Global oil supply and demand equation poses risks

LOOKING ahead few years, global demand for oil will continue to increase because of rising prosperity in emerging economies. Supply, however, will still remain constrained

Soon, the world will not be able to produce all the oil it needs as demand is continually rising while supply is falling. According to International Energy Agency (IEA), oil consumption will rise by 56% between now and 2040, with China and India responsible for half of this increase in consumption.

Global oil demand for 2013 will probably be around 91.3 million barrels per day (mb/d). Demand will grow to 92.6 mb/d in 2014, according to the IEA

About 90% of the increased demand comes from emerging-market economies. However, this may change as Fed "tapering" causes currency volatility and higher interest rates in many emerging-market economies. According to 2014 global demand forecast from the IEA, the biggest demand increases will come from China and Saudi Arabia. The IEA expects Japanese demand to fall.

2014 Global oil supply

Total non-OPEC supplies should grow 1.75 mb/d in 2014, mostly due to the shale oil boom in the US. To meet global oil demand, non-Opec supply will be about 64 mb/d, with a "call" on Opec crude to be about 30 mb/d. Saudi Arabia is head-and-shoulders the largest oil producer in Opec, at currently about 9.76 mb/d. Most Opec countries produced slightly less oil in 2013 versus 2012.

Forecasting the Opec producers is difficult, so energy forecasters use a "call" on Opec. This is the difference between what non-Opec producers will produce, plus an amount from Opec to meet forecasted demand.

It's also helpful to understand spare capacity and current production and their potential "Sustainable Production Capacity." Spare capacity from Opec is about 4.59 mb/d. Opec's low spare capacity is one of the reasons oil prices remain high. Before the 2000s, spare capacity was at least 10 mb/d. In the first decade of the 2000s, spare capacity got as low as 2 mb/d. Global spare capacity has improved the last few years, but remains a concern. The Russia/Ukraine crisis could further reduce worldwide spare capacity and make prices spike higher.

How long will global reserves last?

Some analysts project the world will need close to 100 million barrels per day by the end of the decade. That would be about 36.5 billion barrels a year (100 million b/d times 365 days.)

If global reserves are about 1.525 trillion barrels of proved conventional and unconventional oil, and the world uses about 36 billion per/year, then global oil should last about 42 years.

I don't believe the world has 1.52 billion barrels proved reserves.

Look at most of the non-Opec countries' reserves including Mexico and Canada. Most countries are showing declines, but many Opec countries reserves are stable or are growing despite decades of production.

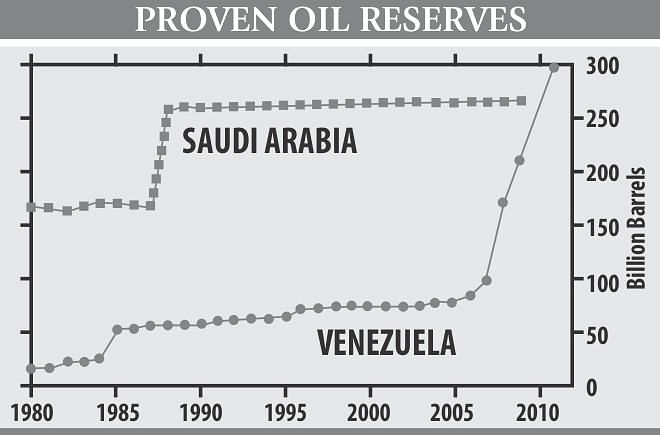

The chart illustrates the problem I see with Opec.

Notice that both countries reserves remained relatively the same since 1985, even though they depleted their reserves by a few hundred billion barrels. Most other Opec countries have similar reserve histories. Should we believe Opec when it tells how much oil its members have?

I think global reserves are closer to one trillion barrels based on research I've done, backing out production going back to 1985. Under my adjusted numbers, we have about 28 years of oil left (1 trillion barrels divided by 36 billion barrels). Bottom line: the world has between 41 to 28 years of oil left. I think it's closer to 30 years.

