BB raises reserve requirement for banks

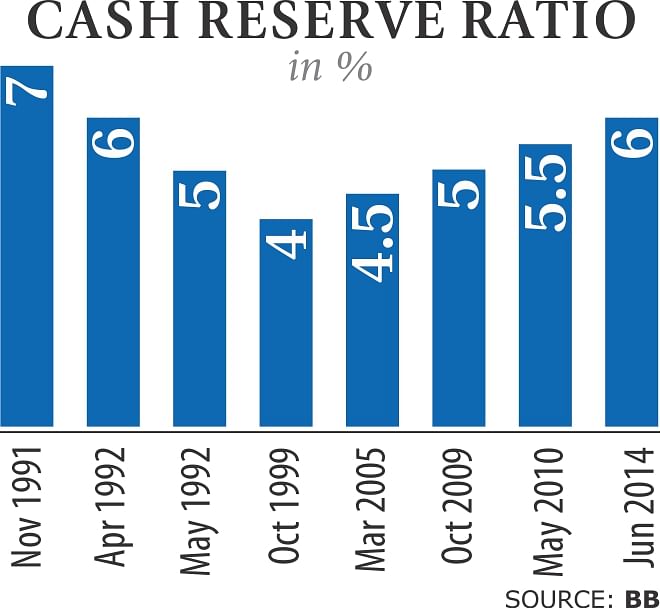

Bangladesh Bank yesterday raised the daily average reserve requirement for banks after a pause of four years to 6 percent from 5.5 percent in a bid to contain inflation.

Also called the cash reserve ratio (CRR), reserve requirement is the minimum fraction of customer deposits and notes that each commercial bank must hold as reserves or place with the central bank rather than lend out.

It is an important tool for monetary policy as it influences the country's borrowing and interest rates.

The higher the reserve requirement is set, the less funds banks will have to loan out, leading to lower money creation and perhaps ultimately to higher purchasing power of the money previously in use.

The notice dispatched by the central bank yesterday asked banks to keep their CRR at 6.5 percent on a fortnightly basis.

The move comes as banks sit on excess liquidity in the face of sluggish investment climate and businesses' increased tendency to obtain loans from abroad.

On May 1, the amount of excess liquidity in banks stood at Tk 102,223 crore, according to central bank statistics.

Typically, banks deposit the excess liquidity with the central bank, for which the rate of interest is 5.25 percent. The interest rate when banks borrow from the central bank is 7.25 percent.

Since January, banks have been depositing more money with BB than lending, meaning the central bank's earning potential by this channel has shrunk.

Hassan Zaman, chief economist of BB, said the banks' increasing tendency to rush to the central bank to park their excess liquidity has sharply increased BB's costs.

By extension, it has increased the costs for taxpayers as well, since it implies that BB can contribute less to the national coffer, he said. “By raising the CRR, we save a portion of these costs.”

The step will not affect investment, as private sector credit growth figures show that there is “sufficient space for banks to lend to their customers if they wish to,” Zaman said.

The private sector credit growth for the first half of the year was 16 percent, but till May it stood at 11 percent, according to BB Deputy Governor SK Sur Chowdhury.“As a result, the banks have an opportunity to increase private sector credit growth by 5 percent,” he said, adding that if excess liquidity lies with banks for long, investment in unproductive and risky sectors will increase, which may create inflationary pressures.

Moreover, this move also helps in achieving BB's reserve money targets, which will help in bringing non-food inflation down further, Zaman said.

The government's plan is to contain inflation within 7 percent in the outgoing fiscal year but until May it stood above the target. In the next fiscal year, the government has set a target of bringing it down to 6 percent.

“So overall, there are lots of advantages to this as entrepreneurs won't suffer from a fund shortage, it has inflation benefits and lowers the interest burden on the public,” Zaman said.

Zahid Hussain, lead economist of the World Bank's Dhaka office, said increasing CRR is not a risk-free step.

“The risk is that it may stem the recent declining trend in lending rates, at a time when the private demand for credit is tending to rise, although only weakly so.”

“BB can mitigate this risk by taking a harder stance on central government borrowing from the banking system and loss financing of state-owned enterprises.”

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments