Bangladesh's destiny is largely in its own hands

GDP growth in Bangladesh is likely to recover in FY2015, driven by some revival in private investment activities, stronger domestic demand resulting from increased public investment in infrastructure, and domestic consumption growth getting a boost from remittance recovery and implementation of wage increases in the garment industry. Macroeconomic stability is expected to be maintained with underlying inflationary pressures, as reflected in non-food inflation, continuing to trend downward, aided by policy restraint. Bangladesh Bank has set a 6.5 percent inflation target for FY2015 and the first quarter data suggest the economy is on track to moving in that direction. Achieving the FY2015 inflation target will depend on international price trends as well as domestic demand and supply conditions.

International commodity prices, particularly crude oil and agricultural commodities, are expected to remain weak through the first quarter of 2015. A slowdown in the euro zone and emerging economies, a strong US dollar, increased oil supplies, and good agricultural prospects have contributed to the recent downtrends in international prices. However, what will matter most for Bangladesh are domestic supply-demand conditions and macroeconomic management. Inflation may be adversely affected if domestic demand is boosted by the monetary effects of a surge in remittances and/or monetisation of budget deficit target. It is reassuring that the monetary policy statement for FY2015 maintains a cautionary stance to ensure price and exchange rate stability as it did last year.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The immediate outlook for global growth is fragile. The IMF recently marked down its global growth projection for 2014 by 0.3 percent, to 3.4 percent, considering a less optimistic outlook for several emerging markets combined with a weak first quarter in 2014 in the United States. Downside risks remain a concern. Financial market risks include higher-than-expected US long-term rates and a reversal of recent risk spread and volatility compression. Global growth could be weaker for longer, given the lack of robust momentum in advanced economies, despite very low interest rates and the easing of other brakes to the recovery. In some major emerging market economies, the negative growth effects of supply-side constraints and the tightening of financial conditions over the past year could be more protracted. Bangladesh's ability to deepen and diversify export markets will depend on the strength of growth in advanced and emerging economies

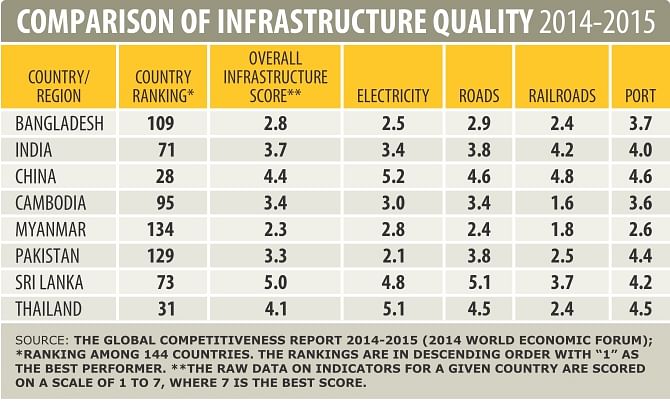

Yet global volatility is not Bangladesh's main worry. The macroeconomic risks hinge primarily on the vulnerability of domestic policies and politics. Even if external risks do not materialise, sustaining growth recovery will depend critically on mitigating the infrastructure deficit. Infrastructure investment increased from less than 1 percent of GDP in FY2009 to about 2 percent in FY2013, but that is still considerably lower than the 7-10 percent needed annually for next ten years to address Bangladesh's infrastructure deficit. Key infrastructure pillars are energy and transport. There has been some progress in improving Bangladesh's competitiveness ratings, most visibly in electricity supply. But there remain large deficiencies on the quality of infrastructure relative to different Asian countries (see Table). Even Pakistan, which ranks lower than Bangladesh in country competitiveness, is ahead on the quality of its roads and port infrastructure. The infrastructure gap is especially large with competitors like Sri Lanka, India and Cambodia. Much stronger attention is needed to achieve an efficient implementation of infrastructure investments along with necessary institutional changes relating to policymaking and regulation.

The availability of serviced land is another binding constraint for sustained growth enhancement. The land market is dysfunctional. Efforts to establish export processing zones (EPZs) have produced limited results, and there are no results yet in establishing special economic zones (SEZs). The latter are hindered by a number of bottlenecks, including infrastructure support for connecting ports and airports with functional roads and rail links along with efficient services.

Deficiencies in the availability and quality of power and gas are an equally important constraint, as are water and drainage connections, effluent treatment, and other basic facilities.

There are also other high-impact risks, particularly when combined with the possibility of a protracted slowdown in advanced economies. A lack of visible progress in upgrading labour and safety standards in garment factories could trigger loss of preferential access to EU markets. The inability to reopen job opportunities in the Middle East clouds the sustainability of remittance growth prospects. The deterioration in the state banks' financial solvency could challenge fiscal sustainability and constrain the availability of resources for public investment.

A resurgence of political unrest, even if it is not as ferocious and as long as experienced in the last half of 2013, is the principal domestic risk for the near term. This would depress private investment, push up inflation and potentially put reserves under pressure. Even if all the conditions are growth friendly, growth may remain elusive unless there is confidence about political stability and policy continuity. Bangladesh is well known as a case of growth despite a large governance deficit. This cannot be taken for granted.

Moving forward in the medium and long term, Bangladesh needs to create a system of governance that can successfully manage the interactions between the state and a well-functioning globally integrated economy. Managing such an economy requires inputs that markets do not automatically and adequately provide: infrastructure, security, rules, standards, certifications, training, and so on.

These can be made available only by professionally competent government agencies operating with adequate funds in a system that decentralises power to identify problems, work out solutions and monitor performance. The non-elected state institutions -- the higher echelons of civil bureaucracy or the Election Commission or the Anti-Corruption Commission and other watchdog bodies -- need the confidence of the public. Without restoring the credibility of these institutions, governance will not grow out of patronage politics. The economy may still stumble forward without harnessing all its potential.

All the hurdles Bangladesh is facing towards faster, more inclusive and sustainable growth are solvable if there is enough political will. Bangladesh's destiny is largely in its own hands.

The authors are respectively lead economist (Bangladesh) and country director (Bangladesh, Bhutan and Nepal) of the World Bank.

Comments