A study by Pickering, Holt &Co, an investment bank focusing on energy, estimates that more than 50 billion barrels of oil and gas had been consumed in 2013 against only 20 billion barrels of conventional oil discovered. The study has examined 400 exploration wells and has concluded that companies have found less oil than anticipated, despite heavy investments in capital and technology. Deep-sea exploration, where more hydrocarbons are being discovered at about 1,500 meters, is becoming ever more important.

None of the discoveries made in 2013 exceeded one billion barrels of oil equivalent. The largest one was made by the Italian ENI off the coast of Mozambique, with two deposits of 700 million barrels, followed by the Lontra (Angola) by the American Cobalt (900 million) and that of a field in Malaysia by Newfield Exploration (850 million). Others have been unsuccessful, such as in Ethiopia and Cote d'Ivoire by British Tullow Oil. Oil explorations by Shell and Total off the coast of French Guyana produced very little.

According to the French Institute of Petroleum (IFPEN), reserves discoveries between 2008 and 2012, including deposits in places to hard operate in, cover only 40% of global consumption of conventional oil. This is far from offsetting the decline of mature fields. According to the IEA, who studied the profile of 1,600 fields having passed their peak production, production has fallen to an average rate of 6% per annum.

Richard Miller, a former BP geologist, and Steve R. Sorrels, a co-director of the Sussex Energy Group at the University of Sussex (UK), have stated that squeezing more oil out of older reserves and exploring new ones in the deep seas will not be sufficient to meet the production levels required to address the demand. They have estimated that we would need to bring on-stream new productions equivalent to a minimum of 3 million barrels per day to compensate for declining crude oil production. This is equivalent to a New Saudi Arabia every 3 to 4 years in order to meet the demand. The oil peak is the result of declining production rates, not declining reserves.

Professor David J. Murphy of Northern Illinois University, an expert in the role of energy in economic growth, has stated that the Energy Return on Investment (EROI) for global oil and gas production is about 15 and declining. EROI is the amount of energy produced compared to the amount of energy invested to get and use it. EROI of oil and gas production is 11 for the US and is also declining. It is generally less than 10 for unconventional oil and biofuels. As the EROI decreases, energy prices increase. The dependence on shale could worsen the decline rates in the long run, since these wells decline extremely fast.

The current rise in oil production in North America, one million barrel a day, has helped offset any outages coming from other oil producer countries and has helped the market remain in balance. Looking out a few years, global demand for oil will continue to increase because of rising prosperity in emerging economies. Supply, however, will still remain constrained.

Last year, IEA predicted that over the 2012-18 period, the largest contributors of new supplies to world markets, after the US and Canada, would be Iraq and Brazil. Iraq is expected to contribute to 45% of global oil growth between now and the end of the decade. Technical challenges seem insurmountable in Brazil, and Iraq has exploded to chaos again, implying that geopolitical factors are the wild cards in the oil equation and they can outdistance the “market only” factors.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The price of oil has risen continuously since 2004, when it was $30. Then, it spiked to $150 to come down to a floor of $100 per barrel in 2008. Today, the oil price is at about $110 per barrel and the markets have been relatively calm, as investors have assumed that Baghdad will not fall. But, the risk is to the upside. While the price of oil has been high, exploration costs have also taken the same trajectory. According to Goldman Sachs, oil companies would need the price of oil to be at $120 per barrel in order for them to balance their own budgets.

The relationship between economic growth and energy consumption is straightforward: the former is a function of the latter. With national economies around the world forced to pay more than $120 for every barrel of oil consumed, a critical question must be asked: what happens when the world's most important source of energy becomes unaffordable?

The writer is Sr. Assistant Secretary (Research & Development), Bangladesh Knitwear Manufacturers & Exporters Association (BKMEA).

E-mail: [email protected]

Comments