Three decades of banking reforms

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Prior to the initiation of reforms in the 1980s, Bangladesh's financial system constituted typical examples of what economists dubbed 'financial repression'. The system, both the market and institutions, in the post-independence period faced major structural problems, evident both in banking and other components of the money market as well as the capital market.

To overcome these problems, the financial sector reform was initiated in 1982 with the denationalisation of commercial banks, followed by the establishment of the “National Commission on Money, Banking and Credit†in 1984. However, major reforms in the sector were launched in the early 1990s.

Banking is a dominant sub-sector of the country's financial system that underwent massive reforms. The reform programmes initiated under various auspices focused on several dimensions, most notably privatisation of state-owned commercial banks (SCBs), and entry of new private and foreign banks.

The other areas of focus were recovery of non-performing loans (NPL), interest rate deregulations, central bank's increased autonomy, enhancing prudential regulation and supervision, rationalisation and merger of bank branches and improvements to the money market.

Given the changing perspective towards denationalisation and private participation, the initial phase of banking reform (1980-1990) focused on the promotion of private ownership of commercial banks and denationalisation of nationalised commercial banks (NCBs).

While donors supported denationalisation from the very beginning, the compulsion to adopt reform measures was not strong until the mid-1980s. As the weakness of the sector exposed, the government transferred three nationalised commercial banks in the private sector during 1984-86 and four private commercial banks were granted licences in the early 1980s.

This round of reform, however, was largely unsuccessful due to the unprecedented influence of vested private commercial banks (PCBs) and NCBs' interest groups, which resulted in a loan default culture.

Given the poor outcome of earlier reforms, wide-ranging banking reform measures were undertaken under the aegis of the World Bank's Financial Sector Reform Project (FSRP) in the 1990s. The focus of reforms, among others, has been on gradual deregulations of the interest rate structure, providing market-oriented incentives for priority sector lending and improvement in the debt recovery environment.

Moreover, a large number of private commercial banks were awarded licences in the second phase of reforms. Although second generation banks have addressed many demand side issues, such as, development of a wide range of financial products and services, the measures have not been successful in addressing the banking sector's key problems. These include high NPL ratios both in state banks and private banks and a lack of enforcement of the capital adequacy and other regulatory requirements.

Since denationalisation, greater private participation and market based pricing of financial products did not generate the anticipated results even until the late 1990s, the focus had shifted to risk-based regulations and supervisions in early 2000s. This was largely due to the absence of firm supervision and effective regulations of Bangladesh Bank.

While the issue of regulation and supervision was spelled out in FSRP and the banks adopted Basel I norms (maintaining adequate capital to withstand crisis) in 1996, it was indeed the reforms in post 2000 that had a de facto focus on risk-based banking supervision.

Moreover, the Central Bank Strengthening Project initiated in 2003 focused on effective regulatory and supervisory system for the banking sector, particularly strengthening the legal framework, automation and human resource development and capacity building of the BB.

The Enterprise Growth and Bank Modernisation Project was adopted in 2004 by the WB to help the government achieve a competitive private banking system through a staged withdrawal through divestment and corporatisation of a substantial shareholding in the three public sector banks (Rupali, Agrani and Janata), and divestment of a minority shareholding in the largest state bank, Sonali.

Outcome:

The banking sector reform faced a strong resistance from organised labours, but political support favoured various reforms in the sector as the entry of private players provided them with considerable incentives. The share of nationalised banks' in total banking assets and deposits has declined over the years. Even in the early 2000s, the NCBs/SCBs constituted 47 percent of industry assets and half of the industry deposits. However, the private commercial banks (both local and foreign) emerged as a dominant player in the sector constituting 65 percent of industry assets.

However, the first two phases of reforms did not bring any measurable outcomes, highlighting the fact that wholesale liberalisation without instituting an effective regulatory structure is not the answer to the cumulative problems of bank nationalisation. Nevertheless, the sector turned around in the early 2000s when the focus was shifted to risk-based regulations and supervisions. Moreover, there has also been a strong public opinion against the defaulters, which along with political commitments facilitated enactment of a number of new laws, regulations and instruments to curb NPLs.

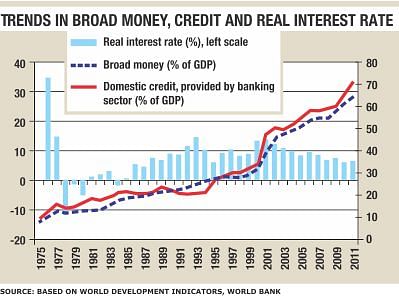

That said, financial development outcome of the banking sector is generally judged on its depth, access, efficiency and stability. Key banking sector indicators show that banks' performance, notably private banks, has increased sharply, particularly in the post-2000s.

Depth in banking assets is reflected in rising share of deposits, private sector credit and broad money in proportion to GDP. Access to banking services is on the rise, reflected in branch expansion and firms' access to credit, including BB's financial inclusion programmes. While high interest spread is a drawback, other indicators of efficiency in the sector, such as return on assets and return on equity, are favourable. Finally, asset quality, capital adequacy ratios, probability of default, among others, that indicate banking sector stability suggest that private sector banks in Bangladesh are fairly stable.

The most important development in 2000s has been the banks, notably private banks' commitments towards the implementation of Basel II, in which banks are required to maintain a Capital to Risk-Assets Ratio (CRAR) of 10 percent.

Governance challenges:

While the reforms' success, notably in the post-2000s, is largely due to better performance of private sector banks that account for nearly 65 percent of banking industry assets, nearly a third of the sector (SCBs and development finance institutions) is ailing. The SCBs' performance has not improved in line with reform objectives, largely owing to political interventions. Moreover, the autonomy of BB has been curtailed by instituting the Banking and Financial Institution Division in the finance ministry in 2009, which has been an obstacle in monitoring of SCBs by the central bank.

As the public banks are not within the de facto purview of the supervision of the BB, their weak compliance with prudential regulations is a serious risk to the stability of the banking system. The recent SCB scams indicate that the success of reform could be reversed if politicians and their aligned business groups find room to channel the outcome entirely in their favour.

The reform experience in the banking sector also offers a broad lesson for other segments of the financial system that without instituting an effective regulatory architecture, market based reforms could do more harm than good -- the lesson thousands of investors learnt, albeit painfully, during the two episodes of stockmarket crashes.

Going forward, the banking sector needs to address a number of challenges with regards to high interest spreads, money market volatility, balance sheet problems of SCBs, central bank's autonomy, political interference in allocation of credit and overall governance problems. Moreover, the sector still has much to catch up with regard to financial innovation. The immediate challenge nevertheless is to reestablish BB's greater control over SCBs, dismantling the Banking and Financial Institution Division.

Comments