Banks struggle as loan appetite diminishes

Banks are facing a huge mismatch between credit and deposit growth, which has not only affected their profitability but also hurt savers.

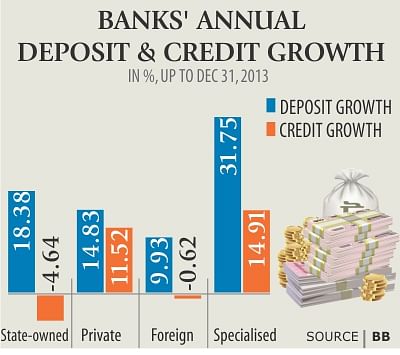

In 2013, bank deposits grew 16.26 percent and credit only 7.41 percent from a year ago, according to central bank statistics.

Though the banks' deposits increased, they are unable to invest the money, leaving them with excess liquidity of around Tk 90,170 crore on December 31, 2013. Subsequently, both the deposit and lending rates were slashed.

On average, the deposit and lending rates last December stood at 8.39 percent and 13.45 percent respectively in contrast to 8.47 percent and 13.8 percent a year ago.

As the deposits could not be invested, most of the banks have lowered the interest rate on them, a bank official said, adding that the rate of interest on term deposit in most of the banks is a maximum of 11 percent, which was more than 13 percent even a few months ago.

The state-owned banks, which have cut their rate of interest more than the private banks, have discontinued various deposit schemes using various excuses to check their losses.

Zaid Bakht, research director of Bangladesh Institute of Development Studies (BIDS), said the investment demand was low for the last two years, but political unrest in the closing months of 2013 compounded it.

Bakht, who is also a director at Sonali Bank, the largest state-owned bank, said they are not getting any application for term loans of late, while the demand for trade financing has also decreased.

The scams unearthed in the banking sector in 2012 had a lingering effect, prompting officials to exercise greater caution when giving out loans, he said.

Moreover, the higher-ups have taken off the authority from the lower echelons of the banks to grant loans.

To recover the losses from the idle deposit, the banks have been investing in the treasury bills and in the call money market, but the interest rate there has been low as well.

Subsequently, the Sonali Bank board has now urged the management to set targets for the bank branches, in a bid to speed up disbursement.

Bakht also said the bank management has been asked to quickly process the good loan proposals.

In the first quarter of the fiscal year, industrial term loan disbursement dropped 8.64 percent year-on-year, while trade financing 12.9 percent, according to central bank statistics.

Meanwhile, the monetary policy statement for the second half of the fiscal year released on Monday said the credit decline is partly due to sluggish investment demand in the lead-up to national elections, tighter lending practice by banks as well as the fact that there are two new channels through which entrepreneurs can excess overseas lenders who offer lower cost financing.

One existing channel is borrowing by companies for term-credit purposes, with most having a maturity beyond five years—around $534 million was approved in first six months of the fiscal year, which was $1.82 billion last fiscal year and $1 billion in fiscal 2011-12.

In addition, private capital flows to local companies have also grown due to the addition of short-term foreign currency loans for working capital purposes in the form of 'buyers credit' and 'discounted export bills'.

Lending rates have fallen faster than deposit rates, Bangladesh Bank said in its monetary policy statement. Domestic lending rates have fallen due to lower costs of funds for banks, lower demand for credit as well as due to increasing competition from overseas lenders whose lending rates are in single digits, it added.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments