Will prices be revised?

We all know that oil prices have slumped globally. What many of us do not know is that the downturn has delayed about US$380 billion in investments on 68 major upstream projects. These dismal figures come through in a report by the Wood Mackenzie Ltd. According to a report by Bloomberg: "The developments account for about 27 million barrels of oil equivalent and about 2.9 million barrels a day of production is being deferred to early next decade, according to the Jan 12 report. Deepwater projects will be hit the hardest and account for more than half of new project deferrals."

That spells, perhaps not doom, but certainly bad news for major oil producing countries and companies globally. The fall in prices is forcing companies across the board to rethink not just new investments in finding new sources of oil but they are going back to the drawing board to rationalise cost of operations. That's why it's not surprising to find oil producers looking at ways to curtail budgets and initiate job cuts. With the price of oil hitting the lowest point in more than a decade and widespread concerns that these lower prices are going to be there for a while, we find companies shying away from investing in new exploration projects, where according to the Mackenzie report, the average break-even price is $62. With prices hovering below $30 a barrel, the quest for finding new oil is simply out of the question.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. It hardly comes as a surprise that the world's largest oil company, the Saudi Aramco is looking into selling a share in its downstream projects, i.e. refining and petrochemical units, and one cannot rule out selling off some of its crude oil reserves. In an era of low sustained crude prices, this oil giant, which ranks fourth in the world ranking of refiners, is looking for cash to consolidate its refined product line to take on the Chinese market for gasoline, diesel and other fuels. Taking a cue from the Saudis, there is little to suggest other major players will be putting money in virgin fields to explore new sources of hydrocarbons – given that there's too much of it stockpiled around the world anyway. And with the Iranians rebounding in production strength within a year; leaves us in a state of too much oil that will help sustain lower prices over a longer period.

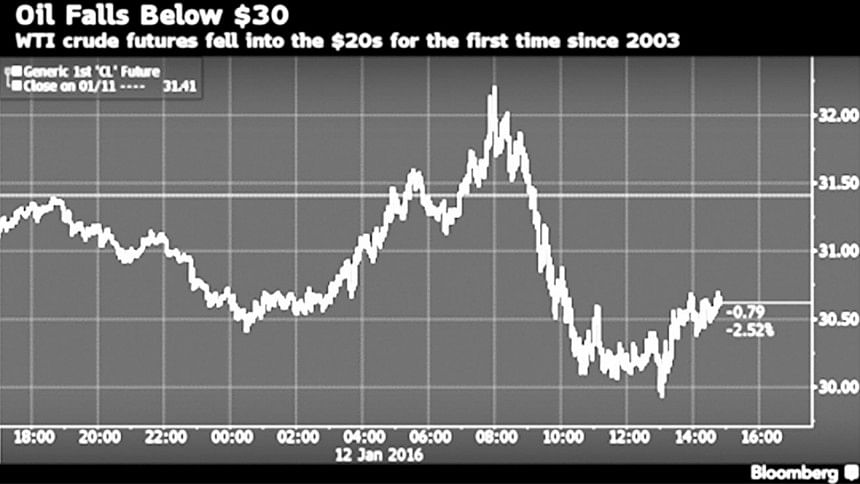

So where exactly are we headed? Some analysts have pointed out to a scenario where the Brent could go down to $20 a barrel and stay there; but it is difficult to predict the market. Goldman Sachs gives it a 50:50 chance that price per barrel of oil could drop to $20 in September of this year. What is not difficult to predict is that major oil producing nations are feeling the pinch all too well. For instance, according to some media outlets, Malaysia loses $68 million a day for every dollar decline in price per barrel. And the slowdown in growth of Chinese economy means that we are actually looking at a supply glut, and all that oil cannot be stored, it needs to be channelled to clients.

It opens up a huge window of opportunity for buyers to renegotiate purchase agreements. For us here in Bangladesh, the implications are all too relevant. Only recently, the Iranian envoy has made overtures that his country is looking forward to joint ventures with Bangladesh that include energy cooperation. While this is welcome news to say the least, one can understand why policymakers may wish to move cautiously, given the fact that the Kingdom of Saudi Arabia and the United Arab Emirates are two of the most important destinations for our expatriate workers. That notwithstanding, we should definitely explore the landscape about clinching better deals with existing suppliers whilst exploring opportunities with new ones.

We keep coming back to the issue of inflated pricing for petroleum products that exists in Bangladesh. Again, statements coming from policymakers are not very encouraging. Now why is that? If we are to take at face value what has been printed in The Financial Express on February 5, 2016 as its lead item, we are informed that the Bangladesh Petroleum Corporation (BPC) has settled all its liabilities (Tk. 71 billion) from profits earned previously. As per the statement of the BPC Chairman, "We have cleared dues with banks, paid outstanding value-added tax (VAT) and import duties to the national exchequer and freight charges to shippers."

Should prices in the domestic market remain unchanged and the current prices in the international markets hold, "the BPC's profit could exceed Tk263 billion within the next five years." By refusing to slash prices despite a price slump of oil in global markets and with BPC no longer in the red, we are putting the onus of higher prices of petroleum products onto manufacturers who in turn pass on the costs of higher production to the consumers – to put a complex situation in layman's terms. Is it worth keeping prices high? Perhaps it makes sense for some people at decision-making level; it certainly does not make sense to the rest of us.

The writer is Assistant Editor, The Daily Star.

Comments