A number game for FY 15 budget

ACCORDING to media reports the finance minister has indicated that the size of FY 15 budget is going to be Tk. 2,50,000 crore. In a country like Bangladesh, characterised by one of the lowest government expenditure as proportion of gross domestic product (GDP), the desire to increase it is understandable. However, such desire needs to be tempered by a sense of realism. Otherwise, the budget would be viewed as a paper exercise with adverse implications for the government's credibility. This paper seeks to give an estimate of what should be a reasonable size of FY 15 budget.

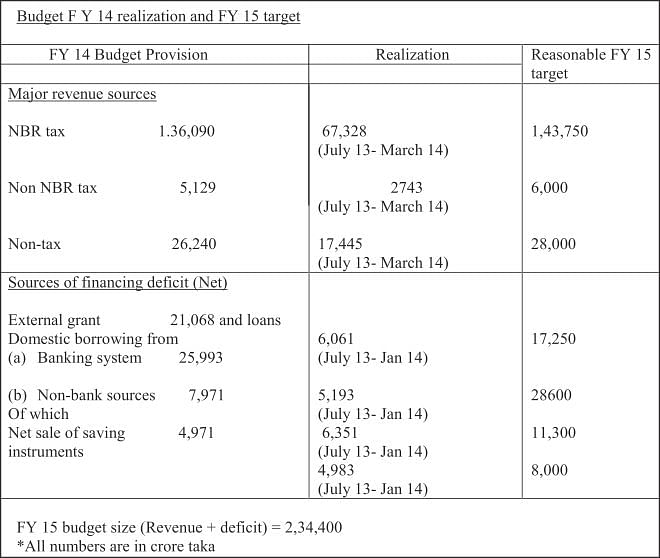

The size of a budget is equal to the sum of revenue and deficit. It should, therefore, be determined by the realistic possibility of raising revenue and of the amounts that can be collected from various sources of financing deficit.

Revenue scenario:

Revenue collected by the National Board of Revenue (NBR) is the largest source. The collection from this source in the current fiscal year has been rather disappointing. The government has already decided to revise the estimate downward from Tk. 1,36,090 crore targeted in FY 14 budget to Tk 1,25,000 crore. Assuming that (i) this revised target is realised (ii) growth of GDP in current prices during FY 15 would be of the order of 13% -14% and (iii) growth of collection would slightly exceed current price GDP growth, a reasonable growth of NBR tax revenue in FY 15 can be estimated to be 15% over the revised estimate of FY 14. However, mention should be made of some downside risks to this estimate.

Apparently the government is under intense pressure to reduce corporate tax rates as well as taxes on export income. There is a demand for raising the exemption limit of personal income tax. The government is likely to yield to some of these pressures. There is also a risk that the present lull in the political climate may not be sustained, leading to problems in collecting revenue from all three major heads, namely, personal and corporate income taxes, value added tax and import duty.

The collection from non-NBR taxes has been similarly dismal, amounting to slightly over 50% of budget provision during the first nine months of the current fiscal year. A major component of this source is the sale of non-judicial stamps. Given that the real estate sector is in a state of doldrums, one cannot expect any significant acceleration of collection of non-NBR taxes.

Information on the collection of non-tax revenue during the current fiscal year suggests that the budget target may just be met. This source is not generally income-elastic and therefore GDP growth does not exert much influence on collection from this source. It would be reasonable to assume a figure of Tk. 28,000 from this source representing an increase of about 7% over FY 14 budget provision.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Financing of deficit:

The disbursement of external grant and loans presents a rather pathetic picture. During the first seven months of the current fiscal year, the disbursement was less than 30%, amounting to just over Tk. 6,000 crore. Even an indomitable optimist would not expect eventual disbursement to exceed Tk. 15,000 crore. The projection of target for FY 15 adds another 15% to this figure.

As regards domestic sources, government's borrowing from the banking system has so far proceeded at a very slow pace. Based on past experience it can be assumed that this pace will gain momentum in the third and fourth quarters of the current fiscal year in tandem with acceleration of expenditure in the later part of the fiscal year. The present paper assumes that borrowing from the banking system will reach the level proposed in FY 14 budget and adds 10% to that level to estimate FY 15 target.

With regard to borrowing from the banking system some people argue that there is no problem for the economy at present if the government borrows heavily. The argument derives its logic from persistently growing excess liquidly in the banking system and hence little possibility of “crowding out” out of credit to the private sector. There is, however, a flak: the growing excess liquidity is largely accounted for by the rising share of what are dubbed as unencumbered approved securities the share of which in total liquid assets rose from 67% at the end of February 2013 to 73% at the end of January 2014. In the situation of virtual non-existence of secondary market, these securities comprising primarily government bonds can be hardly considered liquid.

The last remaining source of financing deficit is non-bank borrowing of which the major component is the sale of saving instruments. The government has already exceeded the budget provision for FY 14 under this head. The demand for purchase of saving instruments has received a stimulus from the falls in interest rates paid by banks on deposits. But the government needs to exercise restraint in the use of this source as the associated cost is the highest. The estimate for non-bank borrowing for FY 15 reflects this caution.

Domestic borrowing from either bank or non-bank sources imposes serious fiscal burden. This point is illustrated by the fact that FY 14 budget provision for interest on domestic borrowing amounts to nearly 20% of non-development expenditure. In contrast, the provision for interest on foreign loans is less than 1.3%.

It is worth reminding the readers that in an article following the announcement of FY 14 budget (The Daily Star, June 15, 2013) I predicted that the government would not be able to realise the targets of NBR tax revenue and external financing. Those predictions have unhappily proved to be correct. One area where my assessment has proved to be wrong relates to net sale of saving instruments. The reason has been alluded to above.

Based on the blend of caution and ambition contained in the preceding analyses I propose that the size of FY 15 budget should be Tk. 2,34,400 crores. Item wise figures are presented in the following table.

In view of the limited space I will not delve into the question of expenditure priorities. However, I would suggest that the size of annual development programme may be fixed at Tk. 67,000 crore. Even this will entail a significant jump considering that during the nine months of the current fiscal year only Tk. 28,300 crore was spent. Another factor which would necessitate conservative allocation for ADP is that non-development expenditure will have to be boosted in view of the likely increase in the remunerations of government officials on the basis of the recommendations of the Pay and Services Commission.

The writer is a former Adviser (Cabinet Minister) to the Caretaker Government, Ministries of Finance and Planning and presently a visiting Professor in BRAC University.

Comments