Bank reform for competition and economic growth

BANGLADESH has seen unprecedented growth of banks in private and public sectors to serve certain interested and purposeful politicians and bureaucratic persons.

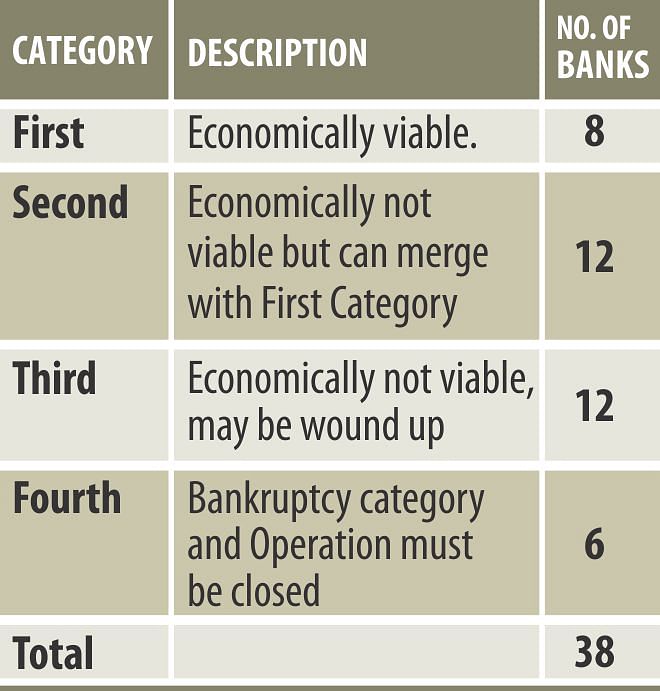

Based on capital surplus of 38 private banks reported in The Daily Star on November 24, 2013, these Banks can be categorized into following categories:

Bangladesh Bank may conduct a proper investigation into the profitability, liquidity, capital surplus and other tests about the survival of the above banks in the competitive world of free market economy. The same test may be applied to all government banks.

According to our above categorization eight banks in the First Category are commercially fit to run and operate banking business. Bangladesh bank may ask the 12 banks listed in Second Category to merge with First Category or go for voluntary liquidation after satisfactorily meeting the demand of the depositors and other creditors. Bangladesh Bank may also cancel the banking licenses of 12 banks in Third Category and ask them to go for voluntary liquidation after meeting all obligations and dues to all depositors and creditors.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. It is the moral obligation and also legal authority of Bangladesh Bank to cancel banking licenses of all six banks in Fourth Category. Such Banks have no justified legal rights to operate any banking business inside and outside Bangladesh. Bangladesh Bank must ask the Board of Directors of these banks to go for immediate voluntary liquidation after meeting their legal obligation to their depositors and creditors.

The Banks in First Category must extend their banking services to the rural Bangladesh at least up to Upazila level. They should go for extensive Mobile Banking Operation in rural area provided they have developed the secured and tested online and mobile net work.

At present four government banks namely Sonali, Janata, Agrani and Rupali Banks operate in the country but they do not have any computer network and knowhow. Although some Banks have computers in their Offices, they do most of the banking jobs on manual basis. They employ a large number of unnecessary employees.

Bangladesh Bank must make proper investigation and analyses into these four banks. If these banks meet the criteria of First Category of private banks, then two out of four government banks may operate independently. Otherwise, they must follow the Rule of Liquidation like private banks. Ansar-VDP Bank, Expatriate Bank like government banks should be merged with government banks. .

Further, is there any justification of Krisi Banks to operate in cities and towns? If there is any necessity of such banks, they must operate at Upazila and Union level only. In fact, their functions can be carried out by the First Category of Banks.

If the number of private and government banks is limited according to the above suggestions, Bangladesh Bank can easily monitor, direct and control all banks in the most effective manner.

Bank scams mainly happens due to the mismanagement and corrupt practices of Board of Directors of banks. Most of them are appointed politically. The Appointment or selection of directors must be delegated to Bangladesh Bank and according to Banking Laws. The Rule for appointing the Directors in all types of banks may be made in the following manner:

The total number of directors in any private or government bank must not exceed 15. Out of 15 directors, Bangladesh Bank must nominate 8 directors and 7 others will be selected from public shareholders. The CEO must be the Chairman of the Board of Directors. The CEO must be a professionally qualified person with sufficient banking experience. No important decision of the bank cannot be approved without 2/3 votes of the full Board. The Chairman will preside over the meeting and can give his view on the issue but he must not have any power to cast his vote in the meeting of the board. Duration of the board may be a period of four years and subject to the provisions of Banking Companies Act and also Companies Act.

The writer is a retired Chartered Accountant.

Email: [email protected].

Comments