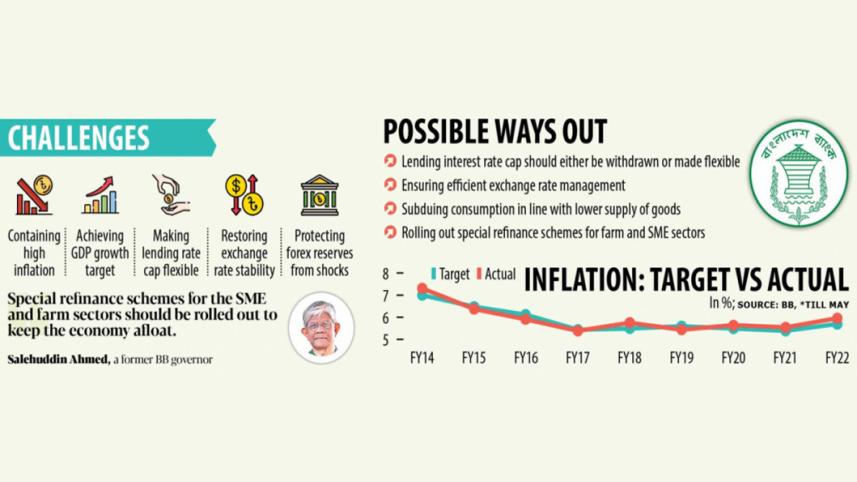

Inflation, which surged to an eight-year high of 7.42 per cent in May, will be tackled if import payments are restrained, he said.

"A disaster will hit the economy if the central bank tries to keep the cheap money available in the market," he warned.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The former official of the International Monetary Fund says nobody has thought six months ago that Bangladesh's foreign exchange regime would face the crisis it currently experiencing.

"The situation will worsen after six months if the central bank continues to follow the ongoing relaxed monetary programmes."

Credit growth to the private sector, which stood at 12.94 per cent in May against the full fiscal-year target of 14.8 per cent, will have to be contained, according to Mansur.

"Now is not the time for pursuing higher GDP growth. Rather, we all should pay attention to restoring macroeconomic stability."

Monzur Hossain, research director of the Bangladesh Institute of Development Studies, said higher import payments have already left an adverse impact on the foreign exchange reserves.

Between July and April, imports went up by 41 per cent to $68.66 billion, bringing the reserves down to $41.7 billion on June 28, whereas it was $46.15 billion on December 31.

"The central bank should take measures to restore stability in the foreign exchange market," Hossain said.

Salehuddin Ahmed, a former governor of the BB, urged the central bank to ensure the money supply to the productive sectors.

"Special refinance schemes for the small and medium enterprises and the agriculture sector should be rolled out to keep the economy afloat," he said.

"Such money supply will help generate jobs and give a breathing space to the public as they fight against a spike in inflation."

Mustafa K Mujeri, a former chief economist of the BB, said although there is some excess demand in the economy, the inflation is largely cost-push, led by food inflation.

"Under the current circumstances, demand management by using the policy rate and the bank interest rate will not be that effective to contain inflation. The main task should be to find a balance between demand management and maintaining the recovery effort and growth momentum."

He urged the central bank to ensure a smooth import of essential commodities and encourage finding alternative sources of imports to tackle the price hike.

Comments