Defaults creep up at NBFIs

Non-bank financial institutions saw their default loans rise 11.71 percent year-on-year in 2014, which observers say is a by-product of the sector's expansion.

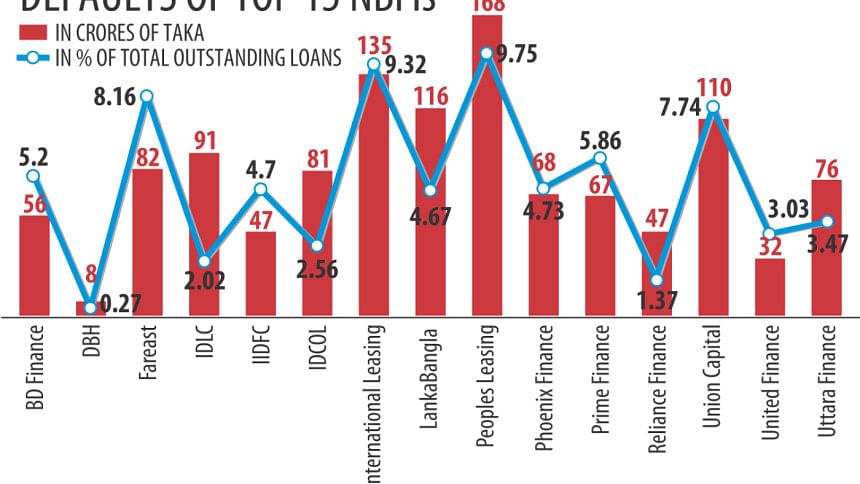

On December 31 last year, 31 NBFIs' default loans amounted to Tk 1,975 crore, according to central bank statistics. And some 15 firms account for 80 percent of the amount.

“As the amount of investment increases, so does the classified loans,” Asad Khan, chairman of Bangladesh Leasing and Finance Companies Association, said.

The NBFIs' total outstanding loans at the end of last year stood at Tk 37,276 crore in contrast to Tk 31,675 crore at the close of 2013.

Another reason for the increase, he said, was the absence of any helping hand from the central bank in 2013 for NBFIs to get by the prolonged political unrest, which unilaterally battered all forms of economic activities.

But that year, the banks were given the scope to reschedule loans under a relaxed policy.

“No such facility was extended to NBFIs and neither did we ask the central bank for it. Our clients continued to repay their loans, albeit in less amounts than they were supposed to.”

Yet, the NBFIs' total defaults are low when viewed against the figures of banks. At the end of last year, the banks' defaults stood at Tk 50,155 crore or 9.69 percent of their total outstanding loans against 5.3 percent for NBFIs.

Mahfuzur Rahman, executive director of Bangladesh Bank, said the rate of interest on NBFI loans is more than that of banks, but in spite of that their classified loans are less. The NBFIs have a much smaller number of clients, so they can manage their loan portfolio efficiently, he said.

Furthermore, the chief executives of NBFIs directly manage their loan portfolios, so the chances of them turning bad are low, according to Rahman.

However, the NBFIs expect the situation to take a turn for the worse in the near future, given the seemingly never-ending nature of the current political unrest.

So much that many good clients now cannot maintain their regular repayment schedule, said a chief executive of an NBFI preferring not to be named.

Yet, the central bank's inspection team “in their subjective observation” has been classifying many of the loans, he added.

Khan went on to urge the BB to give the NBFIs some relief from the subjective classification.

“Given the current scenario, it should not be logical to classify the loans in subjective consideration.”

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments