BB cranks up vigilance on large borrowers

Bangladesh Bank is set to embark on a two-step programme to ensure that the loan situation of the sector's large borrowers do not go out of hand.

The decision was arrived at a board meeting last week after analysing the banks' large loan portfolio.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. “The large borrowers have become a threat to the health of most banks,” said a BB official preferring not to be named.

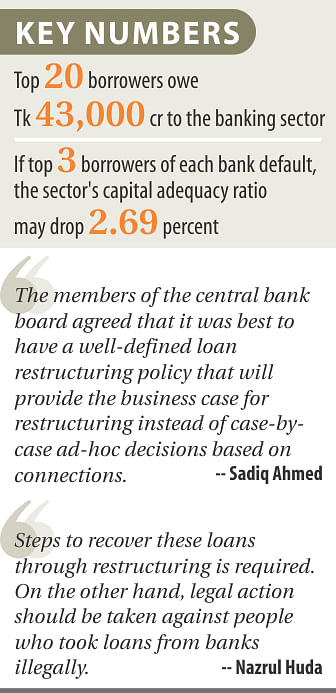

For instance, the central bank's most recent stress tests found that one state-owned commercial bank, 18 private commercial banks and four Islamic banks would be in a precarious situation if their top three borrowers defaulted.

Furthermore, the sector's capital adequacy ratio may drop 2.69 percent to take it below the critical 10 percent. At present, the banking sector's CAR is a little over 10 percent.

“Banks have become hostage to a number of big borrowers,” said Nazrul Huda, a former deputy governor of the central bank.

Many of the large borrowers have been lobbying for long-term restructuring of their loans and the banks too are in favour of the move, as it prevents their default loan portfolios from ballooning.

While it is true that many of the large borrowers have been affected by the global recession and the political instability, many have taken irregular facilities, according to Huda.

“Steps to recover these loans through restructuring are required. On the other hand, those who took illegal leverages need be identified and legal action taken against them,” he said, while citing the successes of neighbouring India as an example.

Subsequently, the central bank is set to form a high-powered panel led by one of its deputy governors this week to closely monitor the performance of the large borrowers and devise a mechanism to restructure their risky loans.

Restructuring is different from rescheduling in that a brand new repayment package would be suggested -- instead of simply extending the loans' maturity period -- after analysing the borrower's assets and liabilities as well as the health of his/her businesses.

Sadiq Ahmed, a member of the BB board, said the economy has been growing at a “respectable pace” of 6 percent per year and the government wants to increase the rate to 7 percent and beyond.

But for that, a healthy and stable banking sector is critical -- and the loan servicing capabilities of the large borrowers are central to that.

Since they pose special risks to the health of the banking sector, BB will pay special attention to them, said the former World Bank high official.

About the need for restructuring, Ahmed said: “The board members are mindful that in a market economy unforeseen circumstances can adversely affect the business of borrowers and in extreme circumstances bank loan restructuring might become necessary to set the business on a viable path.”

In that regard, the board members agreed that it was best to have a well-defined loan restructuring policy that will provide the business case for restructuring instead of case-by-case ad-hoc decisions based on connections, he added.

“The board will also watch the full compliance with single/group borrower exposure limits as per Bangladesh Bank policy, because of the special risk posed by large borrowers to the health of the banking sector.”

Many of the sector's large borrowers happen to be the largest borrowers of a number of banks.

Instead of each bank extending restructuring facility to the borrower separately, Huda suggested that the banks should get together and jointly analyse the loan portfolio to propose a suitable restructured package. Huda stressed that restructuring must be offered in such a way that it not only ensures loan recovery but also prevents repetition of the scenario.

The central bank last rolled out restructuring scheme in 2002 but no borrower was able to avail the facility.

As of September, the sector's top 20 borrowers account for around Tk 43,000 crore, which was 8.7 percent of the total loans then.

Of them, one borrower, who has a range of business interests, owes around Tk 7,000 crore, which is the highest.

On the second spot is another conglomerate, which owes more than Tk 6,000 crore. The next three slots go to a commodity businessman from Chittagong and two real estate businessmen. The five borrowers account for 60 percent of the loans.

Meanwhile, loan defaults have swelled by Tk 16,708 crore in the first nine months of the year, a development which has put the central bank in a state of great worry. “It is a matter of concern,” said Atiur Rahman, Bangladesh Bank governor, at a meeting with chief executives of all banks in mid-December.

At the end of September, the total defaults stood at Tk 57,290 crore, which is 11.60 percent of the total outstanding loans, according to central bank statistics. On December 31, 2013, it was Tk 40,583 crore, which was 8.93 percent of the total outstanding loans at the time.

“While the non-performing loans are particularly problematic for public banks, the incidence is also on the rise for private banks,” Ahmed said. “We discussed this challenge and agreed to take necessary actions to stem the tide of growing non-performing loans for both public and private sectors.”

Comments